China has not built a weapon pointed at Silicon Valley. It has built a supply chain so deeply embedded in the precursor materials of AI hardware that the distinction barely matters. This is an investigation into upstream asymmetry — and what it costs Nvidia every time a mine changes hands in Kazakhstan.

There is a mine in Kazakhstan you have almost certainly never heard of. In 2025, China injected $12 billion into Kazakhstani aluminum and another $7.5 billion into copper extraction under the Belt and Road Initiative — more than the full BRI metals and mining spend of any single prior year.

On a balance sheet, this looks like industrial investment. In the context of AI hardware, it looks like something else entirely: the quiet, systematic annexation of the physical inputs required to run a Nvidia H200 cluster. The copper busbars that distribute power.

The aluminum heatsinks that keep Blackwell GPUs from melting. The precursor materials that feed the foundries that feed the chips. China is not trying to build a better GPU. It is building control over everything a GPU requires to exist.

Aerial view of a BRI-financed open-pit copper mine in Kazakhstan, a key source of critical minerals for AI semiconductor supply chains

Mineral sovereignty in AI

This is the architecture of mineral sovereignty in AI — and understanding it requires abandoning the comfortable fiction that semiconductor competition is primarily a software or even a fab story. The real contest is upstream, in the dirt, at the point where geology meets geopolitics.

The Belt and Road Initiative is, at its most strategically legible, a decade-long program of vertical integration over the global mineral commons. And Nvidia, as the world’s most consequential fabless chipmaker, sits at the far end of a supply chain it has almost no direct visibility into.

“China has achieved a near-monopsony position over the precursor materials required for high-frequency AI logic — effectively placing a structural geopolitical tax on the Blackwell supply chain.”— Supply Chain Strategy Analysis, 2026

What a GPU Actually Requires

The public narrative around semiconductor supply chains focuses on fabrication nodes — the angstrom-level engineering at TSMC’s fabs in Hsinchu and Arizona. This is understandable. It is also incomplete. Before a transistor can be etched at 3nm, a chain of chemical and geological precursors must be assembled, purified, and delivered to exacting specifications.

These are the precursor materials — the raw chemicals and refined inputs that exist before they become a chip.

The Blackwell Material Stack

For a Blackwell-generation GPU, the material dependencies are specific and largely non-substitutable. Gallium, processed into gallium nitride (GaN) and gallium arsenide (GaAs), is essential for the high-frequency, high-power switching that makes AI inference viable at scale.

Germanium underpins high-speed integrated circuits and the fiber-optic infrastructure that connects GPU clusters.

Tungsten — valued for its exceptional resistance to heat — serves as the contact metal in transistor interconnects inside the chip itself.

Cobalt provides electromigration resistance in advanced semiconductor nodes, extending chip lifetime under heavy compute loads.

Rare earth elements, though not embedded in the GPU die itself, are critical inputs to the chip manufacturing equipment: the magnets in lithography systems, the slurries used in chemical-mechanical planarization (CMP), the optical coatings on lens systems inside ASML machines.

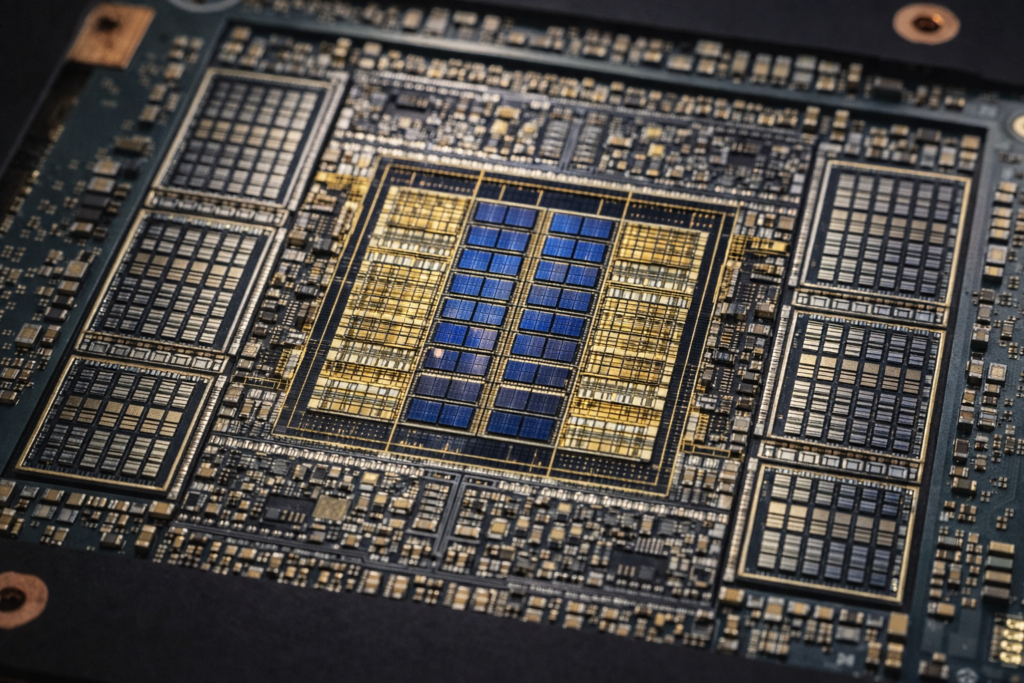

Nvidia Blackwell GPU die showing transistor interconnects made from tungsten, cobalt, and rare earth precursor materials

Fabless by Design, Blind by Default

Nvidia’s own conflict minerals filings acknowledge the structural opacity here. As a fabless company — one that designs chips but contracts all manufacturing to partners like TSMC and Samsung — Nvidia has no direct relationships with smelters or refiners. It cannot independently verify the origin of the materials embedded in its products. The fabless vulnerability is not a compliance failure. It is structural: Nvidia’s business model optimizes for design excellence at the cost of supply chain traceability.

The BRI as a Vertical Integration Strategy

When the Belt and Road Initiative launched in 2013, Western analysts focused primarily on the infrastructure layer: ports, railways, bridges, debt dynamics. This was a category error. The infrastructure was never the product. It was the logistics network that made the real product — patient capital-backed mineral extraction — operationally coherent.

Why Patient Capital Changes Everything

The concept of patient capital is central here. Chinese policy banks — the China Development Bank and China Exim Bank — operate with a tolerance for long-horizon, below-commercial-return investments that no Western public company can replicate.

A copper mine in the DRC or a rare earth project in Kazakhstan may take fifteen years to reach payback. Western mining majors, answerable to quarterly earnings, cannot sustain that exposure. Chinese state-backed entities, explicitly mandated to treat mineral security as a national interest, can and do. This asymmetry in investment horizon is as strategically significant as any export control.

The Kazakhstan Pivot: Securing AI’s Physical Plant

The scale of this patient capital deployment has accelerated sharply. In 2025 alone, BRI investment in the metals and mining sector reached $32.6 billion — including $15 billion in direct mining operations. In the first half of 2025, Kazakhstan alone absorbed $19.5 billion in Chinese engagement across aluminum and copper. These are not coincidental figures.

Copper is required for every busbar, every power distribution rail, every interconnect in an AI data center. Aluminum is the primary material for the thermal management systems that prevent GPU clusters from becoming incandescent. China is not securing battery metals for electric vehicles. It is securing the physical infrastructure of AI compute.

Dependency Matrix — BRI Minerals to Nvidia GPU Architecture

| Stage | Resource | Chinese Control | Nvidia Exposure | Risk Level |

|---|---|---|---|---|

| Upstream | Gallium / GaN | ~98.8% of global supply | AI-grade power logic in Blackwell / Rubin | CRITICAL |

| Upstream | Germanium | ~59% of global supply | High-speed logic; fiber data center links | CRITICAL |

| Midstream | Rare Earth Refining | ~85–90% of processing | Fab equipment magnets; CMP polishing slurries | HIGH |

| Midstream | Cobalt | >50% processing capacity | Advanced node electromigration resistance | HIGH |

| Downstream | Packaging Chemicals | ~30% of TSMC 7nm inputs | Sputtering targets; chemical consumables | MODERATE |

| Infrastructure | Copper / Aluminum | Rising via BRI equity | Data center busbars; GPU cooling systems | HIGH & GROWING |

The Smelter Bottleneck and The 0.1% Rule

There is a common misreading of China’s mineral position: that it can be circumvented by simply mining more ore outside of China. This misreads where the real chokehold sits. Even ore extracted in Australia, Chile, or the DRC must be processed — smelted, chemically separated, refined to semiconductor grade — before it can become a transistor input. This is the refining parity gap, and it is where China’s structural advantage is deepest and most durable.

The Processing Numbers That Define Upstream Asymmetry

Across lithium, cobalt, nickel, and graphite, China controls more than 50 percent of global processing capacity. For gallium, the figure approaches 99 percent. For heavy rare earths — the elements used in the precision magnets inside ASML lithography machines and in the cooling fans attached to every Nvidia GPU — China’s share of refined output is over 85 percent.

The implication is stark: upstream asymmetry does not merely describe who owns the mines. It describes who owns the transformation process that turns geology into technology.

The 0.1% Rule: A Veto Over Every GPU on Earth

The sharpest expression of this leverage is a proposed regulatory mechanism that has not yet been activated but remains live: the 0.1 percent threshold rule. Under regulations drafted in 2025 — currently in abeyance but architecturally intact — any finished product containing even trace quantities of Chinese-processed rare earths would require an individual export license from Beijing’s Ministry of Commerce.

Given that virtually every advanced semiconductor produced anywhere in the world passes through Chinese-processed consumables at some point in the supply chain, this rule would give Beijing effective veto power over the export of any Nvidia GPU on earth. The rule has not been enforced. But it exists.

TSMC, Samsung, and the Point-of-Origin Transparency Problem

TSMC, which manufactures virtually all of Nvidia’s advanced GPUs, reportedly relies on Chinese chemical consumables for approximately 30 percent of its production capacity at 7nm and below. Samsung, which produces high-bandwidth memory stacked on Nvidia’s AI accelerators, placed orders for Chinese sputtering target materials for its 300-layer V-NAND. These are not obscure suppliers.

They are foundational process inputs. The point-of-origin transparency problem — the practical inability of Nvidia or TSMC to fully trace the mineral provenance of their products — is not merely a compliance headache. In a world of escalating export controls, it is an existential supply chain risk.

Value Chain: From BRI Mine to Blackwell GPU

01: BRI Mine — DRC (cobalt), Kazakhstan (copper/aluminum), Indonesia (nickel), Bolivia (lithium). Majority Chinese ownership. Patient capital financing. No Western competitor operates at this risk tolerance.

↓ 02: Chinese Smelter / Refinery — The true chokepoint. Even non-Chinese ore routes through Chinese processing. Refining parity gap means alternatives require 5–10 years to build.

↓ 03: Semiconductor-Grade Precursor Materials — Gallium, germanium, REE compounds, cobalt, tungsten. Subject to export licensing. The 0.1% rule looms.

↓ 04: Fab Equipment & Chemical Consumables — Used by TSMC (7nm / 3nm nodes), Samsung (HBM3e). ASML lithography relies on REE magnets. Point-of-origin transparency collapses here.

↓ 05: Nvidia GPU Fabrication — H100 / H200 / Blackwell / Rubin. Fabless vulnerability: Nvidia has no direct smelter relationships, no independent mineral traceability.

↓ 06: AI Data Center Infrastructure — BRI copper busbars, BRI aluminum cooling. The physical plant of AI compute is also mineral-dependent — and that mineral supply is also being quietly secured.

The Damocles’ Sword: Export Controls as Calibrated Leverage

In December 2024, China’s Ministry of Commerce formally prohibited the export of gallium, germanium, antimony, and super-hard materials to the United States. The impact was immediate: U.S. users reported shortages, and some importers resorted to routing shipments through third countries to access materials that had previously flowed freely.

China had demonstrated, in operational terms, that it could close the tap. Weaponized interdependence — the theoretical framework describing how deeply integrated supply chains can be turned into coercive instruments — had moved from academic concept to industrial reality.

November 2025: The Tap Re-Opens — Conditionally

Then, in November 2025, China suspended the ban. The suspension runs until November 27, 2026, as part of a broader trade truce negotiated following the Xi-Trump meeting in Busan. This has been widely interpreted as a de-escalation. It is more precisely a demonstration.

The ban proved the mechanism worked. The suspension demonstrates that Beijing retains the ability to calibrate the pressure — to tighten or release the valve according to the state of diplomatic negotiations. The materials remain on China’s dual-use export control list. Every shipment still requires a license from Beijing. The military end-use ban remains fully in force. The sword is sheathed, not discarded.

November 2026: The Next Inflection Point

This is the Damocles’ Sword strategy: maximum leverage derives not from using the weapon, but from ensuring that every counterparty knows the weapon exists and is functional. The November 2026 expiry of the current truce is the next inflection point.

If negotiations have not produced sufficient concessions by that date, China possesses a fully tested, legally documented, operationally proven mechanism to constrain the material inputs of the global AI buildout. The Gallium Gap — the absence of any non-Chinese gallium supply at commercial scale — ensures that this leverage has no short-term Western answer.

Separately, China has deployed a more precisely targeted control: export restrictions on rare earth materials specifically required for advanced semiconductor production, with case-by-case approval required for logic chips at 14nm and below and memory chips with 256 or more layers. The H100 and its successors fall directly within that specification range.

The Western Counter-Offensive: FORGE, Price Floors, and Project Vault

FORGE: A Plurilateral Trade Zone with Teeth

The Western response to this structural dependency is real, recent, and significantly underpowered relative to the scale of the problem — though 2026 has brought the most operationally serious effort yet.

On February 4, 2026, Secretary of State Rubio convened the inaugural Critical Minerals Ministerial in Washington, attended by 54 countries and 43 foreign ministers. The headline announcement was the launch of FORGE — the Forum on Resource Geostrategic Engagement — as the successor to the Biden-era Minerals Security Partnership. Chaired by South Korea through June 2026, FORGE is designed as a plurilateral preferential trade zone for critical minerals. Its specific mechanism is to counter one of China’s most effective competitive tactics: market flooding.

Secretary of State Rubio at the 2026 Critical Minerals Ministerial announcing the launch of FORGE

Price Floors: Countering the Dumping Playbook

The price floor architecture addresses a specific vulnerability. When Western mining companies invest in gallium or rare earth extraction — as several are now attempting in the U.S., Australia, and Canada — they face a structural threat: China can flood the market with below-cost material, driving prices below the break-even point for any non-BRI-financed operation.

This is precisely what occurred in the 2024 lithium crash, which bankrupted or suspended dozens of Western lithium projects. FORGE’s proposed reference prices, enforced through adjustable tariffs, are designed to guarantee a floor below which Chinese dumping cannot drive Western producers out of business.

FORGE is a structurally sound response to a structural problem. But the timeline mismatch remains acute. China’s patient capital deployments have been compounding since 2013. FORGE’s price floors and Project Vault’s $10 billion stockpile reserve — significant as they are — are countermeasures to a position that took a decade to build. Refining parity cannot be closed by diplomatic communiqué.

The physical infrastructure of rare earth processing takes five to ten years to permit, finance, and commission. The Gallium Gap is not a 2026 problem. It is a 2030 problem at best — and only if capital deployment begins in earnest now.

Project Vault: A Buffer, Not a Fix

Project Vault, announced alongside FORGE and backed by a $10 billion Export-Import Bank loan — the largest in EXIM’s history — represents a strategic stockpiling initiative: a buffer against sudden supply disruption rather than a structural supply chain fix. It buys time. Whether that time is used productively depends on decisions that have not yet been made.

The Urban Mine — A Circular BRI Economy

There is a dimension of this dynamic that receives almost no analytical attention: the end of life. As hyperscalers — Microsoft, Google, Amazon, Meta — cycle through generations of AI hardware, retiring first-generation H100 clusters in favor of Blackwell and eventually Rubin systems, large volumes of GPU scrap flow back into Asia for processing and material recovery.

If China captures the recycling infrastructure for decommissioned AI accelerators, it creates what might be called a circular BRI economy — a system in which it need not mine new ore to maintain mineral dominance, because it is harvesting the urban mines of the West’s own AI buildout.

This is not hypothetical. China already controls the majority of global rare earth recycling capacity. The rare earths and specialty metals embedded in retired H100s and A100s — the cobalt, the tungsten, the trace rare earth elements in cooling fan magnets — are recoverable at commercially significant concentrations.

A vertically integrated Chinese recycling ecosystem would close the loop: BRI mines feed the front of the supply chain; e-waste recovery feeds the back. Western dependence on Chinese mineral processing would not diminish as the hardware fleet ages. It would deepen.

What This Means for Nvidia, Investors, and Policy

For Nvidia specifically, the risk calculus is mediated but compounding. As a fabless operation, Nvidia does not sit at the direct point of mineral exposure — TSMC and Samsung absorb the first-order supply disruption. But Nvidia is the downstream beneficiary and the ultimate constraint.

A 10 percent reduction in TSMC’s advanced node output capacity translates directly into fewer Blackwell GPUs available for hyperscaler delivery schedules. In a market where GPU allocation is a strategic asset and lead times run to quarters, that constraint has immediate and material consequences for revenue, data center buildout timelines, and the competitive dynamics of the AI infrastructure race.

Why Supplier Diversification Alone Cannot Close the Gap

The deeper issue is structural: mineral sovereignty in AI is not a risk that can be hedged through better supplier diversification alone. The refining parity gap, the patient capital asymmetry, and the 0.1 percent threshold rule operating in combination represent a multi-layered chokehold that no single procurement decision can dissolve. Addressing it requires sustained, loss-tolerant, state-adjacent capital deployment in Western processing infrastructure — precisely the kind of patient capital that public markets are structurally reluctant to provide.

What Investors Are Currently Mispricing

For investors, the implication is a recalibration of how AI hardware risk is priced. GPU demand forecasts that do not embed a mineral supply risk premium are, by this analysis, incomplete. The question is not whether China will use its export control architecture as leverage — it has already demonstrated that it will. The question is when, and under what conditions, the November 2026 truce expires into something less accommodating.

The Long View: Rubin and Beyond

The Silicon Shackle is not a conspiracy. It is an engineering problem with a geopolitical source — a long-run consequence of rational investment decisions made by Chinese state capital over fifteen years, now crystallized into structural dependency.

The Blackwell generation of GPUs that is currently powering the AI transition was, in part, made possible by minerals secured through BRI concessions signed in 2015. The Rubin generation, currently in development, faces the same upstream architecture.

And the generation after that will, absent significant structural intervention, face the same constraints — unless the West begins, at the level of industrial policy, to treat refining parity as the foundational AI infrastructure problem that it is.

Key Statistics

98.8%: China’s share of global gallium supply — the “Gallium Gap”

$32.6B: BRI metals & mining investment in 2025 alone

$19.5B: BRI copper & aluminum engagement in Kazakhstan, H1 2025

30%: TSMC reliance on Chinese chemical consumables for 7nm and below

Nov 2026: Expiry of gallium/germanium export ban suspension — next inflection point

Related article: China vs US AI Investment in Africa: The 2026 Scorecard