The road to 2030 doesn’t run through Silicon Valley; it runs through a 1,200km stretch of red dust in the Central African Copperbelt.

While Washington and Beijing remain locked in a “Chokepoint War” over Pax Silica and semiconductor sovereignty, a new era of African mineral nationalism is quietly rewriting the global trade manual. From the cobalt-rich pits of the DRC to Zimbabwe’s lithium reserves and South Africa’s PGM complexes, the continent is no longer a passive bystander in the energy transition. Every great power is being forced to respond on Africa’s terms.

In 2026, the geopolitical question has shifted: it is no longer about who owns the ground, but who is willing to build the processing and refining infrastructure on African soil.

This deep-intelligence briefing analyzes the 2026 landscape of critical minerals geopolitics in Africa. We examine the structural exclusion of the Pax Silica coalition, the operationalization of the AU Green Minerals Strategy, and how the entry of Gulf sovereign capital and India’s NCMM has turned a binary US-China competition into a complex, multipolar bidding war. For global tech powers, the price of admission to Africa’s minerals is no longer just capital—it is the transfer of technology and the end of the raw-ore export era.

Map of Africa critical mineral deposits 2026 showing the Zambia-DRC Copperbelt and Lobito Corridor infrastructure.

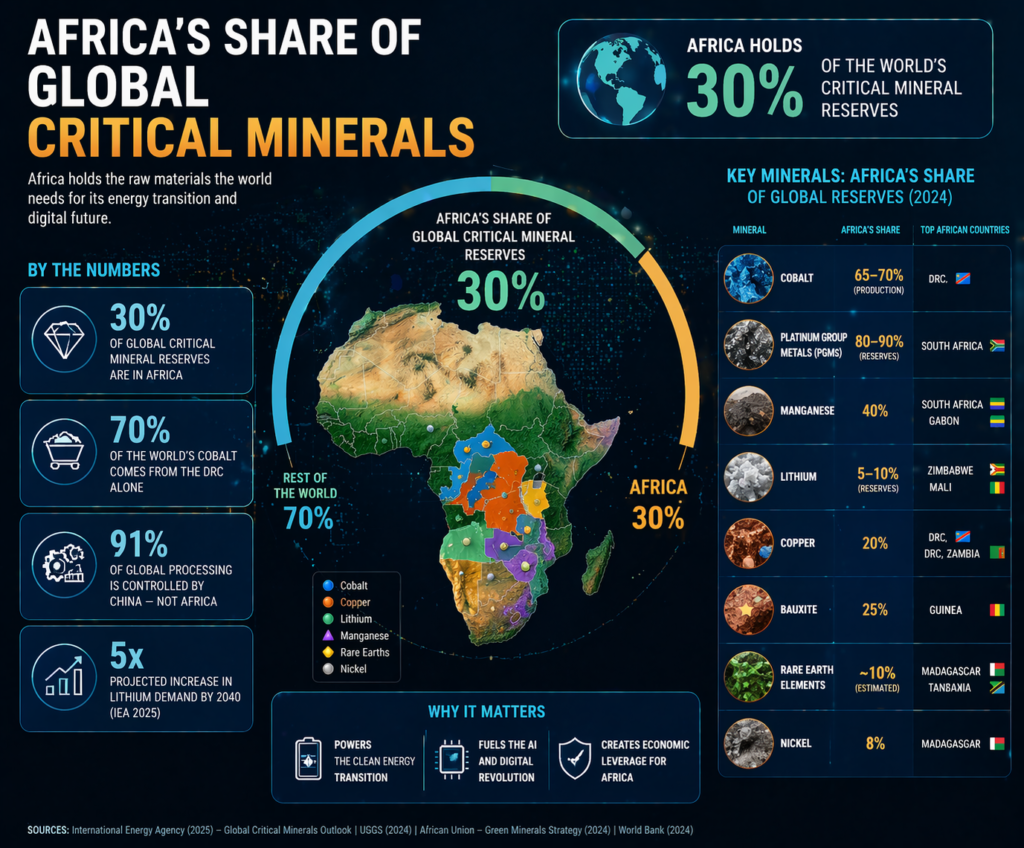

Key Mineral Statistics (2026)

| Statistic | Context & Source |

| 30% | Global critical mineral reserves currently held in Africa |

| 70% | Share of world cobalt supply originating from the DRC alone |

| 91% | Global mineral processing and refining controlled by China |

| 5× | Projected increase in lithium demand by 2040 (IEA 2025) |

The Zambia-DRC Battery Corridor does not yet appear on most geopolitical risk maps. It should. Stretching across the world’s most concentrated battery mineral endowment — the cobalt and copper deposits of Central Africa’s Copperbelt — it represents the first serious attempt by African states to own not just the mine but the manufacturing step that follows it.

When it succeeds, it will be the clearest proof that the critical minerals geopolitics of Africa in 2026 is no longer a story told by outsiders about a passive continent. It is a story about who is setting the terms.

In 2022, Zimbabwe banned the export of raw lithium. In 2023, Namibia outlawed unprocessed mineral exports entirely. In 2025, the Democratic Republic of Congo used cobalt export bans to stabilise global prices and signal market power.

South Africa hosted the G20 presidency and produced the first multilateral framework to formally enshrine local beneficiation as a principle of global mineral governance. These were not reactions to great-power diplomacy. They were the opening moves of a continent that has decided the era of shipping ore abroad and importing value back home is over.

The critical minerals geopolitics of Africa in 2026

The critical minerals geopolitics of Africa in 2026 is most accurately understood as a contest between an assertive, increasingly coordinated Africa and a collection of great powers — the US, China, the EU, the UAE, Saudi Arabia, India, and Russia — whose energy-transition and AI-infrastructure strategies are entirely dependent on what African soil contains.

Each of them wants something different from that soil, and each is finding that the terms of access are being set with increasing confidence by the continent itself.

Africa’s New Mineral Nationalism

The shift began in policy documents and export regulations before it registered in diplomatic cables. Country after country — without a coordinating signal from the African Union — arrived independently at the same conclusion: if the world’s energy transition and AI supply chain cannot function without African cobalt, lithium, copper, manganese, platinum group metals, and rare earth elements, then the terms of extraction need to change.

Namibia and Zimbabwe: Onshore Processing Mandates

Namibia went furthest structurally. Its export ban covers all critical minerals — lithium, cobalt, manganese, graphite, rare earth elements — and its 2025 Minerals Bill requires investors to establish primary processing facilities in-country. A proposal for 51 percent Namibian ownership in all new mining ventures has entered active policy debate.

Zimbabwe’s lithium export restrictions, tightened through 2025 and into 2026, carry the same logic: you can mine here, but you must process here too. The DRC’s temporary cobalt export bans in 2025 stabilized global prices and demonstrated that the continent’s largest mineral producer understands its market power well enough to use it.

South Africa’s G20 Leadership

South Africa’s 2025 Critical Minerals and Metals Strategy goes further, prioritising domestic beneficiation across platinum group metals, manganese, vanadium, and emerging rare earth deposits. At the 2025 G20 summit in Johannesburg — which South Africa hosted as the continent’s first G20 president — the adopted Critical Minerals Framework formally reframed minerals as “drivers of inclusive growth,” not merely supply-chain inputs.

It was the first multilateral document to explicitly place value retention in producing countries as a core principle of global mineral governance.

This is the context in which every external actor must now operate. They are not arriving to a blank-slate resource continent. They are competing to offer terms that increasingly confident African states will accept.

The Mineral Map: Why Africa Cannot Be Substituted

Africa’s leverage in the global mineral supply chain geopolitics of 2026 flows directly from geology that no investment programme or technology roadmap can change on the timescales that matter. The Democratic Republic of Congo accounts for roughly 70 percent of global cobalt production — and no viable large-scale substitute exists before 2035.

South Africa’s Bushveld Complex holds approximately 63 million kilograms of platinum group metal reserves, the vast majority of the world’s known 76 million kilograms — making it irreplaceable for hydrogen technology, catalytic systems, and industrial applications.

Zimbabwe ranks in the global top five for lithium deposits. Guinea possesses roughly a quarter of the world’s bauxite reserves. Zambia sits at the heart of the Copperbelt. East Africa is an emerging concentration of rare earth elements, graphite, and nickel.

Global Demand Trajectories

The IEA’s Global Critical Minerals Outlook 2025 makes the demand trajectory unambiguous: lithium demand will increase fivefold by 2040, graphite and nickel will double, cobalt will be needed in 50 to 60 percent greater quantities. In 2025, one in four new cars sold globally was an electric vehicle.

Minerals that power EVs, store renewable energy, fabricate semiconductors, and run artificial intelligence data centres are, in large part, African minerals. This concentrated supply provides African nations with a structural advantage that other developing regions lack.

The Processing Gap Contest

The structural problem — the one that both the AU Green Minerals Strategy and Africa’s new mineral nationalism are attempting to solve — is that Africa mines the ore and someone else processes it. China controls 60 percent of global mining output and 91 percent of global refining and processing capacity.

African countries export cobalt hydroxide and receive back refined cobalt at a significant markup. The gap between what Africa provides to the global supply chain and what it captures from it is the central political contest of the next decade.

Pax Silica: The Silicon Exclusion

On December 12, 2025, the US State Department convened the inaugural Pax Silica Summit in Washington, D.C. The initiative brought together Japan, South Korea, Singapore, the Netherlands, the UK, Israel, the UAE, and Australia to sign a declaration committing to coordinated supply chains across the full technology stack: critical mineral extraction and processing, semiconductor manufacturing, AI infrastructure, and logistics.

India joined in February 2026, Sweden in March. The Pax Silica Fund launched on March 26, 2026, and is in early deployment.

The Logic of Exclusion

The strategic ambition was explicit and historically framed: if the twentieth century ran on oil and steel, the twenty-first runs on compute and the minerals that feed it. Pax Silica aims to reduce “coercive dependencies” — specifically, the dependence on China’s processing dominance that the 2025 US-China trade war made viscerally clear when Beijing used export controls on gallium and germanium to win tariff concessions from Washington.

Pax Silica coalition members vs African critical mineral producers geopolitics 2026

Africa’s Strategic Response to Pax Silica

What is conspicuously absent from the coalition is any African state. The DRC supplies cobalt. South Africa supplies platinum group metals. Zimbabwe supplies lithium. Guinea supplies bauxite. No African government was invited to help govern the supply chain architecture that depends on their resources.

The logic is structural, not accidental: Pax Silica was built around countries with strong financial ecosystems and advanced manufacturing — Singapore for logistics, Israel for venture capital, the UAE for sovereign wealth liquidity. Selection criteria focus on co-investors in fabrication architecture, not raw material providers.

For African policymakers, the correct response is not to petition for Pax Silica membership — it is to make non-membership expensive for the coalition. Countries that coordinate export restrictions, processing requirements, and beneficiation timelines across the minerals Pax Silica needs create a de facto price for exclusion that Washington must eventually calculate.

The AU Green Minerals Strategy: Continental Framework or Policy Aspiration?

The African Union’s African Green Minerals Strategy (AGMS) is the most significant continental policy response to the global minerals competition — and its success or failure will determine whether Africa’s new mineral assertiveness produces lasting industrial transformation or remains a collection of uncoordinated national policies that external powers navigate around one at a time.

Pillars of the AGMS

The AGMS rests on three substantive pillars. First, local beneficiation: minerals should be processed where they are mined. Second, responsible and ESG-aligned practices that position Africa as a preferred supplier to markets with strict traceability requirements, including the EU’s battery passport framework.

Third, green industrialisation: mineral wealth should anchor domestic manufacturing and employment rather than commodity revenue alone. The strategy is explicitly aligned with the AfCFTA Secretariat‘s Rules of Origin framework, targeting intra-African mineral value chains rather than individual-country supply deals.

Historical Implementation Barriers

The African Mining Vision — the AGMS’s predecessor — was adopted in 2009 and remains “very fragmented” in implementation sixteen years later. The AGMS risks the same trajectory without a binding coordinated negotiating mechanism between member states. Additionally, physical infrastructure remains a binding constraint. Africa’s road density averages 2.76km per 100km²; 15% of rail is non-operational; 13 countries have no rail to sea. Beneficiation requirements without processing infrastructure send investors to better-connected locations.

The Chokepoint War: China’s Processing Moat vs. America’s Security-Driven Diplomacy

China’s position in the African minerals competition is structural and was built over decades of patient, state-directed investment that Western private capital consistently declined to match. State-backed firms control 72 percent of cobalt and copper mines in the DRC alone.

China’s 91 percent share of global rare earth refining and its dominance in cobalt, lithium, and copper processing means that even minerals extracted by non-Chinese companies must often be refined through Chinese facilities before becoming usable.

Weaponization of the Supply Chain

Beijing demonstrated its willingness to weaponize this position in 2025, using export controls on gallium and germanium to win tariff concessions from Washington in the US-China trade war — a live lesson in how mineral supply chain control functions as diplomatic coercion.

This has accelerated Western efforts to decouple, but China’s physical ownership of African mine-to-port logistics makes “derisking” a generational challenge rather than a policy cycle one.

The American Infrastructure Counter-Move

America’s counter-move under the second Trump administration has been aggressive in framing and uneven in delivery. The February 2026 Critical Minerals Ministerial launched FORGE as successor to the Minerals Security Partnership and completed a joint venture securing 100,000 tons of copper for American supply chains from Africa. The US Lobito Corridor — a rail investment linking Zambia and the DRC to Angola’s Atlantic port — is a genuine infrastructure counter to China’s BRI dominance.

Beijing responded immediately by committing to rehabilitate the Zambia-Tanzania railway, demonstrating that US infrastructure moves do shift Chinese behaviour.

Russia’s Minerals Model: Security-for-Ore and Its True Costs

Russia’s approach to African critical minerals is operationally unlike every other actor in this analysis. It does not compete through capital markets or technology transfer. It competes through security provision — deploying state-controlled military advisors to fragile governments in exchange for mining concessions. What began as the Wagner Group’s privatized model has since 2024 been absorbed into Africa Corps, operating under direct Ministry of Defense authority.

Case Study: Central African Republic and Mali

The Central African Republic remains the most developed case study. From 2018, Wagner embedded itself in President Touadéra’s security apparatus, securing gold and diamond concessions in exchange for protecting the government.

In Mali, the model proved harder to replicate. Stricter mineral regulations and northern mines controlled by armed groups hostile to Russian presence limited extraction. Africa Corps seized the Intahaka mine in February 2024, but withdrew within days after realizing the operational costs exceeded the artisanal gold tax revenue.

Gulf Sovereign Capital: The Most Underestimated Player

The entry of Gulf states into African mineral investment may be the most consequential structural shift in critical minerals geopolitics since China’s BRI expansion.

Driven by Vision 2030-style diversification mandates and possessing sovereign wealth funds with the capital and patience to operate where Western private equity will not, the UAE and Saudi Arabia have moved from peripheral to structurally important actors in African mineral supply chains in less than three years.

UAE: Operational Equity and Logistics

UAE’s primary vehicle is International Resources Holding (IRH), chaired by UAE National Security Advisor Tahnoun bin Zayed al-Nahyan. Key operational deals: 51 percent of Zambia’s Mopani Copper Mines ($1.1bn, December 2023); 56 percent of Alphamin Resources’ Bisie tin complex in the DRC ($366m); iron ore joint ventures in Angola. These investments are bundled with port and logistics control via DP World, which manages six African ports.

The EU’s Global Gateway: 300 Billion Euros on Paper, Less on the Ground

The EU’s engagement with African critical minerals is architecturally the most sophisticated of any external actor and operationally the most frustrating to African partners awaiting delivery. The combination of the €300 billion Global Gateway initiative, the Critical Raw Materials Act (CRMA), mandatory ESG and traceability standards, and Strategic Partnership agreements produces the most comprehensive offer on the table. Delivery has been slow.

Recent Progress and CRMA Milestones

Concrete progress did arrive in 2025–2026. The CRMA’s 60 Strategic Projects included four in Africa: Malawi, Madagascar, South Africa, and Zambia.

The EU’s ReSourceEU Action Plan committed €3 billion for 2026. The November 2025 EU–South Africa minerals pact pledged €750 million through Global Gateway, explicitly targeting processing on African soil. These moves are directionally correct toward integrating African projects into the EU battery value chain.

Africa’s Non-Aligned Mineral Policy: A Feasibility Analysis

The most significant intellectual shift in African mineral diplomacy in 2025–2026 is the explicit articulation of multi-alignment as a deliberate strategy. Chatham House’s March 2026 assessment is direct: “Most African countries are now deliberately pursuing multi-alignment — working with China, the Gulf, India, Turkey, and increasingly Russia.”

Strategic Positioning in Kinshasa and Pretoria

In practice: South Africa holds BRICS membership, hosted the G20 presidency, maintains an EU CRMA strategic partnership, and is in active mineral engagement with the US, Gulf, and India simultaneously.

The DRC held the Washington Accords with the US, maintained Chinese mining concessions, engaged UAE sovereign investment, and facilitated Qatari infrastructure diplomacy — all in the same twelve-month period. These are not accidents of foreign policy; they are deliberate positioning.

India’s Positioning: The National Critical Minerals Mission in Africa

India’s engagement with African mineral diplomacy has accelerated sharply since the launch of the National Critical Minerals Mission (NCMM) in January 2025. India is 70 to 80 percent import-dependent on lithium from China, with over ₹34,000 crore spent on critical mineral imports in FY2023–24. Demand is projected to grow fourfold by 2030. Africa is the most accessible large-scale alternative to Chinese supply chains for Indian industry.

A Competitive Pitch to the Global South

India’s pitch is explicitly framed as an alternative to China’s model: technology transfer, workforce training, shared value creation. Indian diplomats emphasize a “partnership of equals,” drawing on long-standing ties to East and Southern Africa. Indian companies are increasingly active in Zambia and Mozambique, focusing on mid-sized assets that are too small for Chinese state giants but perfect for India’s growing manufacturing base.

South-South Cooperation: Building the Infrastructure of Leverage

The strongest evidence against a purely passive framing of Africa’s mineral geopolitics is the growing body of African-initiated industrial strategy that does not wait for external sponsors. South-South mineral cooperation is the most promising structural development of the past three years — and the one most likely to determine whether the new mineral nationalism translates into durable economic transformation.

What Africa Can Extract — and What Policymakers Must Do Before 2030

The critical minerals geopolitics of Africa in 2026 presents the continent with a combination of structural leverage and structural vulnerability it has not encountered in quite this form before. Leverage is real because demand for African minerals is irreversible and viable supply alternatives do not exist at scale. At the same time, vulnerability remains high for individual states negotiating against powers with vast institutional capacity.

The window for converting this leverage into lasting industrial transformation is open — but it is narrow and time-limited. The supply chain architecture being built by Pax Silica, FORGE, the CRMA, and China’s 15th Five-Year Plan will produce a new global mineral order by the early 2030s. Decisions committed now will determine whether Africa is a processing hub in that architecture or a raw materials annex to it.

Policy imperatives

Three policy imperatives stand out from the analysis.

First, the AU Green Minerals Strategy must be operationalized as a concrete coordinated negotiating framework. The Zambia-DRC battery corridor is the model; it produced joint industrial strategy that neither country could have achieved alone.

Second, every infrastructure-bundled investment deal must be evaluated against a single criterion: does it build African processing capacity, or does it build better raw ore export capacity?

Third, and most urgently, African policymakers must act inside the current window of multipolarity before supply chains harden by 2030. This is the most powerful negotiating position Africa has held in a generation.

The strategic imperative: use the multipolarity before it closes

Africa holds 30% of global critical mineral reserves. The world’s AI infrastructure, clean energy transition, and semiconductor supply chains all depend on what African soil contains. The great-power competition for that soil — Pax Silica, FORGE, the CRMA, Gulf sovereign capital, India’s NCMM — gives African states a window of genuine leverage they have not had in a generation.

That window closes as supply chains harden through the late 2020s. The choice is not between China and the West. It is between coordinated agency and fragmented deference. The Zambia-DRC battery corridor shows what the former looks like. The next ten decisions taken in Kinshasa, Lusaka, Harare, Windhoek, and Pretoria will determine which path the continent actually takes.