As the global race for compute heats up, artificial intelligence in Africa is hitting a critical inflection point in 2026. A homegrown revolution is bridging the gap through Small Language Models (SLMs) and edge computing. From the $1.5 trillion potential of the AfCFTA Digital Trade Protocol to the surge of AI startups in Nigeria, Kenya, and South Africa.

The framing problem

Most coverage of “AI in Africa” starts in the wrong place. It opens with a statistic about smartphone penetration, pivots to a quote from a Silicon Valley executive about untapped markets, and ends with a list of pilot programmes that may or may not still be running.

This hub starts somewhere different: with the distinction between AI deployed in Africa and AI built by Africans. These two things are not the same, they don’t require the same infrastructure, and they don’t produce the same economic outcomes. Conflating them — as most reporting does — obscures what is actually happening on the continent and why it matters.

AI labelled by Africans. A significant proportion of the human labour powering the global AI boom runs out of Nairobi, Lagos, and Accra — workers annotating data, moderating content, and training models for companies headquartered in San Francisco. Understanding where this fits in the picture is essential to any honest account of African AI in 2026.

Taken together, Africa occupies three distinct roles simultaneously.

- Target market for global AI products

- An increasingly serious origin point for homegrown ones

- And a labour source for the global AI supply chain.

Each role produces different economic outcomes and different political stakes. Throughout this tracker, we distinguish between them.

Scale and stakes: why this moment is different

Africa’s basic demographics are well known but bear repeating in the AI context. The continent holds approximately 1.6 billion people, a median age of around 19, and the fastest-growing internet population on Earth. Moreover, the African AI market is projected to grow at a compound annual rate of 28.34% through 2030, potentially reaching $16.5 billion.

Those numbers are real — but they are also a trap. Large addressable markets do not automatically translate into homegrown capability. The history of mobile money in Africa — genuinely transformative, genuinely African-led — is the better template than the history of social media, which arrived as an imported product built on infrastructure Africa does not own.

Who captures the value?

According to McKinsey’s State of AI Africa survey, more than 40% of African organisations have either started experimenting with generative AI or deployed significant AI solutions. That is adoption, not creation. Meanwhile, 159 African AI startups have raised a combined $803.2 million in total funding — less than what major US AI companies raise in single funding rounds.

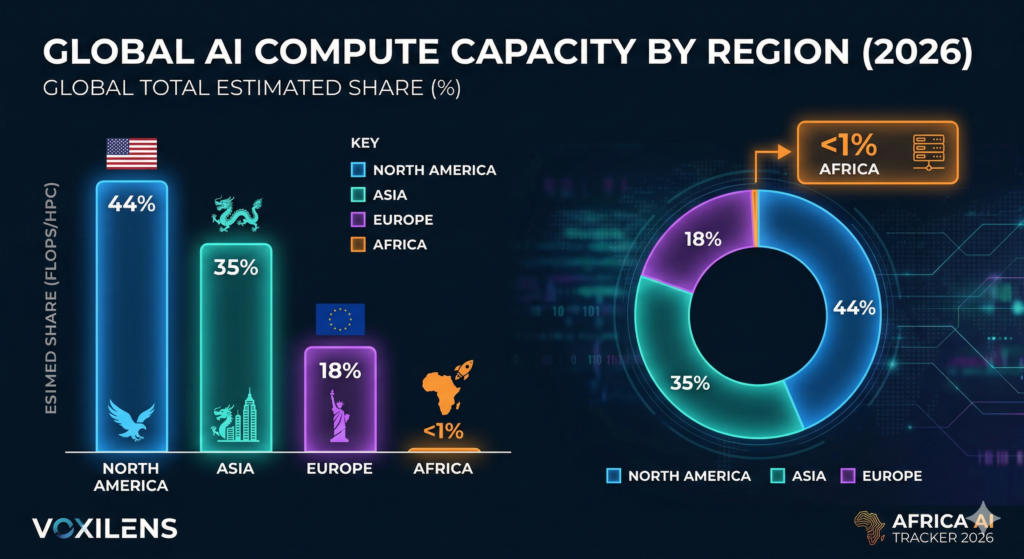

The compute gap — in one number

Africa holds less than 1% of global compute capacity. The United States alone accounts for roughly 34%, and the entire African continent has less compute infrastructure than the state of Virginia. No amount of enthusiasm or policy rhetoric can close this gap quickly. It is a physical constraint that shapes every other dimension of African AI development.

Global AI compute capacity by region in 2026

Homegrown AI: startups, models, and talent

The 2026 African AI Startup Landscape

| Country | Hub Status | Startup Count (2026) | Market Significance |

| Nigeria | Primary Hub | 50 | Leads in volume; driven by the Lagos “Yaba” tech ecosystem and fintech AI. |

| South Africa | Primary Hub | 49 | The continent’s compute anchor; specializes in industrial and language AI. |

| Kenya | Primary Hub | 31 | High capital efficiency; leader in 90% renewable-powered data centers. |

| Ghana | Emerging Cluster | 13 | Notable strength in healthtech and diagnostic AI (e.g., minoHealth). |

| Tunisia | Emerging Cluster | 11 | Consistent growth; strong technical talent pipeline in North Africa. |

| Egypt | Emerging Cluster | 11 | Fastest Growth: 267% increase since 2022; emerging as the “Fourth Hub.” |

Summary table of the 2026 African AI startup landscape, showing Nigeria, South Africa, and Kenya as dominant hubs with Egypt as the fastest-growing market.

Key Insights at a Glance

- The Power Trio: Nigeria, South Africa, and Kenya still command the lion’s share of the market, accounting for 63% of all tracked AI startups.

- The Egypt Surge: Rising from just 3 startups in 2022 to 11 in 2025, Egypt is the most aggressive newcomer to the “top tier” landscape.

- Regional Consolidation: The presence of double-digit clusters in Ghana and Tunisia suggests that AI development is no longer isolated to the traditional tech “heavyweights.”

What the money is funding

Investment in AI during 2025 was largely applied rather than speculative. Rather than backing standalone AI platforms, investors favoured companies integrating AI into finance, agriculture, logistics, health, and commerce. The sector split matters.

African AI startups concentrate in verticals where the problem is urgent, the customer is paying, and regulatory friction stays manageable. Fintech AI dominates deal flow; agritech and healthtech follow, partly because international development capital flows into those sectors regardless of VC cycles.

Still missing, and what the ecosystem needs more of, is foundational infrastructure. The data pipelines, compute platforms, and language datasets that would let every subsequent startup build faster.

Standout companies to watch

- Lelapa AI (South Africa) — building language AI for South African languages. Its VulaVula API covers Zulu, Sesotho, and Afrikaans, and InkubaLM is specifically designed to run on low-resource hardware in rural settings.

- DataProphet (South Africa) — industrial AI for manufacturing defect prevention. Rather than automating an existing process, it solves a genuinely hard technical problem.

- Neural Labs Africa (South Africa) — clinical AI for respiratory diseases, trained on African X-ray data and optimised for the lower-resolution imaging equipment typical of regional clinics.

- minoHealth AI Labs (Ghana) — Darlington Akogo runs West Africa’s leading AI-powered diagnostic facility. Deep learning models for chest X-rays achieve an AUC-ROC of 0.97, outperforming human radiologists by 10%. Notably, the Government of Barbados has adopted minoHealth’s infrastructure, demonstrating that African-built systems meet global standards.

- Zindi (pan-African) — a data science competition platform with over 70,000 engineers building production-ready AI models, including work for UNICEF and the Government of Malawi.

The definition problem

The question of definition matters more than it sounds. How you define a thing determines whether it gets counted, and whether it gets counted determines whether it gets funded.

A genuine African AI startup is one where AI is not merely a feature but the primary mechanism through which the business creates value — through predictive modelling, intelligent automation, or data-driven decision tools built on locally relevant datasets.

By that standard, many “AI startups” counted in continental reports are better described as tech startups with an AI module.

→ Full breakdown: African AI startups: the 2026 landscape report

The Francophone gap

The dominant narrative of African AI is Anglophone. Nigeria, Kenya, South Africa: large markets, established venture ecosystems, English-language developer communities that integrate easily with Silicon Valley’s professional networks. This framing carries a structural bias, and it is worth naming directly.

Senegal

In February 2025, President Bassirou Diomaye Faye launched Senegal’s “New Deal Technologique Horizon 2034” — a ten-year digital strategy backed by a $1.7 billion budget. By 2034, the plan targets over 500 recognised tech startups, 150,000 direct digital economy jobs, and digital contributing 15% of GDP.

Adopted in 2020 but made fully operational from 2025, the Startup Act creates a legal and fiscal framework for innovative startups: targeted tax incentives, official startup status recognition, and simplified administrative environments.

In November 2025, the Ministry of Communication, Telecommunications and Digital Economy formally launched the Startup Ecosystem. Rather than replicating Anglophone models, Senegal is positioning itself explicitly as a Francophone digital hub — building for French and Wolof-speaking West Africa and the diaspora.

Côte d’Ivoire

Abidjan has seen accelerating AI activity in agritech and GovTech. Driven partly by its role as the economic capital of Francophone West Africa and partly by French development finance (AFD) investment in digital infrastructure. The country’s proximity to Ghana means Anglophone and Francophone networks increasingly overlap, which is pulling both ecosystems closer together.

Morocco

It sits at a different intersection: Arabic, French, and increasingly English. Casablanca’s tech ecosystem — home to companies like DeepEcho and a growing cluster of applied AI startups — benefits from proximity to European markets. Additionally, the Mohammed VI Polytechnic University has become a serious AI research institution, and Morocco hosted GITEX Africa 2026 in Marrakech in April 2026, signalling its ambition to be the northern gateway to continental AI investment.

The Francophone gap has three roots:

- Most AI research and funding documentation is in English (a language problem).

- Francophone African founders have historically been better connected to Paris than to Nairobi or Lagos (a network problem).

- And data collection for Francophone markets is systematically less comprehensive (a measurement problem).

None of these explanations make the gap acceptable for a tracker claiming continental scope.

→ Further coverage : AI governance in Africa: country-by-country tracker

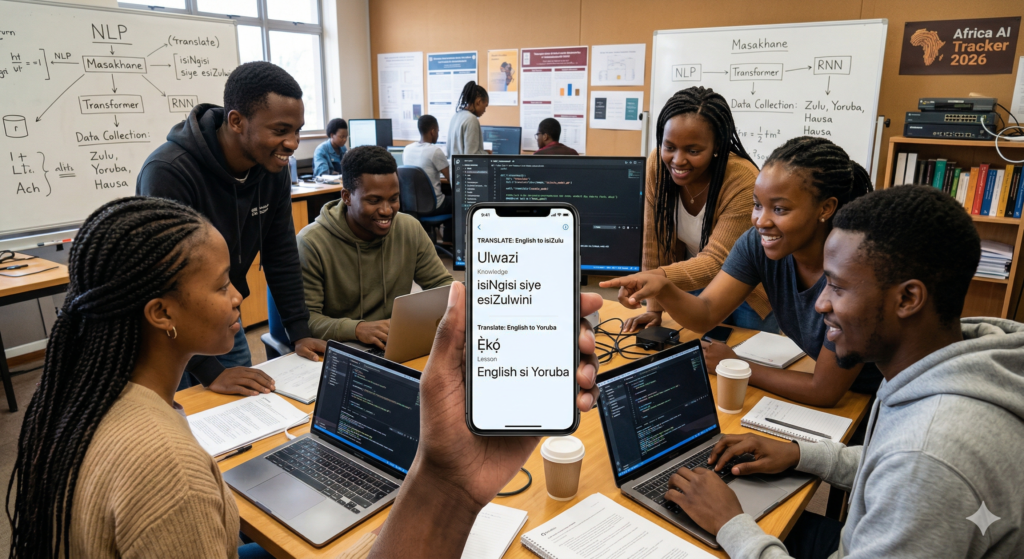

African AI researchers developing the Masakhane NLP project, featuring a smartphone interface with Zulu and Yoruba language machine translation.

Who is building the African language LLMs

Africa is home to over 2,000 languages, yet none of the top 34 languages used globally on the internet are African. This is not an abstract concern. When a language is absent from training data, its speakers cannot access AI tools meaningfully — not for healthcare information, not for legal advice, not for the productivity gains the rest of the world is beginning to take for granted. Put simply: when a language isn’t in the data, its speakers aren’t in the product.

Masakhane is the most important organisation in this space. A pan-African NLP network — its name is isiZulu for “we build together.” It coordinates over 1,000 contributors, with 35 active contributors creating machine translation tools and publishing results for over 48 African languages.

In January 2026, the Masakhane African Languages Hub launched a grant scheme to fund high-quality datasets for 50 African languages, supported by Google.org ($3 million), the Gates Foundation, FCDO, and IDRC. The target: empowering one billion Africans with locally designed AI tools by 2029.

Community-led initiatives like Masakhane are training transformer models — including AfriBERTa and SwahBERT — on African languages including Amharic, Hausa, Swahili, and Yoruba, with these models frequently surpassing mBERT in downstream tasks.

Lelapa AI’s VulaVula is a production-ready API for South African languages now in active commercial deployment. UlizaLlama, built by Kenyan health company Jacaranda Health, provides maternal healthcare advice in Swahili — the clearest example of why language AI is not a niche research project.

Why SLMs are the strategy, not the compromise

The compute required to train large foundation models is beyond the reach of most African research institutions. However, purpose-built Small Language Models have proven to outperform general-purpose LLMs for specific tasks — mathematical reasoning, code generation, domain-specific applications like healthcare and legal advice.

They are faster, more cost-effective, and easy to fine-tune with limited resources. Crucially, they run on edge hardware without cloud connectivity. For a maternal health tool deployed in rural Kenya, an SLM that runs on a basic Android phone is not a fallback — it is the appropriate solution. Africa’s language model builders are not waiting to afford GPT-scale compute; instead, they are building for the constraint.

→ Here’s a full breakdown on who’s building the African language LLMs

Talent, brain drain, and the return

The honest picture here is mixed. African universities — particularly in South Africa, Kenya, Nigeria, Rwanda, and Morocco — are producing machine learning researchers of genuine global standing. Many leave for North America or Europe for PhDs and remain there, drawn by compute access, institutional infrastructure, and salary differentials that homegrown ecosystems cannot yet match.

The counterforce is the Deep Learning Indaba. An annual pan-African AI research gathering that has become the continent’s most important technical community event. Alongside a growing number of researchers making deliberate choices to return or remain.

The Masakhane-to-startup pipeline is starting to function as an actual career path. Even so, the fundamental constraint is not attitude — it is that world-class researchers cannot do frontier work without frontier compute, and most of that compute is not in Africa.

Infrastructure: compute, power, and data centres

Comparative view of Kenya’s geothermal solar farms and a Tier-4 data center in South Africa

South Africa as Africa’s compute anchor

South Africa is not Africa’s largest economy by some measures, but it is decisively the continent’s compute hub. Around 69 operational data centre facilities confirm its role as the digital gateway for enterprise, cloud, and AI services in sub-Saharan Africa.

The reasons are structural and self-reinforcing:

- Best undersea cable connectivity on the continent,

- Most developed financial infrastructure,

- More stable regulatory environment,

- And historically more reliable power than peers.

Consequently, the hyperscaler footprint has grown substantially. Microsoft announced $300 million for cloud and AI infrastructure in South Africa by end-2027.

Plans for significant hyperscale expansion have emerged that would push current IT power load over 1,200 MW. Teraco (Digital Realty) plans four new data centres in 2025–2026 with a cumulative investment of approximately $877 million.

The data centre market is projected to grow from $580 million in 2025 to $1.25 billion by 2030, at a CAGR of about 16.6%.

That concentration carries a cost that investment press releases rarely discuss. Most African startups outside South Africa depend on foreign-hosted cloud infrastructure — South African or European — to run their products. That is a latency problem, a data sovereignty problem, and a currency problem simultaneously.

→ Full breakdown in the spoke: South Africa as Africa’s compute anchor

The power problem: load-shedding and AI

South Africa’s load-shedding crisis is in partial remission. Eskom improved its performance significantly in 2025. The improvement, however, deserves careful reading: considerable talk suggests the grid is “sorted” due to fewer outages, yet demand has dropped significantly because customers adopted backup power and solar generation. The grid hasn’t improved as much as demand has decreased.

Teraco’s response is instructive. In 2026, the company is building a 120MW solar farm in Bloemfontein to wean itself off the unreliable grid — because any significant growth in data centre capacity must now be filled by renewables. There is simply no alternative.

Data centres in South Africa must invest in diesel generators, battery backup, and solar-plus-storage installations to meet uptime guarantees. These costs pass directly to tenants, meaning African startups pay a power-risk premium that competitors in Frankfurt or Virginia do not.

Nigeria’s power challenges are more severe still: diesel generator dependency is the norm for any Lagos business requiring guaranteed uptime. And the cost — denominated in US dollars against a volatile Naira — compounds the burden further.

Kenya’s structural advantage is worth stating clearly. Kenya’s grid runs at approximately 90% renewable — primarily geothermal from the Rift Valley. This gives Kenya power stability and sustainability that is genuinely competitive globally, which is part of why it has attracted disproportionate cloud investment relative to its GDP.

Kenya leads the continent in total AI capital raised, with $242.3 million across 19 companies and an average funding level of $12.8 million per startup.

→ Full breakdown in the spoke: Data centers and load-shedding: the power problem

Connectivity and the edge AI imperative

With roughly 40% of Africa still offline, the dominant AI deployment model for most of the continent is not cloud-based inference — it is edge AI. A maternal health tool deployed in rural Nigeria does not look like a ChatGPT interface. More likely, it resembles a USSD menu accessible on basic feature phones without a data connection, with AI-generated responses running behind it. Almost certainly, it uses a smaller model than anything deployed in San Francisco.

Far from a deficiency, this is a design constraint that is producing some of the most interesting applied AI engineering on the continent. Builders who cannot rely on cloud compute are solving optimisation problems that well-resourced teams in data-rich environments never confront.

Policy, governance, and trade frameworks

Country-by-country governance tracker

African AI governance is fragmented, uneven, and in most countries, embryonic. The gap between continental rhetoric and national implementation is real and widening.

Tier 1 — Active, published strategy:

- South Africa — the most developed framework, with a National AI Policy process and the AI Institute of South Africa (AIISA) active on research governance.

- Egypt — a published National AI Strategy with specific targets, and the largest AI startup count on the continent.

- Rwanda — punches above its weight on digital governance. The Smart Rwanda initiative has made it a continental reference point on data protection.

- Kenya — an active strategy, bolstered by the presence of Google and Microsoft regional hubs in Nairobi. Notably, Kenya is the only country in Africa whose national AI strategy directly names and acknowledges the exploitation that data labellers face.

Tier 2 — Policy in progress:

- Nigeria, Ghana, Morocco, Ethiopia — frameworks at various stages of consultation or draft. Nigeria’s National Centre for Artificial Intelligence and Robotics (NCAIR) is the institutional anchor but has struggled with funding and mandate clarity.

- Senegal — deserves special mention. The New Deal Technologique Horizon 2034, launched February 2025 with a $1.7 billion budget, combined with the operationalisation of the Startup Act in November 2025, places Senegal meaningfully ahead of most Tier 2 countries. In practice, it is a Tier 2 country executing with Tier 1 ambition.

Tier 3 — No formal framework:

- The majority of sub-Saharan Africa. For countries like Tanzania and Côte d’Ivoire — where AI adoption is accelerating — the absence of governance frameworks represents a growing gap.

African leaders have signed onto multiple multilateral AI agreements, including the Bletchley Declaration on AI Safety and the Africa Declaration on AI. Nevertheless, the challenge remains translating declarations into domestic legislation with genuine enforcement capacity.

→ Full country-by-country breakdown: AI governance in Africa: country-by-country tracker

AfCFTA Digital Trade Protocol — what it means for AI

The African Continental Free Trade Area’s Digital Trade Protocol is the most consequential and least-covered AI policy development in Africa right now.

In practice, the protocol governs how AI products are licensed, how data flows across borders, and whether a startup in Lagos can legally sell model outputs to a company in Accra without navigating two separate regulatory regimes.

What the protocol covers — and where it chafes

The protocol covers cross-border data flows, digital payment frameworks, consumer protection in digital transactions, and data localisation requirements. That last element is where the tension lives.

Several African countries have enacted or are drafting data localisation laws — legitimate sovereignty instruments that nonetheless sit uncomfortably against the logic of a continental free trade zone that assumes frictionless data movement.

For AI specifically, the implications are significant. Training a model on pan-African data — the kind of dataset that would actually capture linguistic and cultural diversity across the continent — requires moving data across borders. If each country applies different localisation rules, that becomes legally treacherous very quickly.

Who has ratified, and who hasn’t

The protocol has not yet been ratified by enough countries to enter into force. Countries that have moved fastest on ratification are, broadly, the same ones with active AI governance frameworks: Rwanda, South Africa, Kenya.

The holdouts tend to be countries where data localisation is politically sensitive or where the digital economy remains small enough that the protocol feels abstract.

→ Full explainer : AfCFTA Digital Trade Protocol: the full explainer

The geopolitical AI race: China, the West, and what Africa actually chose

So far, this article has discussed the Western hyperscalers — Google, Microsoft, Meta — as the primary external actors in African AI. That framing misses a variable that is arguably more consequential for the continent’s AI infrastructure: China.

Huawei’s hardware dominance

Huawei equipment accounts for nearly 70% of 4G infrastructure in Africa, and the company was the first to offer 5G services on the continent. Consequently, when an African mobile carrier runs AI inference on its network, that inference almost certainly runs on Huawei infrastructure. Beyond networking, Huawei alone is involved in 25 data centre and e-governance projects across Africa.

This is not only a commercial relationship — it is a governance one. Huawei’s “Safe City” programme bundles facial recognition, licence-plate recognition, social media monitoring, and integrated command centres into a single package.

Cities across Egypt, Nigeria, South Africa, Uganda, Kenya, Zimbabwe, and at least nine other African countries have deployed it. Nairobi was the first African city to go live with the system, in 2014; today, the city has nearly 2,000 Huawei surveillance cameras sending data to the police.

AI surveillance systems developed by Chinese companies now operate in 13 African countries, with equipment from Hikvision and CloudWalk specifically underpinning SafeCity and SmartCity projects. Chinese technology equips 24 presidential residences, 26 parliamentary offices, and 32 police or military installations across Africa. In Uganda, for example, digital rights groups explicitly linked a $126 million Huawei facial recognition purchase to the suppression of political opposition.

DeepSeek’s relevance to Africa

The rise of DeepSeek in early 2025 matters for Africa specifically because it offers a capable, open-source model dramatically cheaper to run than OpenAI or Anthropic alternatives. For African developers working with constrained budgets and limited cloud credits, open-source frontier models change the economics of building.

Whether those models carry Chinese data governance defaults — or whether African builders can audit and modify them freely — remains an open question that national AI governance frameworks are not yet equipped to answer.

What this means for African AI governance

African governments face a genuine dilemma. Chinese infrastructure is cheaper, arrives faster, and comes bundled with financing that Western alternatives rarely match. Western “Responsible AI” frameworks, by contrast, arrive with governance conditions that African policymakers sometimes experience as patronising and inconsistently applied.

The February 2025 Paris AI Summit — at which the United States refused to sign declarations on “inclusive” AI — did not go unnoticed on a continent that has faced repeated lectures on AI safety from governments running significant surveillance programmes of their own.

In practice, most African governments are not choosing between Chinese and Western AI models as an ideological matter. Rather, they are making pragmatic infrastructure decisions, vendor by vendor, while the governance implications accumulate silently in the hardware layer.

→ Further coverage : AI governance in Africa: country-by-country tracker

Investment and Big Tech attention

Why Big Tech is finally paying attention

The case for Africa as an AI market is straightforward: 1.6 billion people, the fastest-growing urban population on Earth, a majority mobile-first user base, and an AI adoption curve that is steep precisely because the baseline is low.

Google has made the most substantive public commitment. Beyond the $37 million announced in Accra in July 2025 — covering the Masakhane language hub, food security AI, and research funding for African institutions — Google runs the Google for Startups Accelerator: Africa, which has supported 153 startups from 17 countries. Those startups have collectively raised over $300 million and created more than 3,500 jobs.

Microsoft is making the largest infrastructure bet: $300 million in South Africa, alongside a collaboration with Cassava Technologies — the continent’s largest network of interconnected, neutral facilities, effectively serving as Africa’s digital economy backbone — giving it distribution reach its competitors lack.

Meta’s most consequential African investment is not a press release. Rather, it is the WhatsApp integration through which most African users will first encounter AI. Meta’s No Language Left Behind (NLLB) project produced translation models for 200 languages including dozens of African ones, forming the technical foundation. From an African perspective, WhatsApp AI deployment is the most significant consumer AI launch of the last two years.

The investment reality check

In 2025, global AI startup funding reached $270.2 billion — 52.7% of all venture capital deployed worldwide. North America alone took $214.5 billion. By comparison, Africa’s $803 million in total AI startup funding over five years represents less than what major US AI companies raise in single rounds.

Nevertheless, the trajectory is moving. African startups raised more than $700 million across 59 deals in Q1 2026, with debt financing now accounting for the majority of capital. Egypt attracted $190 million, South Africa $157 million, and Nigeria $78 million. The shift toward debt over equity is a maturation signal: growth-stage companies are replacing equity dilution with structured debt, which happens when ecosystems develop enough exit history for lenders to trust their assets.

→ Full analysis: The 1.6 billion consumer AI market: why Big Tech is finally paying attention

Nigerian AI: Lagos and the ecosystem {#nigeria}

Nigeria is simultaneously the most active and most constrained AI environment on the continent.

Activity without capital

Nigeria dominates the most recent startup founding cohort, with 14 new AI startups in 2024–2025. Lagos — specifically the Yaba tech district — is home to a developer community that is large, technically capable, and increasingly oriented toward AI rather than pure web and mobile development. Yet the constraints here are not talent. They are infrastructure and macroeconomics.

Nigerian companies, despite the country’s large market, have raised only $47.3 million across 34 startups — a striking mismatch between startup volume and available capital. Currency volatility partly explains this.

Power is the other structural issue: every Lagos tech startup is also, in effect, an energy company managing its own supply. GPU-intensive AI workloads require stable, high-voltage power that the grid does not provide.

What is being built despite this

Despite these constraints, the calibre of output is high. Dr. Tobi Olatunji developed Africa’s first clinical speech-to-text AI trained specifically on African accents. After deploying it at University College Hospital, Ibadan, radiology reporting time fell from 48 hours to 20 minutes. That is not a pilot.

→ Full deep dive : Nigerian AI: the Lagos tech ecosystem

AI in practice: healthcare

A healthcare worker in a rural Kenyan clinic using an AI-powered diagnostic tool on a tablet to analyze patient X-rays in real-time.

Why healthcare is the sector that matters most

The structural case for AI in African healthcare is overwhelming. Doctor-to-patient ratios across sub-Saharan Africa are among the lowest in the world. Diagnostic infrastructure is sparse, and maternal and neonatal mortality rates remain high in countries where the proximate cause is often delayed or absent diagnosis.

This is not a market opportunity framing. It is a statement about where AI can do its most important work.

Real deployments, not pilots

The most important distinction in African health AI reporting is between pilots and deployments. A pilot runs in one clinic for six months with external funding and research supervision. A deployment, by contrast, runs continuously, is paid for by someone with a stake in the outcome, and has survived the transition from controlled conditions to real-world chaos.

Adeola Ayoola, founder of Famasi Africa, built “Remi,” an AI agent predicting medication stockouts and managing refills for over 20,000 patients. Shamim Nabuuma’s Chil Femtech platform enables AI-supported self-collection cervical cancer screening in Uganda and Tanzania.

In rural Zimbabwe, Tafadzwa Kalisto Munzwa of Dawa Health uses multimodal AI combining computer vision and language models to detect pre-cancerous lesions with 96.7% accuracy, cutting anemia detection from three days to five minutes. Dr. Abiodun Adereni’s ADVISER framework, meanwhile, increased vaccination retention in rural Nigeria from 45% to over 70%.

Lelapa AI’s InkubaLM runs on low-resource hardware typical of rural clinics. Its VulaBula API lets patients describe symptoms in African languages — because describing symptoms in a language learned at school rather than the one you think in introduces a diagnostic barrier that is easy to overlook when designing systems from a position of multilingual comfort.

The implementation gap

For every functioning deployment there are several tools that worked in controlled conditions and then stalled. Three problems explain most of the failures.

Connectivity. A diagnostic tool requiring 4G to run inference cannot deploy in a rural clinic with only 2G or USSD access. Edge AI offers the solution, but optimising models for edge deployment demands engineering time and compute access that most African health AI teams lack in abundance.

Regulation. No pan-African medical AI approval pathway exists. A tool validated in South Africa faces different regulatory processes in Kenya, Nigeria, and Ghana, which dramatically increases the cost of continental scale for any health AI product.

Data sovereignty. When an international NGO funds a diagnostic AI project in a Kenyan hospital, who owns the model weights? This is not a theoretical question — it shapes whether African-built models remain in African hands.

→ Full deployment tracker: AI in healthcare across sub-Saharan Africa

AI in education: the overlooked deployment

Healthcare gets the evidence base; education gets the narrative. The honest position in 2026 is that AI EdTech in Africa is at an earlier stage than health AI — more pilots than deployments, more promise than proof. Even so, the structural need is not smaller.

The scale of the problem

Africa faces a teacher shortage of approximately 17 million, projected by UNESCO to persist for decades. Average primary school class sizes in many sub-Saharan countries exceed 50 students.

Furthermore, the colonial-era language problem persists: students are taught and examined in English or French. Often languages they do not fully speak at home, which creates a cognitive barrier before they even encounter the subject material.

Where AI is being applied

AI is addressing this problem along three lines:

- Personalised learning pathways that adjust to individual student pace.

- Language-bridge tools that help students transition from mother-tongue instruction to English or French for exams.

- And AI tutoring systems that can provide one-to-one instruction at scale in under-resourced classrooms.

Kenya leads deployment activity, where generative AI has produced documented improvements in academic performance and engagement. Additionally, the Masakhane language infrastructure — speech recognition and translation models for African languages — is directly applicable to building effective mother-tongue educational tools.

The caveat is important: the evidence base remains thin. Most of what is described as “AI in African education” in 2026 is small-scale, externally funded, and not yet at the scale required to move national learning outcomes.

The sector is worth watching closely, but it should be watched with the same rigour applied to healthcare: deployment matters more than pilot, and evidence matters more than announcement.

The data labelling economy: Africa’s hidden AI role

The human layer no one talks about

A dimension of Africa’s relationship with AI does not appear in startup landscape reports or investment trackers. A significant proportion of the human labour powering the global AI boom runs out of Nairobi, Lagos, and Accra. Workers annotating images, labelling training data, moderating content, and refining model outputs for companies headquartered in California.

This is not a peripheral activity. Data labelling, content moderation, and RLHF (reinforcement learning from human feedback) are not automated processes. Every AI system deployed at scale requires large numbers of human workers making fine-grained judgements about what is correct, harmful, or appropriate.

Global AI companies have discovered that this work costs less in Kenya than in Kansas, and the result is a substantial industry operating largely outside public view.

Sama, a San Francisco-based firm with offices near Nairobi’s Sameer Business Park, employs over 3,000 workers in Kenya. Documents revealed that OpenAI agreed to pay Sama $12.50 per hour per worker; however, workers themselves received between $1.32 and $2 per hour after tax.

Remotasks, operated by Scale AI, employed thousands of Kenyan workers on similar terms before abruptly shutting down its Kenya operations in March 2024, locking all workers out of their accounts with a last-minute email.

The conditions on the ground

When 185 Kenyan content moderators working for Meta through Sama attempted to unionise and demand better conditions, the company fired them. These former moderators are now suing Meta and Sama in Kenyan courts, alleging unlawful termination, exploitative working conditions, lack of mental health support, and meager pay.

A 2025 Equidem survey of 76 workers from Colombia, Ghana, and Kenya documented 60 independent incidents of psychological harm — including anxiety, depression, PTSD, and substance dependence — directly attributed to the content workers processed. Additionally, workers reported forced unpaid overtime, no fixed salary, and companies withholding payments.

In response, Kenyan workers founded the Data Labelers Association (DLA), organising for fair pay, mental health support, and an end to draconian non-disclosure agreements. The DLA’s existence is significant: it represents both a recognition that the current arrangement is extractive and a refusal to accept that it must be permanent.

The structural question

The “digital sweatshop vs. skills ladder” debate is real but not binary. Data labelling work provides income, exposure to AI systems, and in some cases a genuine entry point to higher-tier roles. The question is whether the industry, as currently structured, facilitates that progression or indefinitely maintains a low-cost labour pool. The evidence points more toward the latter.

Kenya’s national AI strategy is the only one in Africa to directly acknowledge the issue, noting that “many Kenyans work in AI but remain stuck in bottom-of-pyramid and entry-level jobs such as data annotation.” It names Sama explicitly. Nevertheless, the strategy offers no concrete mechanism to change the dynamic — it notes the problem and does not solve it.

The structural leverage, if any exists, lies in the AfCFTA framework and in national digital labour regulations. Several African AI governance analysts have argued that regional bodies like the AU should establish binding directives around data labourer rights, similar to the EU Platform Work Directive of 2024. Whether the political will for this exists remains uncertain.

The structural barriers: an honest accounting

The compute deficit

Africa holds less than 1% of global compute capacity. Training any reasonably sized language model requires either purchasing cloud time from foreign providers — in hard currency, at latency, against terms of service designed for American enterprise customers — or waiting for hyperscaler infrastructure to expand into African regions.

As a result, African AI development will, for the foreseeable future, concentrate at the fine-tuning and application layer rather than the foundation model layer.

The data problem

Most African languages and contexts remain underrepresented in global training datasets. Common Crawl — the largest web archive used in AI training — is estimated to be over 50% English by volume.

Creating quality training data for a low-resource language requires linguists, annotators, recording infrastructure, and careful methodology. The African Next Voices project is currently recording speech data across Kenya, Nigeria, and South Africa in multiple language families. This is important and underfunded work.

Regulatory fragmentation

Fifty-four countries means fifty-four potential regulatory regimes. For an AI company trying to sell a product across the continent, this creates compliance overhead that simply does not exist for a company operating in the European Union.

The AfCFTA Digital Trade Protocol is the structural solution, but it has not yet entered into force.

Currency and payment infrastructure

This barrier receives far less attention than it deserves. Paying for cloud compute, API access, and AI tooling requires US dollars. Most African founders earn revenue in local currencies with limited hard-currency access.

In Nigeria, accessing foreign exchange to pay a cloud bill has, at various points, been genuinely difficult regardless of the founder’s ability to pay.

This is not an AI-specific problem, but it hits AI startups harder than most because their infrastructure costs are more cloud-intensive.

Limitations

Startup funding data is self-reported and inconsistently disclosed across markets. Francophone African data coverage is improving but remains less comprehensive than East and West African Anglophone data.

Policy tracker assessments draw on publicly available documents; unpublished draft frameworks are not included. Chinese infrastructure deployment figures are estimates derived from open-source research and may undercount actual deployment.

Key terms

LLM — Large Language Model. The type of AI powering tools like ChatGPT. Trained on enormous text datasets to generate, translate, and reason with language. Training one requires significant compute. Notably, most African builders are fine-tuning existing models rather than training from scratch — an important distinction.

SLM — Small Language Model. A leaner, task-specific model that runs on constrained hardware, including edge devices. For most African deployments, SLMs are not a compromise — they are the strategy. Faster, cheaper, and capable of running without cloud connectivity.

AfCFTA — African Continental Free Trade Area. A continental trade bloc covering 54 countries. Its Digital Trade Protocol, currently being ratified, governs cross-border data flows, AI product licensing, and model deployment.

Compute — shorthand for the GPU clusters needed to train and run AI models. Africa has less than 1% of global capacity.

Load-shedding — South Africa’s term for scheduled power cuts by state utility Eskom, used to prevent total grid collapse. Structurally fragile even in periods of reduced frequency.

Edge AI — AI running directly on a device rather than requiring server connectivity. Essential for the roughly 40% of Africans still offline.

Digital Silk Road — China’s programme of digital infrastructure investment across the developing world, delivered through state-backed companies including Huawei and ZTE.