The “intelligence” of a Large Language Model is often discussed as something ethereal—a cloud-based miracle of code and logic. Yet, the physical infrastructure required to sustain the AI revolution is tethered to the earth by a massive, complex, and increasingly volatile supply chain.

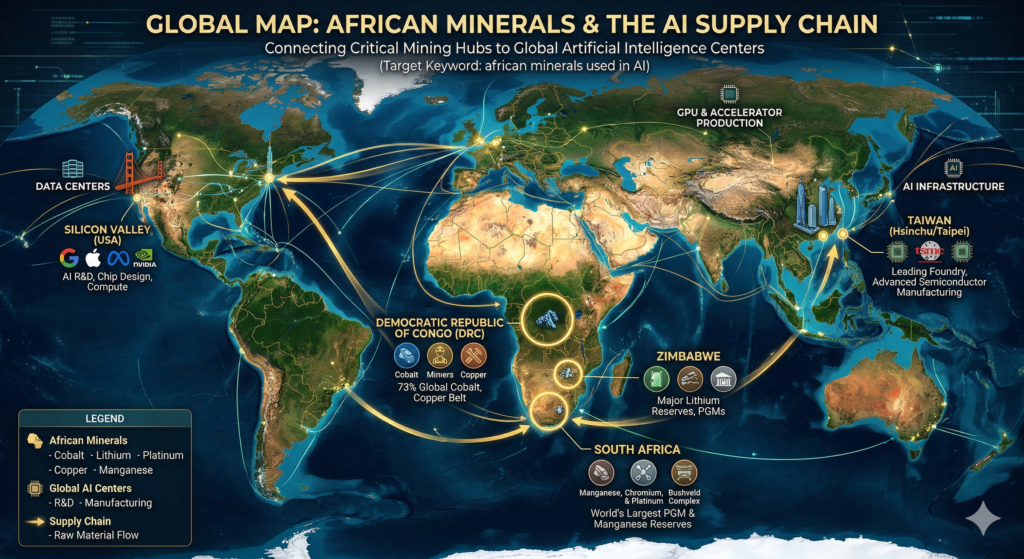

To build a single NVIDIA H100 GPU, the global tech industry relies on a geological mosaic that stretches across the African continent: cobalt from the Democratic Republic of Congo, platinum from South Africa’s Bushveld Igneous Complex, and lithium from the emerging spodumene mines of Zimbabwe.

Africa holds over 30% of the world’s critical mineral reserves, making the continent the load-bearing infrastructure for the 21st-century compute race. However, a profound paradox remains: while African minerals are indispensable to the AI hardware stack, the continent has historically been excluded from the economic “downstream” value of the technology it enables.

As global powers race to secure “AI-ready” supply chains, a new era of resource nationalism, artisanal mining reform, and AI-driven geological prospecting is fundamentally reshaping the map.

This guide serves as a comprehensive, quarterly-updated hub for understanding the African minerals used in AI. From the thermal management properties of South African PGMs to the battery-grade lithium processing shifts in Harare, we trace the journey of raw ore from African soil to the server racks of the world’s most powerful data centers.

I. The Supply Chain Behind the AI Revolution

NVIDIA didn’t buy cobalt from the DRC. They bought HBM chips from SK Hynix. SK Hynix bought from a South Korean refiner. That refiner sourced from a Chinese trading house. The trading house bought from a négociant in Kolwezi. The négociant bought from a man with a hand shovel. That is the supply chain.

A single NVIDIA H100 GPU — the workhorse of the current AI infrastructure build-out — contains materials traceable, with varying degrees of difficulty, to at least six African countries. This fact is frequently cited in discussions of the AI industry’s resource footprint. It is almost never honestly qualified.

The qualification matters enormously. The H100’s African mineral content is not purchased directly by NVIDIA. It arrives through a chain of transactions so long, and so opaque in its middle sections, that no company at the top of the stack can state with legal certainty where its constituent materials originated.

This is not a corporate evasion. It is a structural feature of how global commodity markets have functioned for decades — and the AI industry’s unprecedented scaling has made the consequences of that structure impossible to ignore.

The global supply chain of African minerals used in AI, connecting the DRC’s cobalt and South African platinum to global semiconductor manufacturing hubs.

The Traceability Score: Defining Our Terms

Throughout this briefing, each mineral is assigned a Traceability Score from 1 to 5. The score reflects how reliably the AI industry can verify the origin and conditions of extraction of that mineral. It is not a measure of ethical performance — it is a measure of informational visibility. Most score badly.

| 5 / 5 | Direct mine-to-OEM contract; third-party verified |

| 4 / 5 | Certified smelter program (RMI RMAP); Tier 1 verified |

| 3 / 5 | Smelter known; country of origin confirmed; mine unknown |

| 2 / 5 | Refined material sourced; pre-refinery origin unverifiable |

| 1 / 5 | Commingled at trading stage; origin unknown |

The majority of African minerals entering AI hardware score 2 or lower. This is the central diagnostic fact of the supply chain. Everything else in this briefing flows from it.

Africa’s Share of the Global Critical Mineral Supply

Africa is not a marginal contributor to the AI hardware stack. It is load-bearing infrastructure.

| Mineral | Primary AI Function | Africa’s Global Share | Key Risk | Traceability |

| Cobalt | Li-ion battery cathodes; data centre UPS systems | ~73% (DRC) | Child labour; Chinese refining monopoly | 2 / 5 |

| Lithium | Battery anodes & electrolytes; edge AI devices | ~6% and rising (Zimbabwe) | Export ban volatility; single-country refining | 2 / 5 |

| Platinum / PGMs | MLCCs; GPU cooling; generator catalysts | ~90% of reserves (South Africa) | Labour strikes; EV demand transition | 3 / 5 |

| Copper | PCBs; power busbars; fibre connectors | ~10% mined (DRC + Zambia) | Infrastructure fragility; price cycles | 3 / 5 |

| Rare Earths | Permanent magnets; cooling fans; wafer polish | 3–5% mined; growing | Undeveloped processing; Chinese offtake | 1 / 5 |

| Bauxite / Al | GPU heatsinks; advanced packaging substrates | ~25% of reserves (Guinea) | Political instability; zero in-country refining | 2 / 5 |

| Tantalum | HBM capacitors; AI server power regulation | ~40% (Rwanda / DRC) | Conflict mineral status; trading opacity | 2 / 5 |

| Antimony | Semiconductor dopants; data centre flame retardants | South Africa: significant reserves | Chinese export controls; supply concentration | 2 / 5 |

| Graphite | Li-ion battery anodes; electrode materials | Major deposits (Mozambique, Tanzania) | 100% Chinese processing dependency | 1 / 5 |

The table above is updated quarterly. Where a mineral scores 1 or 2 on traceability, treat the supply share figure as an estimate with a wide confidence interval — the opacity that makes tracing difficult also makes accurate accounting difficult.

II. The Minerals: A Systematic Analysis

Cobalt — The DRC and the GPU Supply Chain

| QUICK STATS: COBALT | |

| AI Function | Lithium-ion battery cathodes; data centre UPS systems |

| Africa’s Share | ~73% of global mine supply |

| Key Countries | DRC (Katanga Belt — Kolwezi, Likasi) |

| Primary Risk | Artisanal mining / child labour; 80%+ of refining in China |

| Traceability Score | 2 / 5 |

| Current Quarter Price | ~$28,000–$35,000 / tonne (cathode-grade) |

Why Cobalt Is Central to AI Hardware

No mineral better illustrates both Africa’s indispensability to AI and its structural exclusion from AI’s rewards than cobalt. Most significantly, the Democratic Republic of Congo accounts for roughly 73 percent of global cobalt mine production.

The Katanga Mining Belt — a geological formation running through the provinces of Lualaba and Haut-Katanga — is, in the medium term, effectively irreplaceable.

In terms of hardware function, cobalt’s primary role is as a cathode material in lithium-ion batteries. Consequently, every AI-capable laptop, every smartphone running an on-device language model, and every data centre’s uninterruptible power supply system relies on cobalt chemistry.

An AI-capable consumer device contains 5 to 30 grams of cobalt; a utility-scale data centre UPS bank, by contrast, may contain several tonnes.

How the Supply Chain Actually Works

To understand why traceability is so difficult, it helps to follow the chain step by step. Cobalt ore is mined in Katanga, either by large industrial operations — Glencore’s Kamoto mine, China Molybdenum’s Tenke Fungurume — or by artisanal and small-scale miners.

It is then purchased by local traders called négociants, aggregated, and exported primarily to Chinese smelters in Guangdong and Zhejiang provinces, where it is refined into battery-grade cobalt sulphate or cobalt metal. From there it moves to cathode precursor manufacturers, subsequently to battery cell producers in South Korea, Japan, and China, then to device assemblers, and finally to OEMs.

A mineral traceability tag on a cobalt shipment in the DRC to monitor the AI supply chain for ethical sourcing.

The Traceability Ceiling

By the time an AI company like NVIDIA, Google, or Microsoft encounters cobalt, it is embedded in a component purchased three or four transactions downstream from the refinery. As a result, there is no commercially viable mechanism by which these companies can currently guarantee that their cobalt supply excludes material from artisanal mines using child labour. This is not a hypothetical risk; rather, it is a documented reality confirmed by UNICEF, Amnesty International, and the International Peace Information Service (IPIS).

| → DEEP DIVE Cobalt and the DRC: Inside the GPU Supply Chain A granular mapping of how cobalt moves from an artisanal mine in Kolwezi to a GPU cluster in a Silicon Valley data centre — including the five commercial transactions that make direct attribution structurally impossible. |

Lithium — Zimbabwe and the Battery-AI Convergence

| QUICK STATS: LITHIUM | |

| AI Function | Battery anodes & electrolytes; data centre UPS backup; edge AI devices |

| Africa’s Share | ~6% of global supply; rapidly growing |

| Key Countries | Zimbabwe (Arcadia, Bikita deposits); also Mali, Namibia |

| Primary Risk | Export ban volatility; complete refining dependency on China |

| Traceability Score | 2 / 5 |

| Current Quarter Price | ~$12,000–$18,000 / tonne (spodumene concentrate) |

Zimbabwe’s Strategic Position

Zimbabwe’s emergence as a significant lithium producer is one of the most consequential supply chain developments of the decade — and, moreover, one of the most instructive case studies in the persistent gap between mineral wealth and economic sovereignty.

The Arcadia lithium deposit near Harare and the Bikita polymetalite deposit in Masvingo province rank among the largest in Africa. Taken together, they represent a resource base of genuine strategic significance.

The Export Ban Experiment

In 2022, the Zimbabwean government imposed a ban on raw lithium ore exports, requiring at minimum concentration before export and signalling an ambition to move toward full in-country processing. It was a bold policy intervention with a clear logic: if Zimbabwe must supply the world’s batteries, it should accordingly capture more than mining royalties for doing so.

However, the results have been mixed. Chinese firms — specifically Zhejiang Huayou Cobalt and Sinomine Resource Group — moved quickly to establish processing partnerships that technically satisfied the ban’s requirements while ensuring the refined product still flows primarily to Chinese battery manufacturers. The policy lever exists; the economic infrastructure to fully exploit it does not yet.

The AI Infrastructure Demand Driver

The AI dimension is more direct than is commonly recognised. The surge in data centre construction globally has, in turn, driven substantial growth in demand for battery backup capacity.

Every hyperscale data centre — the facilities running the inference workloads of ChatGPT, Gemini, and Claude — requires megawatt-hours of lithium battery backup for continuous operation.

As a result, lithium demand is no longer driven solely by electric vehicles; AI infrastructure has become a material demand driver in its own right, one that is accelerating rather than plateauing.

| → DEEP DIVE Zimbabwe’s Lithium and the Battery-AI Convergence An examination of whether Zimbabwe’s export ban is working — and what the country’s lithium ambitions mean for the geography of AI infrastructure finance. |

Platinum Group Metals — South Africa and AI Chip Cooling

| QUICK STATS: PLATINUM / PGMS | |

| AI Function | MLCCs; GPU thermal management; diesel generator catalysts in data centres |

| Africa’s Share | South Africa holds ~90% of known global platinum reserves |

| Key Countries | South Africa (Bushveld Igneous Complex) |

| Primary Risk | Major labour disputes; diesel-to-EV demand transition suppressing prices |

| Traceability Score | 3 / 5 |

| Current Quarter Price | Platinum: ~$950–$1,050 / troy oz; Palladium: ~$950–$1,100 / troy oz |

The Geology Behind the Monopoly

South Africa’s Bushveld Igneous Complex is one of the most remarkable geological formations on earth. Stretching across Limpopo and North West provinces, it contains approximately 90 percent of the world’s known platinum reserves alongside substantial quantities of palladium, rhodium, iridium, and ruthenium.

Despite their significance, these platinum group metals (PGMs) are embedded in the AI hardware stack in ways that receive almost no attention in mainstream supply chain discussions.

Specific Applications in AI Hardware

In AI-specific applications, the connections are more numerous than commonly assumed. Palladium and platinum feature in multi-layer ceramic capacitors (MLCCs), which are present in the thousands in every GPU and server motherboard. Platinum-based materials additionally appear in thermal interface compounds used in high-performance chip packages.

Furthermore — and perhaps most directly — every diesel generator deployed for data centre backup power requires a catalytic converter containing platinum group metals. This last application alone makes PGMs structurally essential to data centre operations worldwide.

Thermal Pressure and Growing Demand

As GPU thermal envelopes continue to expand — the NVIDIA H100 draws 700 watts; the B200 approaches 1,000 watts per chip — cooling architecture has consequently become an increasingly critical engineering challenge.

Advanced cooling systems, including immersion cooling and direct liquid cooling components, contain PGM-derived materials in their thermal management subsystems. The practical implication is that rising AI compute density drives rising PGM demand per data centre built.

A Distinctive Risk Profile

South Africa’s PGM sector, however, carries a risk profile that is fundamentally different from cobalt or lithium. Rather than geopolitical instability, the primary threat to supply continuity is industrial: the sector has experienced repeated, prolonged strikes — including a five-month work stoppage in 2014 — driven by disputes between mining companies and unions including AMCU and NUM.

Accordingly, any serious modelling of AI hardware supply chain resilience must explicitly account for South African labour relations rather than treating the Bushveld as a stable supplier.

| → DEEP DIVE South Africa’s Platinum and AI Chip Cooling Systems A technical examination of PGM applications in H100/B200 GPU cooling architectures, and what the Bushveld’s labour disputes mean for data centre supply chain resilience. |

Copper — Zambia and the Fibre-Optic Backbone

| QUICK STATS: COPPER | |

| AI Function | PCB traces; data centre power busbars; server interconnects; fibre cable hardware |

| Africa’s Share | ~10% of global production (DRC + Zambia Copperbelt) |

| Key Countries | Zambia; DRC (shared Copperbelt province) |

| Primary Risk | Infrastructure fragility; chronic load-shedding; price volatility |

| Traceability Score | 3 / 5 |

| Current Quarter Price | ~$8,500–$9,500 / tonne |

The Omnipresence of Copper in AI Infrastructure

Copper is, in the most literal sense, the connective tissue of AI infrastructure. It is present in every printed circuit board, every power busbar delivering electricity to server racks, every interconnect linking GPU clusters, and the physical hardware of the fibre-optic cable networks carrying AI-generated data between data centres and end users.

Unlike more specialised minerals, there is currently no substitute for copper across these applications at comparable cost or conductivity.

The Scale of Hyperscale Demand

To understand the magnitude of demand, consider that a single large data centre can require upward of 40 million pounds of copper wiring.

As AI clusters scale further — the largest current deployments involve hundreds of thousands of GPUs — copper intensity per unit of compute does not decrease; if anything, advanced power delivery architectures increase it.

The Copperbelt’s output, therefore, is not merely relevant to AI — it is structurally required for AI infrastructure growth.

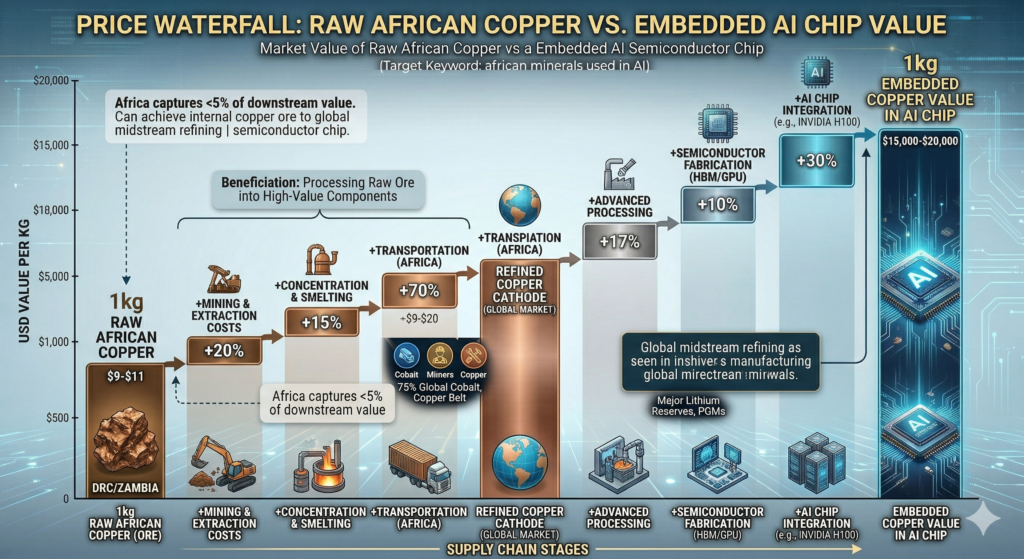

Contrast the raw African copper ore with the value of refined copper when embedded in an advanced AI semiconductor chip (e.g., an H100 GPU).

The Value Chain Paradox

Zambia and the DRC’s shared Copperbelt province is the geographic anchor of African copper production. Zambia alone produces 800,000 to 900,000 tonnes annually.

Yet, despite this scale, Zambia’s copper is exported primarily as blister copper or concentrate, with refining and fabrication occurring outside the continent.

The resulting irony is stark: the country that produces the cable hardware enabling internet access across sub-Saharan Africa — and therefore access to AI services — captures only the first and lowest-value stage in that entire chain.

| → DEEP DIVE Zambia Copper: The Fibre-Optic Backbone of African AI Tracing Zambian mine output through to a server rack in a Lagos data centre — and why Zambia’s copper story is the clearest illustration of the value chain gap. |

Rare Earth Elements — Tanzania and Madagascar

| QUICK STATS: RARE EARTH ELEMENTS | |

| AI Function | Permanent magnets in cooling fans & hard drives; wafer polishing compounds |

| Africa’s Share | 3–5% mined globally; growing fast |

| Key Countries | Tanzania (Ngualla deposit); Madagascar (Toliara); Malawi; Namibia |

| Primary Risk | Undeveloped processing; Chinese processing monopoly (~85%); offtake concentration |

| Traceability Score | 1 / 5 |

| Current Quarter Price | Mixed basket: Neodymium ~$60–$80/kg; Dysprosium ~$250–$300/kg |

How Rare Earths Enter AI Hardware

Rare earth elements are the hidden substrate of AI’s physical infrastructure. Specifically, neodymium, dysprosium, terbium, and praseodymium are essential for the permanent magnets powering every cooling fan in every server rack — at hyperscale facilities, this represents millions of individual motors running continuously.

In addition, cerium and lanthanum appear in the polishing compounds used to finish semiconductor wafers at the nanometre precision that advanced chip manufacturing requires. Both applications are, in the near term, irreplaceable.

East Africa’s Emerging Deposits

Tanzania’s Ngualla deposit, operated by Peak Rare Earths, is among the world’s highest-grade rare earth carbonatite formations. Similarly, Madagascar’s Toliara project, developed by Base Resources in partnership with Energy Fuels, holds significant monazite and xenotime deposits. These are genuinely world-class resources.

Nevertheless, they score 1 out of 5 on traceability — not because of ethical failures, but because the processing infrastructure does not yet exist in Africa to produce finished rare earth oxides. As a result, virtually all material must be shipped to China for separation and processing before it can enter the supply chain.

The Strategic Stakes

The geopolitical stakes here are higher than for any other mineral in this analysis. China controls approximately 85 percent of global rare earth processing, which means that even deposits located outside China feed back into Chinese industrial capacity.

African deposits, if developed with in-country processing facilities, would therefore represent the single most significant opportunity to diversify a supply chain that Western governments and technology companies have already identified as a critical vulnerability.

Whether that development ultimately happens — and who captures the resulting economic value — will be determined by investment decisions being made in the period 2024 to 2030.

| → DEEP DIVE Rare Earths in Tanzania and Madagascar — What’s at Stake What makes the Ngualla deposit different, whether Western buyers can outbid Chinese offtake agreements, and the decade-long investment required to build African rare earth processing capacity. |

Bauxite — Guinea and the Aluminium-Semiconductor Link

| QUICK STATS: BAUXITE / ALUMINIUM | |

| AI Function | GPU heatsinks; server chassis; aluminium nitride substrates in advanced packaging |

| Africa’s Share | Guinea holds ~25% of known global reserves (~25 billion tonnes) |

| Key Countries | Guinea (Sangaredi, Boké region) |

| Primary Risk | Military coup instability; zero in-country alumina refining; Chinese investment concentration |

| Traceability Score | 2 / 5 |

| Current Quarter Price | Bauxite: ~$35–$55 / tonne (FOB Guinea) |

Guinea’s Reserve Dominance

Guinea holds the world’s largest bauxite reserves — approximately 25 billion tonnes, representing roughly one quarter of the global total. Over the last decade, production has expanded dramatically, with output exceeding 100 million tonnes annually.

This growth has been driven overwhelmingly by Chinese investment and Chinese demand, establishing a dependency relationship that mirrors patterns seen elsewhere across Africa’s mineral sector.

Advanced Packaging: The Emerging AI Connection

In AI hardware, aluminium’s most important emerging application is not the heatsink or chassis — familiar uses that have remained stable for decades — but rather advanced chip packaging. As NVIDIA, AMD, and Intel move toward 2.5D and 3D chiplet architectures, aluminium nitride ceramics play an expanding role as substrates and thermal spreaders.

These are precision materials derived from the same bauxite-to-aluminium pipeline that begins in Guinea’s Boké region. Furthermore, as packaging becomes more complex with each GPU generation, this application is growing in significance.

Political Risk and the Processing Gap

Guinea’s political context is, however, inseparable from its mineral story. The 2021 military coup that removed President Alpha Condé created immediate uncertainty about existing mining agreements and future investment conditions.

Beyond political instability, the infrastructure required to build alumina refining capacity in-country — road, rail, port, and power — remains severely underdeveloped relative to the deposit scale. Consequently, Guinea is the archetype of a country with exceptional mineral endowment and minimal structural capacity to capture downstream value from it.

| → DEEP DIVE Guinea’s Bauxite and the Aluminium-Semiconductor Link The bauxite-to-aluminium-to-AI-chip pipeline in full, and why advanced packaging is changing the demand equation for a mineral most technologists have never considered. |

Tantalum — Rwanda, DRC, and the HBM Power Problem

| QUICK STATS: TANTALUM | |

| AI Function | Capacitors in High-Bandwidth Memory (HBM); power delivery regulation in AI accelerators |

| Africa’s Share | ~40% of global mine supply (Rwanda ~25%, DRC ~15%) |

| Key Countries | Rwanda; eastern DRC |

| Primary Risk | Conflict mineral classification; Chinese trading house dominance; iTSCi compliance gaps |

| Traceability Score | 2 / 5 |

| Current Quarter Price | ~$150–$180 / kg (tantalite concentrate) |

The HBM Architecture Connection

Tantalum is the supply chain story that the AI industry has not yet been forced to tell — but will be. Its connection to AI hardware runs specifically through one of the most consequential recent developments in chip architecture: High-Bandwidth Memory.

HBM — the stacked DRAM technology sitting atop the GPU die in NVIDIA’s A100, H100, and H200 chips — is what enables AI accelerators to move data between memory and compute fast enough for large model inference and training.

HBM2e, HBM3, and HBM3e are manufactured almost exclusively by SK Hynix, Samsung, and Micron. Each HBM stack contains dozens of tantalum electrolytic capacitors providing stable power delivery across the extreme thermal cycles of sustained AI workloads.

At data centre scale — tens of thousands of H100 GPUs in a single facility — tantalum demand is therefore material and growing with each new GPU generation.

Rwanda’s Transparency Model

Rwanda has, notably, constructed the most transparent tantalum supply chain in Africa, anchored by the iTSCi (ITRI Tin Supply Chain Initiative) mineral tagging and bagging system. As a result, Rwandan tantalum scores better on traceability than most African minerals.

And yet it still scores only 2 out of 5 — because the midstream trading layer, dominated by Chinese trading houses, remains opaque. Additionally, the conflict mineral classification imposed by Section 1502 of the US Dodd-Frank Act paradoxically suppressed investment in legitimate Rwandan operations while simultaneously driving some supply underground.

The Eastern DRC Problem

Eastern DRC’s tantalum presents a sharply contrasting picture. Often extracted alongside cassiterite in zones of active or recent armed conflict, it represents the opposite end of the risk spectrum from Rwanda’s iTSCi-tagged material. Critically, however, the two streams commingle in the trading layer before reaching Asian component manufacturers.

No HBM manufacturer can currently guarantee complete separation between these origin streams — a gap that regulators in both the EU and US are beginning to address, though enforcement timelines remain unclear.

| → DEEP DIVE Tantalum, HBM, and Africa’s Most Transparent Supply Chain A technical deep-dive into tantalum’s role in AI accelerator power architecture, Rwanda’s iTSCi system, and why Dodd-Frank’s unintended consequences still shape this supply chain. |

Antimony — South Africa and the Overlooked Semiconductor Input

| QUICK STATS: ANTIMONY | |

| AI Function | Semiconductor dopants (GaSb); flame retardants in data centre cabling & PCB laminates |

| Africa’s Share | South Africa holds significant reserves; global supply highly concentrated |

| Key Countries | South Africa (Limpopo — Consolidated Murchison area) |

| Primary Risk | Chinese export restrictions (2024); supply concentration; minimal African processing |

| Traceability Score | 2 / 5 |

| Current Quarter Price | ~$12,000–$16,000 / tonne (elevated post-2024 restrictions) |

A 2024 Warning Shot

In 2024, China imposed export restrictions on antimony — the first major non-rare-earth mineral subject to Chinese export controls. The response across procurement departments at technology companies was instructive: almost none had flagged antimony as a supply chain risk.

The price spiked immediately. Sourcing teams were, in many cases, scrambling to identify alternative suppliers for the first time. The pattern is worth studying closely, because it is almost certainly a template for how China will apply mineral leverage going forward.

Two Distinct Roles in AI Infrastructure

Antimony’s role in AI hardware actually operates through two distinct and largely independent channels. The first is as a semiconductor dopant: gallium antimonide (GaSb) is a compound semiconductor used in infrared sensors and specialised AI edge hardware for thermal imaging and environmental sensing applications.

The second channel — and the more pervasive — is as a flame retardant synergist. Antimony trioxide is a critical component of the halogenated flame retardants applied to data centre cabling, server rack insulation, and the laminates of printed circuit boards throughout AI infrastructure.

South Africa’s Position and the Broader Template

Every major data centre build, as a consequence, contains antimony in its fire suppression material stack. At hyperscale — facilities with hundreds of megawatts of installed capacity — this is a meaningful and non-trivial quantity.

South Africa’s Limpopo province hosts reserves at the historic Consolidated Murchison mine, and while production has fluctuated with price cycles, the reserves are real and accessible.

The broader lesson of the 2024 restrictions, however, extends beyond antimony itself. China has now demonstrated both the willingness and the institutional mechanism to restrict exports of minerals that Western supply chain analysts had classified as second-tier.

Germanium and gallium restrictions preceded antimony; graphite controls followed. The trajectory, taken together, suggests a systematic expansion of Chinese mineral leverage — one that has no obvious natural limit and that will likely continue to surface minerals previously overlooked by AI hardware procurement teams.

| → DEEP DIVE Antimony: The AI Industry’s Next Supply Shock A post-mortem on the 2024 Chinese export restrictions and a forward analysis of which African antimony reserves could provide alternative supply — and on what timeline. |

III. Cross-Cutting Themes: The Systemic Analysis

Who Benefits? The AI Value Pyramid and Africa’s Revenue Gap

The gap between Africa’s role in the AI supply chain and its share of AI’s economic value is not a marginal oversight. It is the defining feature of the relationship. The following analysis makes it concrete.

The AI Value Pyramid

Consider cobalt — the mineral with the longest documented African supply chain footprint. The arithmetic is deliberately stark:

| LAYER 3 — Silicon Valley 1,000x multiplier on raw ore value | NVIDIA H100 GPU | ~$30,000–$40,000 per unit | Weight: ~4.4 kg | Cobalt content: ~0.5–1 kg equivalent |

| LAYER 2 — Chinese Refinery Processing adds ~40% over mine-gate price | Refined Cobalt Metal | ~$50,000 per tonne | Midstream processing captures the first margin step |

| LAYER 1 — DRC Mine Gate Base reference: 1x value | Raw Cobalt Ore / Concentrate | ~$35,000 per tonne | Africa’s capture point in the chain |

Africa captures the value at Layer 1. The ~1,000x multiplier between mine-gate cobalt and finished GPU accrues almost entirely outside the continent.

This is not, in isolation, a story of exploitation — value genuinely is created in design, fabrication, and software. But it does make the frequent claim that African mineral wealth positions the continent to benefit from the AI boom sound, at minimum, premature.

Beneficiation: The Missing Middle

The gap is not filled by royalties or taxation alone. The structural solution — moving African mineral economies up the value chain through domestic processing, or beneficiation — is technically achievable but requires sustained policy consistency, energy infrastructure, and patient capital. All three are in short supply.

Zimbabwe’s lithium export ban is the most aggressive recent attempt. The DRC’s ambitions for local cobalt refining at the Kamoa-Kakula processing complex are genuine but early-stage.

Tanzania and Namibia are positioning for battery value chain investment under the African Continental Free Trade Area (AfCFTA) framework. These are real policy movements. They are also, on the timeline of global AI infrastructure build-out, slow.

| → DEEP DIVE Who Benefits? Mineral Wealth vs. Revenue Capture in Africa A country-by-country analysis of royalty structures, export tax regimes, and beneficiation policies — and a frank assessment of which initiatives are advancing and which remain aspirational. |

The Energy Paradox: Green AI, Dirty Mining

Every major AI company has published a net zero or carbon neutrality commitment. Microsoft has pledged to be carbon negative by 2030.

Google committed to operating on 24/7 carbon-free energy across all its data centres. Amazon Web Services targets 100 percent renewable energy by 2025. These commitments are, within their defined scope, largely credible.

Their defined scope is the problem.

The Scope 3 Blind Spot

Corporate carbon accounting distinguishes between Scope 1 emissions (direct, from owned operations), Scope 2 (indirect, from purchased electricity), and Scope 3 (all other indirect emissions across the value chain, including those from the production of purchased goods and services).

The net zero commitments invariably cover Scope 1 and 2. They do not, however, in almost all cases, extend meaningfully to Scope 3 Category 1 — the emissions generated by mining and processing the minerals that make the hardware possible in the first place.

Those upstream emissions are, in fact, substantial. Consider the energy context at the mine:

| Country / Mineral | Primary Energy Source at Mine | Carbon Implication |

| DRC (Cobalt) | Diesel generators; unreliable grid | ~2.5–3x grid renewable carbon intensity |

| Guinea (Bauxite) | Almost entirely diesel | Grid access minimal in mining zones |

| Zimbabwe (Lithium) | Diesel at remote spodumene sites | Grid available in cities; not mine sites |

| South Africa (PGMs) | ~85% coal-powered national grid | One of the highest coal-grid dependencies globally |

| Zambia (Copper) | Grid + chronic diesel backup | Load-shedding forces diesel fallback |

The Practical Implication

The implication is not merely that AI companies are failing an accounting test. Rather, it is that an industry marketing itself on environmental credentials has drawn a boundary around its carbon footprint that excludes the most carbon-intensive stage of its physical supply chain.

Diesel-powered mining produces approximately 2.5 to 3 times the CO₂ per unit of energy compared to grid electricity from renewable sources — meaning that the African mining operations feeding AI hardware are, in aggregate, among the highest-carbon mineral extraction operations in the world.

The Leading Edge of Better Practice

There is, nonetheless, a leading edge of better practice beginning to emerge. Apple has started imposing supplier-level energy transition requirements as conditions of component offtake agreements — in effect, making renewable energy adoption a commercial prerequisite for supplying into Apple’s hardware stack.

This is the direction the norm should move. It is not yet the norm across the AI industry more broadly, and without regulatory pressure or competitor action, the pace of adoption is unlikely to accelerate on its own.

| → DEEP DIVE The ESG Contradiction: ‘Green AI’ and Diesel Mining A Scope 3 audit of the AI industry’s upstream carbon footprint — and what honest climate accounting would look like for a sector that runs on African minerals extracted with diesel power. |

AI Geological Mapping: Digital Colonialism or African Advantage?

There is a feedback loop at the heart of the AI minerals story that has received insufficient analytical attention: AI systems are now being deployed to discover and optimise the extraction of the minerals needed to build more AI.

What AI Geological Mapping Does

Modern AI prospecting integrates satellite multispectral imagery, legacy seismic datasets, drone-based hyperspectral surveys, and historical geological survey records into machine learning models that predict subsurface mineral deposits with precision unavailable to human geologists working from conventional methods.

KoBold Metals — backed by investors including Bill Gates and Jeff Bezos — has applied this methodology in Zambia and the DRC, where its models contributed to the identification of the Mingomba copper deposit, one of the largest undeveloped copper finds in recent years.

The Data Sovereignty Problem

If an AI model trained on public Tanzanian geological survey data discovers a billion-dollar deposit, who owns the digital twin of that land?

This question has no legal answer in most African jurisdictions, because the scenario did not exist when mining legislation was written. It has an economic answer, which is less comfortable: the AI model is the property of the firm that built it. The firm files for a mining concession. The government negotiates royalties on a deposit whose existence it learned about from the company that intends to extract it.

The training data for these geological models often includes public national survey archives — in many African countries, geological surveys conducted by colonial administrations and subsequently transferred to national ministries with varying degrees of digitisation and accessibility.

A well-capitalised AI prospecting firm can digitise, clean, and structure this data faster and more comprehensively than an underfunded national geological service. The practical result: a private company’s model may know more about a country’s mineral endowment than the country’s own Ministry of Mines.

This is the dynamic that scholars including Abeba Birhane and Nanjala Nyabola describe as digital colonialism: the deployment of digital infrastructure and AI capability, concentrated in wealthy countries, to extract value from poorer ones — replicating colonial economic structures through technological rather than political means. The term requires precision to be useful. Applied to AI geological prospecting in Africa, the structural fit is exact.

What Would Change the Dynamic

The solutions are technically straightforward even if politically and financially difficult. National AI geological capacity — computational geology training programmes, GPU access for government geological services, and sovereign data infrastructure — would allow African governments to run their own predictive prospecting.

Data licensing frameworks, establishing clear IP terms for commercial use of national geological survey data in AI models, would create revenue streams and negotiating leverage. Neither is currently standard practice in any African jurisdiction.

| → DEEP DIVE AI Geological Mapping: How AI Is Finding Its Own Raw Materials The technology, the actors, the data sovereignty question, and a proposed framework for geological AI licensing that would allow African governments to monetise their own subsurface data. |

Artisanal Mining, Child Labour, and the AI Industry’s Blind Spot

The Scale of Artisanal Mining

Artisanal and small-scale mining (ASM) is not a marginal footnote to Africa’s mineral supply chains. On the contrary, it is estimated to employ between 40 and 45 million people across the continent, providing livelihoods in areas where formal employment alternatives are minimal or non-existent.

In the DRC’s cobalt sector specifically, ASM accounts for approximately 15 to 20 percent of total production by volume — a figure that fluctuates with cobalt prices, which in turn determine whether ASM is economically viable relative to other informal activities.

The Documented Reality of Child Labour

Documented child labour in DRC artisanal cobalt mining is not alleged or speculative. It has been confirmed by multiple independent investigations: UNICEF, Amnesty International, and IPIS have all published field research identifying children working in surface scraping and underground tunnel operations in the Kolwezi and Kailo areas of Lualaba province.

The physical risks are severe and well-documented — they include tunnel collapse, cobalt dust inhalation causing hard-metal lung disease, and exposure to sulphuric acid runoff.

Why the Supply Chain Cannot Self-Correct

The traceability problem is structural rather than attitudinal, which is why voluntary commitments alone have failed to solve it. ASM cobalt enters the formal supply chain through négociants who purchase from individual and small-group miners without systematic age verification.

It is then aggregated with industrial-mined cobalt at trading points before reaching Chinese smelters, where material from multiple origins is commingled in the refining process. Consequently, the AI industry’s Tier 1 suppliers — battery manufacturers in South Korea and Japan — are purchasing refined cobalt sulphate in which the proportion of ASM-origin material is unknown and, under current systems, unknowable.

What Technology Has and Has Not Achieved

Blockchain traceability pilots have been conducted by multiple actors, including Glencore, RCS Global, and several technology company consortia. The honest assessment is that these pilots have demonstrated technical feasibility while failing to achieve commercial scale.

The economic incentives for trading houses to maintain commingled material flows — lower administrative burden, greater price flexibility — continue to outweigh the current pressure to change sourcing practices.

The Regulatory Pressure Building

The most concrete current mechanism for structural change is, in fact, regulatory rather than commercial. The EU’s Corporate Sustainability Due Diligence Directive (CSDDD) and the forthcoming critical minerals supply chain provisions within the Critical Raw Materials Act create binding obligations for EU-headquartered companies and, by extraterritorial effect, their major suppliers.

Nevertheless, these frameworks apply to European companies first — creating an asymmetry with US AI hardware manufacturers who currently face no equivalent binding obligation, and who therefore face less near-term pressure to act.

| → DEEP DIVE Artisanal Mining, Child Labour, and the AI Industry’s Blind Spot A supply chain traceability forensic — how ASM cobalt enters AI hardware despite responsible sourcing commitments, and what regulatory and commercial mechanisms are beginning to close the gap. |

Forward Analysis: What Changes, and When

The Next Minerals Entering the AI Supply Chain

Graphite: The Cobalt Pattern, Repeated

Graphite deserves specific attention because the structural risks mirror cobalt almost exactly. It is the anode material in every lithium-ion battery, and therefore in every AI-capable device and data centre backup system.

Mozambique’s Balama deposit, operated by Syrah Resources, is the largest graphite mine outside China. Tanzania’s Mahenge deposit is moreover among the highest-grade globally.

Both operations, however, export almost entirely as raw flake graphite concentrate — to Chinese facilities that convert it to the spherical graphite required for battery anodes. The processing gap is identical to cobalt. The geopolitical risk is, accordingly, comparable.

Manganese and Nickel: The Next Demand Wave

Manganese is entering the AI supply chain analysis as battery chemistry diversifies. Lithium manganese iron phosphate (LMFP) batteries — a next-generation chemistry promising better energy density than standard LFP while simultaneously reducing cobalt dependency — use substantial manganese.

South Africa holds the world’s largest manganese reserves. Consequently, if LMFP adoption accelerates in data centre UPS applications, South Africa’s manganese position becomes strategically significant in ways that current procurement models do not reflect.

Nickel, used in NMC battery cathodes, is represented by Tanzania’s Kabanga deposit — one of the highest-grade undeveloped nickel sulphide resources globally, currently being developed by Kabanga Nickel with an unusual emphasis on in-country refining.

If the Kabanga development proceeds as planned, it would be among the first African mineral projects to achieve meaningful value chain integration from mine to refined metal within the continent — making it a rare potential exception to the raw-export pattern.

The Geopolitical Realignment

China’s Sequential Export Restrictions Strategy

The Chinese antimony export restrictions of 2024 are best understood not as an isolated trade action but as the clearest signal yet of a systematic strategy to leverage mineral processing dominance as geopolitical currency.

China controls the refining chokepoint for cobalt, lithium, rare earths, graphite, gallium, germanium, and antimony — in other words, for the majority of minerals examined in this briefing.

The pattern of selective export restrictions — escalating from gallium and germanium in 2023, to graphite controls in late 2023, to antimony in 2024 — suggests a deliberate sequencing rather than reactive policy.

Western Policy Responses: Real but Slow

Western policy responses are real but slow, and that gap in timelines matters. The US Inflation Reduction Act’s critical minerals provisions create economic incentives to diversify away from Chinese-processed materials. Similarly, the EU Critical Raw Materials Act sets diversification benchmarks.

The US-DRC-Zambia minerals corridor agreement, signed in 2022, is still in early implementation. These are, however, frameworks rather than facilities. Processing capacity takes five to ten years to build from a standing start, which means that policy commitments made today will not translate into supply chain resilience until the early 2030s.

African Governments as Strategic Actors

African governments, meanwhile, are navigating this realignment with uneven but growing sophistication. The Democratic Republic of Congo, Zimbabwe, and Namibia are all explicitly positioning their mineral endowments as leverage in a great-power competition they did not create and cannot fully control.

The risk, nevertheless, is that this leverage is extracted by the competing powers without African states successfully translating it into processing capacity, technology transfer, or long-term industrial development.

The historical pattern of African resource booms offers limited grounds for optimism; the difference this time is that African governments are, increasingly, aware of that history.

Technology Shifts That Could Redraw the Map

Advanced Packaging: Rising Mineral Intensity

Advanced chip packaging is increasing, not decreasing, the mineral intensity of a unit of AI compute. As NVIDIA moves toward NVLink Switch multi-die architectures, as TSMC advances CoWoS (Chip on Wafer on Substrate) packaging at scale, and as HBM stack heights increase from 8-hi to 12-hi, the per-GPU demand for tantalum capacitors, aluminium nitride substrates, and platinum-group thermal materials rises correspondingly.

The assumption that semiconductor technology will progressively reduce materials dependency is simply not supported by the current trajectory.

Chemistry Shifts: Partial Relief, Not Elimination

Cobalt-free battery chemistries — particularly lithium iron phosphate (LFP) — are, nonetheless, gaining adoption in data centre stationary storage specifically because hyperscalers recognise cobalt supply chain risk. This is a meaningful structural shift that deserves acknowledgment.

It does not, however, eliminate cobalt from the AI supply chain; high-energy-density applications in AI-capable consumer devices continue to require cobalt-containing cathode chemistries. The net effect is a redistribution of cobalt demand across the hardware stack rather than its elimination.

Intelligence Assessment

Africa’s Non-Negotiable Role

Africa is not a peripheral participant in the AI hardware supply chain. It is, rather, the physical foundation upon which the AI industry’s infrastructure rests. Cobalt, lithium, platinum, copper, tantalum, rare earths, bauxite, antimony, and graphite — the minerals analysed in this briefing — cannot be substituted out of AI hardware on any near-term timeline.

The deposits that matter most are in African ground, and that geographic reality is not changing.

Three Structural Gaps That Define the Relationship

Three structural realities, taken together, define the gap between that fact and Africa’s actual economic position in the AI era.

First, the traceability gap. The opacity of midstream refining — concentrated overwhelmingly in China — means that the AI industry’s responsible sourcing commitments are structurally unverifiable at the mineral origin level.

This is not primarily a failure of corporate ethics; it is, instead, a failure of market architecture. Fixing it requires investment in supply chain systems, regulatory enforcement, and in-country processing infrastructure that creates natural traceability checkpoints.

Second, the value capture gap. Africa’s minerals enter a value chain that multiplies their worth by three to four orders of magnitude, with almost all of that multiplication occurring outside the continent.

Export bans, beneficiation requirements, and continental trade frameworks are the policy instruments available to African governments. They are beginning to be deployed. They work, however, slowly against entrenched supply chain relationships and Chinese investment dominance.

Third, the accountability gap. The AI industry’s net zero commitments exclude the most carbon-intensive stage of their physical supply chain. Their responsible sourcing programmes cannot currently guarantee freedom from child labour in artisanal cobalt mining.

Their geological AI tools may, in some cases, know more about African mineral deposits than African governments do. Each of these gaps represents both an ethical failure and — as regulatory frameworks tighten — a material business risk that will eventually demand resolution.

The question behind the target keyword — which african minerals are used in AI — is technically answerable. The harder question, which this briefing has attempted to address, is: on what terms?

A Structural Problem, Not a Villainous Industry

The AI industry is not uniquely villainous in this analysis. The supply chain structures it inherited were built for efficiency, not accountability, across a century of industrial commodity markets.

What is nonetheless distinctive is the AI industry’s scale, the pace of its scaling, and the specificity of its ESG commitments — which together create a measurable gap between stated values and operational reality that is, with each passing quarter, harder to close with language rather than action.

The minerals are African. The question of who ultimately benefits remains, at this point, genuinely open.

Related Intelligence: Spoke Articles in This Series

| → | Cobalt and the DRC: Inside the GPU Supply Chain |

| → | Zimbabwe’s Lithium and the Battery-AI Convergence |

| → | South Africa’s Platinum and AI Chip Cooling Systems |

| → | Zambia Copper: The Fibre-Optic Backbone of African AI |

| → | Rare Earths in Tanzania and Madagascar — What’s at Stake |

| → | Guinea’s Bauxite and the Aluminium-Semiconductor Link |

| → | Who Benefits? Mineral Wealth vs. Revenue Capture in Africa |

| → | AI Geological Mapping: How AI Is Finding Its Own Raw Materials |

| → | Artisanal Mining, Child Labour, and the AI Industry’s Blind Spot |

Production figures sourced from USGS Mineral Commodity Summaries, World Mining Data, and corporate annual reports. Pricing indicative; verify against current spot data.