South Africa controls 70% of Africa’s data center capacity but holds just 1% of global AI compute. That gap isn’t a weakness — it’s the continent’s largest untapped digital frontier. And the money is starting to follow that logic.

Here’s Why That 1% Figure Tells the Whole Story

The Executive Summary

- The Paradox: South Africa holds 70% of Africa’s data center capacity but just 1% of global AI compute — a gap that reframes the story from weakness to the continent’s most compelling infrastructure growth thesis.

- The Shift: Investment has pivoted from cloud storage to sovereign AI compute. Microsoft’s $5.4B commitment and Cassava’s NVIDIA GPU rollout signal that South Africa is transitioning from “server landlord” to Africa’s GPU Clearing House.

- The Cost: Power reliability has stabilised (200+ consecutive days without load shedding by late 2025), but a 14,000km transmission gap, high GPU access costs, and slow enterprise adoption remain the three structural risks that determine whether the anchor holds.

Live Infrastructure Vital Signs — South Africa Compute Hub

| Metric | Current Status | Context & Source |

| Grid Stability | 322+ Days | Consecutive days without load shedding (as of April 2026, Eskom Recovery Plan). |

| AI Readiness | 5 / 56 | Data centers currently equipped with high-density cooling for AI workloads. |

| Critical Power | 228 MW | Total capacity for Teraco (including JB7 campus completion, due late 2026). |

| Compute Power | 3,000+ GPUs | NVIDIA units deployed via Cassava Technologies (Phase 1 rollout, 2025). |

| Market Growth | 43.7% CAGR | Projected annual growth rate for SA’s AI data center market through 2030. |

South Africa didn’t become Africa’s compute capital through a national strategy or a long-term digital masterplan. It became the anchor the same way most infrastructure hubs emerge — through the compounding logic of geography, finance, and being the first place that worked well enough to justify the next investment.

Johannesburg sits at the continental convergence of subsea cable systems, hosts the most sophisticated financial sector in sub-Saharan Africa, and built its first major data centers years before any serious competitor moved. Those advantages still hold. The question now is whether they hold long enough — and at sufficient scale — to absorb what’s coming.

AI infrastructure race

Because what’s coming is significant. The global AI infrastructure race is, for the first time, looking at Africa as a serious participant rather than a future market. That attention lands first in South Africa. But the investment wave brings its own pressure: it demands power density the grid wasn’t designed for, GPU access the supply chain hasn’t prioritized, and enterprise adoption at a pace South African businesses aren’t yet moving at. The headline figures are genuinely impressive. The structural gaps are genuinely real.

This piece navigates both.

South Africa’s share of Africa’s total data center capacity is 70%— across 56 facilities hosting AWS, Microsoft Azure, and Google Cloud regions. The continent’s next-largest market doesn’t come close.

Map of the African continent showing the routes of the Equiano and 2Africa submarine cables, highlighting Johannesburg, South Africa as the primary high-capacity landing and exchange hub.

How Johannesburg Became the Continent’s Default Compute Hub

The Cable Advantage

The most literal explanation for South Africa’s dominance is physical: submarine cables. Johannesburg is the primary landing point for the cable systems connecting sub-Saharan Africa to Europe, Asia, and the Americas. The Equiano cable (Google) and the 2Africa cable (Meta-led consortium) are the two most recent additions to that infrastructure — and both terminate with South Africa as a primary anchor node.

The strategic significance of the 2Africa system in particular shouldn’t be underestimated. The 2Africa West Subsea Route activated in Q4 2025, delivering high-speed, low-latency capacity along the full West African coastline — not as a separate system, but as an extension of infrastructure that still routes through Johannesburg’s exchange points.

Every time a packet of data from Lagos or Accra touches the global internet, it’s often transiting South African infrastructure first. That’s the foundation of anchor status: you’re not just a destination, you’re a transit point.

Financial and Regulatory Maturity

Infrastructure follows money, and South Africa has the most sophisticated banking and financial services sector on the continent. That matters for data center investment for a specific reason: banks are the primary high-value AI workload drivers.

Fraud detection, real-time credit scoring, algorithmic risk assessment, customer identity validation — these are the workloads that justify hyperscale GPU infrastructure because they run continuously, at low latency, and with zero tolerance for downtime.

South African financial institutions have been early and aggressive AI adopters, not because of enthusiasm for the technology but because the commercial case — particularly for fraud detection — is immediately measurable. The result is that South Africa has a domestic demand base that other African markets can’t yet match at scale, which in turn justifies the infrastructure investment that attracts international players.

Regulatory clarity amplifies this. The Protection of Personal Information Act (POPIA), South Africa’s data protection framework, gives the country the most established data sovereignty environment in sub-Saharan Africa. Hyperscalers — particularly those serving enterprise clients with strict data residency requirements — choose South Africa because they understand the legal terrain. That predictability has monetary value, and it shows in the investment decisions.

First-Mover Lock-In

Teraco (now a Digital Realty subsidiary), Africa Data Centres (Cassava Technologies), and NTT Data established large colocation campuses in Johannesburg before any serious regional competitor had the scale to attract global hyperscalers. That head start created a self-reinforcing dynamic. Once AWS, Azure, and Google Cloud commit a local region to a facility, the facility becomes essential to every enterprise in the country that uses those cloud platforms.

And once it’s essential, competitors can’t displace it by simply building something newer nearby — they have to offer lower latency, better interconnection, or meaningfully lower cost. None of South Africa’s regional rivals can currently offer all three.

“South Africa is a springboard for cloud provision into Africa and, as a result, has become the technology and data centre hub for sub-Saharan Africa. Massive global investments into undersea cables, like Equiano and 2Africa, further strengthen this position.”— Jan Hnizdo, CEO, Teraco

The Investment Wave — Who Is Betting on South Africa?

The investment signals from 2024 through early 2026 have been unusually clear in direction. The money is moving fast, it’s denominated in billions, and it’s targeting AI compute specifically — not general cloud capacity.

Active Capital Commitments — South Africa AI Infrastructure (2024–2026)

| Investor / Player | Commitment | Focus Area | Status |

|---|---|---|---|

| Microsoft | $5.4 Billion (USD) / ZAR 5.4B | Cloud & AI infrastructure; NVIDIA GPU access via AI Diffusion Framework preferred status | Announced March 2025; active |

| Cassava Technologies | ~$700M programme; 3,000 NVIDIA GPUs (Phase 1) | Regional AI Mesh — SA anchor, expanding to Kenya, Nigeria, Egypt, Morocco | Phase 1 deployed June 2025 |

| Teraco / Digital Realty (JB7) | R8 Billion syndicated loan; 40 MW critical power load | High-density liquid-to-air & liquid-to-liquid cooling for AI workloads; 120 MW solar PV plant | Construction started Nov 2024; completion 2026 |

| MTN Group | Ambition 2030 (undisclosed capital) | Greenfield AI-enabled data centers; SA confirmed as Priority Market 1 | Market assessment complete Q1 2025; co-investment partners shortlisted |

| Africa Data Centres (Cassava) | R2 Billion (Cape Town capacity doubling) | Western Cape expansion; NVIDIA DGX SuperPOD — branded Africa’s first “AI Factory” | Financing secured; June 2025 deployment confirmed |

The trajectory of the market supports these commitments. The AI data center market in South Africa is projected to grow from $78.85 million in 2025 to $483.5 million by 2030 — a 43.7% compound annual growth rate that, if sustained, would represent one of the fastest infrastructure scaling stories in the emerging world.

The broader African data center construction market, valued at $1.26 billion in 2024, is projected to nearly triple to $3.06 billion by 2030.

What’s striking about the capital table above isn’t just its size — it’s its composition. Microsoft’s investment isn’t a general infrastructure play; it’s a deliberate positioning move anchored to GPU chip allocation rights under US export controls. Cassava’s commitment isn’t a colocation expansion; it’s an attempt to build a distributed continental AI mesh.

These are sovereign compute investments, not capacity investments. That’s a categorical difference, and it’s the shift that defines South Africa’s current infrastructure moment.

From Server Landlord to GPU Clearing House — The Sovereign AI Pivot

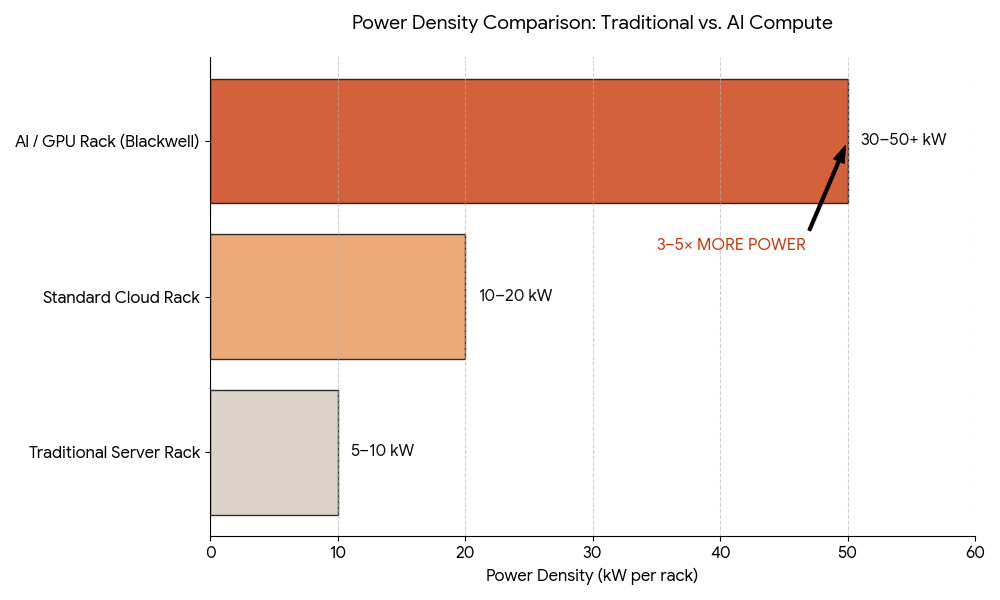

The distinction between cloud infrastructure and AI compute infrastructure is not semantic — it’s architectural, economic, and increasingly geopolitical. Cloud infrastructure stores data and serves applications. AI compute infrastructure processes intelligence: training large models, running inference at scale, fine-tuning foundation models for local datasets and languages.

The two require fundamentally different hardware, different cooling systems, and orders of magnitude different power inputs.

Power Density: Traditional Cloud vs. AI Compute — Why South Africa’s Cooling Infrastructure Had to Change

Teraco JB7 benchmarks: 1.47 PUE (Power Usage Effectiveness) | 0.05 L/kWh water intensity — both world-class metrics for an African facility operating in a water-stressed environment. Sources: Teraco JB7 specs; Mordor Intelligence SA AI Data Center Report 2026.

The GPU Clearing House Role

Microsoft’s preferred distributor status under the US AI Diffusion Framework is the most consequential geopolitical detail in South Africa’s infrastructure story right now. The AI Diffusion Framework controls which entities can purchase and distribute high-end NVIDIA chips — the H100s and B200s that power large-scale AI training and inference.

Microsoft holds preferred status. South Africa is Microsoft’s primary African infrastructure anchor. The logic connecting these two facts creates a specific structural position: when a startup in Lagos, a government ministry in Accra, or a bank in Nairobi needs access to high-end GPU compute, the most viable legal and logistical path currently routes through Johannesburg.

That is the definition of a clearing house — not a destination you choose because it’s the best option, but a transit point you pass through because the architecture makes it necessary. South Africa isn’t holding that position passively. Cassava’s June 2025 deployment of over 3,000 NVIDIA GPUs at its South Africa facility — the first phase of a broader continental mesh — is a deliberate attempt to institutionalize that clearing house role before a competitor can claim it.

The Access Gap — Who Benefits, Who Doesn’t

Infrastructure dominance does not automatically translate to equitable access. This is the friction point that separates the investment narrative from the development reality. Across the continent, only 5% of AI innovators have reliable access to advanced compute — a figure that reflects latent demand suppressed by cost and infrastructure absence, not a lack of ambition.

GPU access globally continues to favour hyperscalers. Smaller African buyers still face steep prices and long delivery windows, and South Africa’s anchor status doesn’t change that structural inequality on its own.

The shift from cloud (affordable, commoditized) to AI compute (scarce, expensive) actually risks widening this gap if the investment wave primarily serves large enterprise and government clients while leaving startups and smaller businesses priced out.

This is the policy gap that Microsoft’s pledge to train 1 million South Africans in AI skills by 2026 only partially addresses — training users to work with AI tools is not the same as providing the compute infrastructure for them to build and deploy AI models.

The Power Question — Eskom, Stability, and the Green Compute Pivot

The Load Shedding Legacy

Any credible account of South Africa’s data center infrastructure has to start with Eskom’s failures, because those failures shaped every investment decision, every cost structure, and every risk assessment made in this market for the past decade. Load shedding isn’t a background nuance — it is the central variable around which South African data center operations were engineered.

The costs were not abstract. Load shedding costs to the South African economy surged fivefold between 2020 and Q1 2023, reaching ZAR 224 billion. Every data center operator in the country was forced to build diesel generator redundancy at a scale that peers in Europe and North America don’t carry — adding capital expenditure and ongoing operational costs that are invisible in the headline infrastructure statistics but very visible on the balance sheet.

The 2025 Stability Milestone

Stability Milestone — Eskom Grid Performance 2025

“South Africa has now experienced over 199 consecutive days without an interrupted supply, with only 26 hours of load shedding recorded in April and May during the financial year. The Energy Availability Factor stands at 67.55% month-to-date in December 2025 — a year-on-year improvement of 10.5%.”— Eskom Data Portal ·

This is genuinely significant. The Generation Recovery Plan is delivering measurable results. Unplanned outages dropped by over 1,800 MW year-on-year. Diesel expenditure fell sharply. For data center operators who spent years engineering around 6–8 hour daily outages, 200 consecutive stable days represents a structural improvement in the investment case, not just a temporary reprieve.

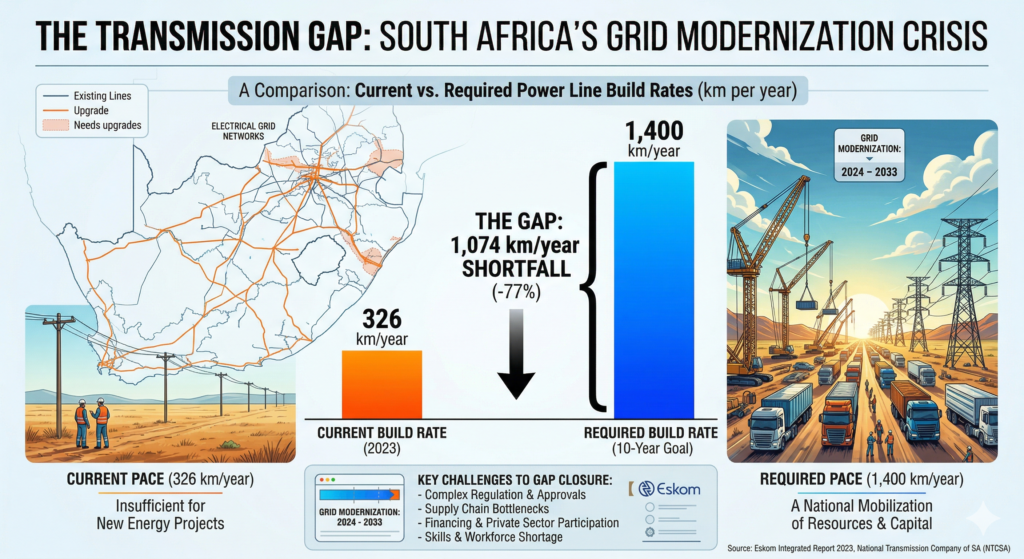

The Transmission Gap — The Hidden Bottleneck

Eskom estimates that 14,000km of new transmission lines are needed over the next decade to connect new power generation to demand centres. In 2023, South Africa built just 326km. The generation crisis is easing. The grid infrastructure crisis is not. For hyperscale data center operators planning 10-year investment horizons, this transmission gap is the more consequential risk.

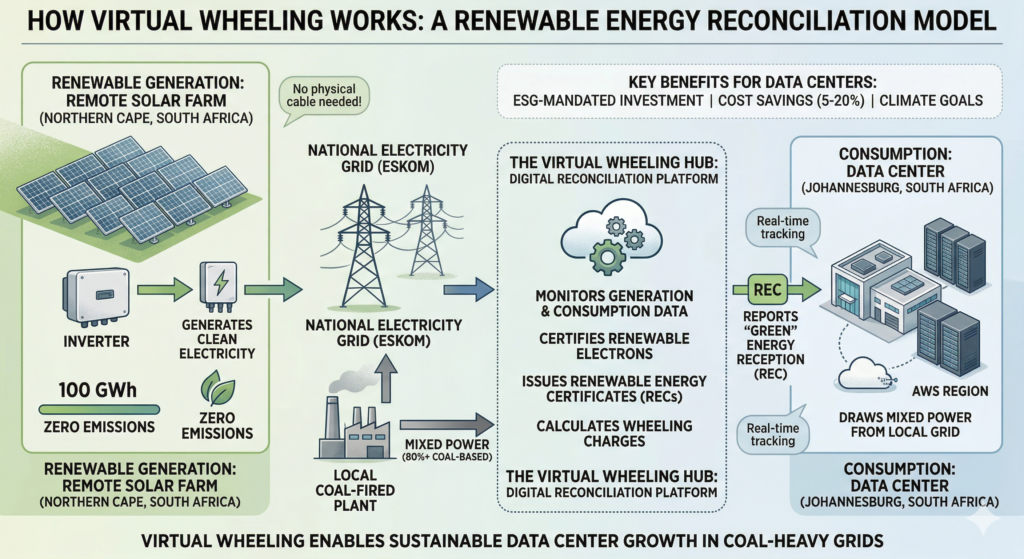

A remote solar farm generates power into the national grid while a data center in a different city receives renewable energy credits through a digital reconciliation platform.

Virtual Wheeling — The Real Story for 2026 and Beyond

While load shedding has dominated the South Africa energy narrative for over a decade, the more strategically important development for data center investment is what’s happening at the policy and procurement layer: virtual wheeling.

Virtual wheeling is, in essence, a sophisticated energy accounting system. A data center in Johannesburg signs a Power Purchase Agreement with a solar farm in the Northern Cape. That farm injects renewable electricity into the national grid. The data center draws an equivalent volume of electricity from its local grid connection — and the virtual wheeling platform, now operated at scale, reconciles the generation and consumption data to certify the transaction as renewable.

No dedicated cable is required. No geographic adjacency is needed. The renewable energy doesn’t physically flow to the data center — what flows is the accounting credit that allows the operator to legitimately claim renewable sourcing.

This matters for three reasons that compound on each other

First, European and American hyperscalers operating under net-zero mandates cannot locate infrastructure in markets where they cannot credibly claim renewable power sourcing. Before virtual wheeling, South Africa’s coal-heavy grid (still over 80% coal-fired) was a hard barrier to ESG-conscious investment. Virtual wheeling removes that barrier.

Second, renewable energy sourced through virtual wheeling is delivering cost savings of 5–20% compared to traditional grid electricity — making it commercially attractive independent of the ESG argument.

Third, the combination of virtual wheeling and rapidly declining battery energy storage costs is beginning to turn intermittent renewable generation into a credible 24/7 supply chain for data center operations.

The live deployment data reinforces the momentum. Vodacom’s Power Purchase Agreement with SOLA Group went live in September 2025 — the first virtual wheeling arrangement operationalised at scale on the African continent, drawing from SOLA’s 195 MW Springbok Solar Power Project in the Free State.

Teraco has committed R3.5 billion to building 200 MW of utility-scale solar by 2035, with 100 MW already registered with NERSA and wheeling agreements secured with the City of Ekurhuleni and the City of Cape Town. Vantage Data Centers has concluded similar wheeling agreements with solar farms in the remote Northern Cape.

Teraco’s 120 MW solar PV plant, currently under construction in the Free State province, is expected to supply power to its data centers across the country by 2026 — covering a meaningful portion of its 228 MW total critical power load from renewable sources via the national grid as a transmission medium.

“Virtual wheeling creates a triple win: for the planet, for grid stability, and for business. Renewable energy through virtual wheeling can deliver cost savings of 5–20% compared to traditional grid electricity.”— Vodacom Virtual Wheeling Report, November 2025

The Investment Timeline

| Date | Milestone | Strategic Impact |

| November 2024 | Teraco JB7 Groundbreaking | Construction begins on the 40 MW JB7 facility (funded by a R8B loan) and a 120 MW solar PV plant in the Free State. |

| Q1 2025 | MTN Group Market Confirmation | South Africa and Nigeria are officially confirmed as Priority 1 markets for greenfield data center development. |

| March 2025 | Microsoft Capital Commitment | Microsoft commits ZAR 5.4 billion to SA infrastructure and pledges to train 1 million citizens in AI skills by 2026. |

| June 2025 | Cassava’s “AI Factory” Launch | Phase 1 deployment of 3,000+ NVIDIA GPUs is completed, marking the launch of Africa’s first branded AI Factory. |

| September 2025 | Virtual Wheeling Activation | The Vodacom/SOLA Group PPA goes live, fueled by the 195 MW Springbok Solar Project—Africa’s first large-scale operational wheeling event. |

| 2026 (Target) | Full Operational Integration | Teraco JB7 and the 120 MW solar plant reach completion; Microsoft’s sovereign AI infrastructure becomes fully operational. |

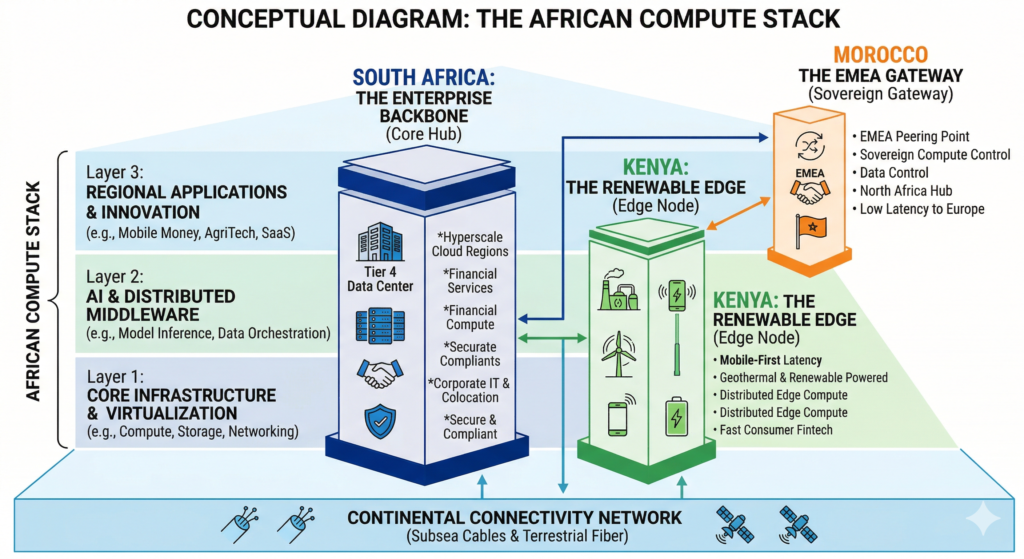

The Competitive Map — “Fort Knox” vs. The Edge

South Africa’s dominance is real and durable in the near term. But framing it as unchallenged misreads the emerging continental architecture. The more accurate picture is that sub-Saharan Africa is developing a tiered compute stack — and the different tiers serve fundamentally different workloads.

South Africa is not competing with Kenya for the same compute business. Understanding this distinction matters for anyone assessing where to deploy AI workloads, where to invest, and what the competitive dynamics actually look like over the next five years.

South Africa: “The Fort Knox”

Secure, enterprise-grade, regulated. Banking, insurance, telco B2B, government sovereign AI. High compliance overhead. Latency-tolerant for heavy workloads. GPU clearing house for the continent.

Kenya: “The Edge”

Mobile-first, consumer-facing AI. Fintech micro-decisions, health diagnostics, agri-data services. IXAfrica/Safaricom NBO1 targets 22.5 MW. 90% renewable grid is a structural ESG advantage.

Morocco: “The EMEA Gateway”

Sovereign compute positioning for Europe, Gulf, and North Africa. Naver/NVIDIA 500 MW campus (announced June 2025) targets EMEA AI infrastructure — not African-market workloads.

Nigeria: “The Deferred Giant”

Population scale South Africa cannot match. Grid constraint is the binding limit — never exceeded 6 GW for 230M people vs. SA’s 48 GW for 63M. MTN’s greenfield bet is a long-horizon play.

The Kenya contrast is particularly instructive, and worth engaging with honestly rather than dismissing as a lesser competitor. Kenya’s grid is approximately 90% renewable — predominantly geothermal and hydro. For AI workloads that require clean-energy certification, Kenya offers a structural advantage that South Africa’s virtual wheeling progress is only beginning to approximate.

Microsoft and G42’s 100 MW data center commitment in Kenya — expandable to 1 GW, powered entirely by geothermal — is a direct play on that advantage, not a consolation investment after missing out on South Africa.

A conceptual diagram of the African ‘Compute Stack,’ categorizing South Africa as the core enterprise hub, Kenya as the renewable edge node, and Morocco as the sovereign compute gateway for EMEA.

The market is best understood not as a competition between African countries but as a continental stack being built layer by layer. South Africa is the backbone. Kenya is the East African edge node. Morocco is the North African and EMEA gateway.

Nigeria is the eventual West African anchor, waiting on grid infrastructure that isn’t there yet. These layers are complementary. A startup in Nairobi building a consumer health AI application probably doesn’t need South African data center infrastructure — but the bank providing their healthcare financing almost certainly does.

Data visualization showing the ‘Transmission Gap’ in South Africa: A comparison between the current annual build rate of 326km of power lines and the 1,400km per year required to meet the 10-year grid modernization goal.

What Needs to Happen to Lock In the Anchor Role

South Africa earned its position through geography, early infrastructure build-out, and regulatory predictability. But anchor status in digital infrastructure isn’t a permanent designation — it’s a market position that must be actively maintained.

The following five requirements aren’t aspirational wish-list items; they are the specific structural gaps whose resolution will determine whether South Africa deepens its lead or watches it erode over the next decade.

1. Transmission Grid Acceleration

The single most urgent infrastructure requirement is not new data center capacity — it’s the transmission lines to power what’s already planned. Eskom’s own estimates call for 14,000 km of new transmission lines over the next decade. At the 2023 pace of 326 km per year, that target would take 43 years to reach.

The government’s separation of Eskom’s generation, transmission, and distribution functions creates the structural conditions for private sector participation in transmission build-out. But structural conditions alone don’t string cable. The National Transmission Company of South Africa (NTCSA) needs capital, independent borrowing authority, and an accelerated construction mandate — and it needs them before 2028, not after.

2. Virtual Wheeling at Data Center Scale

The Vodacom and Teraco wheeling models need to become industry standard, not exceptional. Specifically, the South African Wholesale Electricity Market (SAWEM), expected to go live in 2026, should create the liquidity mechanisms that allow data center operators to source renewable PPAs through competitive market processes rather than bilateral negotiations.

ESG-driven hyperscale capital from European operators will not flow to a coal-backed compute stack, regardless of the infrastructure quality. Virtual wheeling, at sufficient scale, removes that objection permanently.

3. GPU Access Below Enterprise Pricing

Microsoft’s preferred distributor status under the AI Diffusion Framework is a geopolitical win for South Africa. It means nothing for African AI innovation if the pricing structure serves only enterprise and government clients.

A meaningful GPU access programme — whether structured as subsidised access for registered startups, compute credits through a national AI innovation fund, or shared-infrastructure models at university research centres — is the policy gap that most directly connects infrastructure investment to the talent and innovation ecosystem it’s supposedly enabling.

4. Skills Pipeline Depth

The distinction between training AI users and training AI builders is not a pedantic one. South Africa needs machine learning engineers, data infrastructure architects, and AI safety researchers — not primarily more prompt engineers.

Microsoft’s commitment to train 1 million South Africans is directionally correct and genuinely valuable. But the country’s universities, technical colleges, and private training providers need to be building curriculum depth in model development, not just application use, if the skills base is to match the infrastructure ambition.

5. Johannesburg as a Continental Peering Hub

NAPAfrica, based at Teraco’s Isando campus, is already Africa’s largest internet exchange point — a facility where African ISPs and content providers directly peer with each other, reducing latency and transit costs for African internet traffic. With over 16,500 interconnects at the Isando campus, Johannesburg is already performing this function to a degree.

The next step is actively extending that peering architecture to serve East, West, and Central African traffic — not just as a destination, but as an exchange. The difference matters: a destination requires traffic to route to you; an exchange allows traffic to transit through you. The latter creates stickier infrastructure lock-in and generates value across the continent, not just within South Africa’s borders.

Frequently Asked Questions

Why does South Africa dominate African data center capacity?

South Africa’s dominance is the result of a “compounding advantage” across three pillars: connectivity, capital, and compliance.

- Connectivity: Johannesburg serves as the primary landing hub for the continent’s most powerful subsea cables, including Google’s Equiano and Meta’s 2Africa.

- Capital: A sophisticated financial sector provides the high-value AI workloads (fraud detection and credit scoring) that justify hyperscale investment.

- Compliance: The POPIA framework offers a level of data sovereignty and legal predictability that reduces the “risk premium” for global hyperscalers like AWS, Azure, and Google Cloud.

What is virtual wheeling and why does it matter for South African data centers?

Virtual wheeling is a digital energy-accounting system that allows data centers to purchase renewable energy from remote solar or wind farms (often in the Northern Cape or Free State) and receive certified green-energy credits via the national grid.

It is the “unlock” for ESG-conscious investment. Because the Eskom grid remains 80% coal-heavy, virtual wheeling allows hyperscalers to bypass the “dirty” carbon profile of the grid, achieving clean-energy certification and cost savings of 5–20% compared to standard municipal tariffs.

Is load shedding still a problem for South African data centers in 2026?

The situation has fundamentally shifted. As of April 2026, South Africa has surpassed 322 consecutive days without load shedding, marking the most stable period for the national grid in over a decade. While diesel backup systems remain a standard “insurance policy” for Tier III and IV facilities, the operational burden of running generators has plummeted by over 60% year-on-year. The primary concern has now shifted from generation (having enough power) to transmission (having the lines to move it), where a 14,000km infrastructure gap remains.

How does South Africa’s AI data center capacity compare globally?

South Africa hosts roughly 70% of Africa’s total capacity, yet this represents only about 1% of global AI compute. This “1% Paradox” defines the current market: South Africa is a regional giant but a global startup. To close this gap, the market is projected to grow at a 43.7% CAGR through 2030, driven by the deployment of AI-ready facilities like Teraco’s JB7, which utilizes liquid-to-liquid cooling to handle the extreme power density (up to $50\text{kW}$ per rack) required by NVIDIA Blackwell chips.

Will South Africa lose its infrastructure lead to Kenya or Morocco?

Unlikely, because they are serving different layers of the “Continental Stack.”

- South Africa is the “Fort Knox”: heavy enterprise workloads, banking, and sovereign government compute.

- Kenya is the “Renewable Edge”: consumer-facing fintech and mobile-first AI running on a 90% green grid.

- Morocco is the “EMEA Gateway”: a strategic bridge for workloads serving Europe and the Middle East.These markets are complementary; a regional mesh makes the entire continent’s digital economy more resilient rather than creating a winner-take-all scenario.

What is the AI Diffusion Framework and why does it affect South Africa?

Administered by the US Bureau of Industry and Security (BIS), this framework governs the export of high-end AI chips. Microsoft holds “Preferred Distributor” status, and because they have anchored their African AI infrastructure in Johannesburg, South Africa has become the de facto GPU Clearing House for the continent. If you are an African developer training a foundation model on H100s or B200s, your data is likely transiting South African geography to access that silicon.

Is the AI skills gap being closed?

There is a vital distinction between AI Literacy and AI Engineering. While initiatives like Microsoft’s 1-million-person training pledge are excellent for creating AI users, South Africa still faces a critical shortage of AI builders—specifically data architects and machine learning engineers capable of maintaining hyperscale infrastructure. Closing the “1% Paradox” requires moving beyond prompt engineering to deep-tech infrastructure expertise.