How Beijing built the continent’s digital backbone — and what that means for sovereignty, debt, and the next decade of African development.

- 70% of Africa’s 4G networks built by Huawei (estimated)

- $39B Chinese construction & investment in Africa, H1 2025

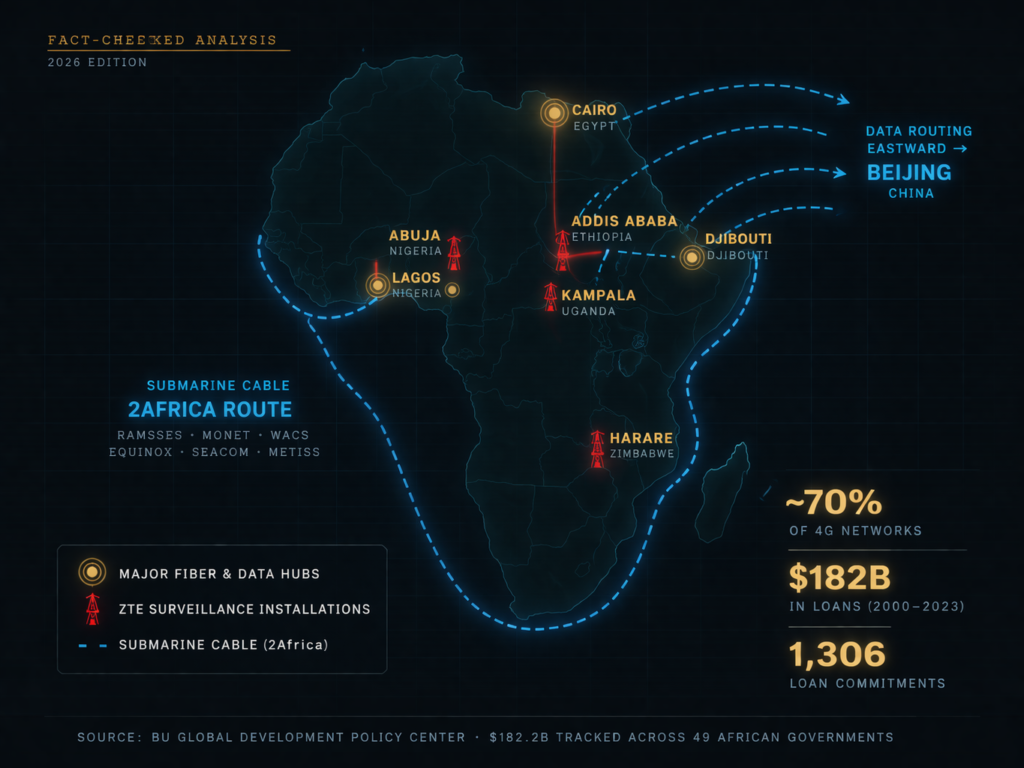

- $182B Total Chinese loans to Africa, 2000–2023

- 1,306 Loan commitments across 49 African governments

- 35+African countries with Chinese tech infrastructure

Map of Africa showing Chinese digital infrastructure networks — fiber optic routes, submarine cables, and surveillance tower locations — overlaid with data points.

The Scale and Surge of Investments

The digital backbone of Africa is being built in Beijing. As mobile phones proliferate across the continent and governments rush to digitize services, one nation has positioned itself as the indispensable architect of Africa’s technological future: China.

The Numbers Tell the Story

Chinese companies, led by Huawei, have built an estimated up to 70% of Africa’s 4G networks. This figure — widely cited from 2020 African Business and Deloitte data — refers to market share of equipment rather than total ownership. Analysts from the Carnegie Endowment place the range between 50% and 70% depending on methodology and whether core or radio access networks are counted. The imprecision matters: this is not merely market dominance, but the creation of technological dependency that will shape the continent’s digital trajectory for decades.

In the first half of 2025 alone, Chinese construction contracts and direct investments in Africa reached $39 billion — surpassing Chinese engagement in every other region globally. This surge confirms that the Digital Silk Road, the technological component of China’s Belt and Road Initiative, has made Africa its primary theater of operation.

From 2000 to 2023, China provided $182.28 billion in loans across 1,306 commitments to 49 African governments, with a significant subset funding tech infrastructure including:

- Telecommunications networks (4G/5G towers, fiber optic cables, satellite communications)

- Data processing facilities (data centers, cloud platforms)

- Control systems (smart city platforms, surveillance equipment, e-government services)

Africa as the BRI Priority

Africa has become China’s top priority region for Belt and Road investments. Nigeria secured substantial Chinese deals in the first half of 2025, primarily concentrated in oil and gas infrastructure — specifically large energy projects such as the Ogidigben Gas Revolution Industrial Park. This macroeconomic relationship creates favorable conditions for parallel tech infrastructure deployment, but the bulk of these contracts are in energy, not digital technology. Actual technology and manufacturing engagement in Nigeria for 2025 was closer to $1–3 billion, focusing on data centers and green energy systems.

African Leaders’ Perspective

Kenyan President William Ruto has stated that “China has a special place to enhance the competitiveness of Africa,” while Ethiopian Prime Minister Abiy Ahmed noted that “China continues to be a critical partner for Ethiopia.” This reflects how many African governments view Chinese engagement as essential for rapid development.

Why This Database Matters

Information about Chinese tech projects in Africa exists in fragments: buried in opaque loan agreements, scattered across government announcements, or deliberately obscured by non-disclosure clauses. This fragmentation isn’t accidental — it serves parties who benefit from complexity and lack of transparency.

The Chinese Loans to Africa Database, maintained by Boston University’s Global Development Policy Center, tracks 1,306 loan commitments totaling $182.28 billion between 2000 and 2023, and serves as the primary empirical foundation for this analysis. It is supplemented by African telecommunications regulators’ reports, Chinese Ministry of Commerce announcements, company annual reports, investigative journalism, investor presentations, and academic research.

Critical limitations apply throughout: many contracts contain NDAs preventing full disclosure; project costs are often contested; the gap between announced and delivered projects can be substantial; and projects with the highest strategic significance — military and intelligence-related — are deliberately hidden within commercial entities.

A digital infographic shows three engineers—representing Huawei, ZTE, and China Telecom—overlooking a futuristic city in Ethiopia at sunset

The Companies Building Africa’s Digital Future

Huawei Technologies: The Undisputed Leader

Huawei dominates an estimated up to 70% of Africa’s 4G backbone and leads 5G expansion across 30 markets, embedding systems into critical national infrastructure. The company has evolved from equipment vendor to total solution provider through All-Scenario Intelligent Campus Solutions (hardware, cloud platforms, big data, AI), the EM 2.0 Model deeply embedding Huawei in operators’ strategic planning, and training programs that have equipped over 120,000 Africans — while ensuring expertise remains tied to Chinese technology.

After U.S. sanctions in 2019 cut access to advanced semiconductors and Google services, Huawei pivoted toward enterprise solutions, cloud services, and higher-value recurring-revenue offerings — leveraging its already installed network infrastructure base. In Egypt, Huawei operates the largest regional cloud data center in Africa and supplies network equipment to all four major Egyptian telecommunications operators.

ZTE Corporation: The Cost-Competitive Alternative

ZTE served as Ethiopia’s exclusive telecom equipment supplier from 2006 to 2009 and built the national network extensively. The company specializes in government surveillance contracts, lower-cost telecommunications equipment, and “Safe City” projects. ZTE’s competitive advantage is approximately 30% lower prices than Western competitors.

Notable projects include Ethiopia’s Addis Ababa Safe City (1,900+ cameras with facial recognition), Nigeria’s Abuja surveillance initiative ($470 million contract, though significantly hampered by funding shortfalls rather than technical issues), and Zimbabwe’s nationwide camera networks.

China Telecom Global: Controlling Data Highways

Less visible than equipment manufacturers, China Telecom Global controls submarine cable landing stations, operates Points of Presence (PoPs) across the continent, and participates in major cable consortia. The 2Africa cable — a 45,000-kilometer system encircling Africa — is now fully operational as of 2025, significantly reducing wholesale bandwidth costs. Significant volumes of African internet traffic to Asia and Europe physically pass through Chinese-controlled infrastructure, with clear implications for data sovereignty.

StarTimes: The Soft Power Amplifier

As of 2026, StarTimes has approximately 13 million DVB subscribers and 20–27 million OTT users across 28 African countries. The company controls cultural pipelines into African homes, links content distribution with underlying Chinese network infrastructure, and achieves dual leverage: infrastructural control combined with cultural influence.

CloudWalk Technology: AI Training Ground

CloudWalk operates Zimbabwe’s facial recognition system with an explicitly stated purpose: using Zimbabwe as a training environment for AI algorithms to better recognize individuals with darker skin tones. “The differences between technologies tailored to an Asian face and those to a black one are relatively large, not only in terms of color, but also facial bones and features,” explained CloudWalk CEO Yao Zhiqiang.

Ethical Concerns

Zimbabwe sends facial data on millions of citizens captured by CCTV cameras to CloudWalk to improve its AI systems. Citizens become unwitting participants in AI training without consent. Biometric data — unique and permanent — is used to develop systems potentially deployed for political control, creating a feedback loop where repression in one country generates data improving systems deployed elsewhere. Implementation has faced delays due to Zimbabwe’s currency instability, but the architecture of the arrangement remains intact. 03 — Financial Backbone

Financial Backbone: Policy Banks and Vendor Financing

China Export-Import Bank (Exim Bank)

The world’s third-largest export credit agency provides concessional bilateral loans for major national projects. Typical maturities run 15–20 years with grace periods up to 8 years. Interest rates of 1–6% are significantly higher than World Bank IDA rates of 0.75–1.5% — a point of candor often missed in pro-BRI commentary. All loans carry a tied aid mandate: borrowers must use Chinese contractors, Chinese equipment, and often Chinese labor.

Vendor Financing: The Irresistible Offer

Perhaps the most powerful financing tool is direct lending by Huawei and ZTE, backed by state reserves. African telecom operators need network upgrades to remain competitive but lack capital and creditworthiness for favorable loans from Western banks. Traditional financing requires environmental studies, governance reviews, detailed projections, and lengthy approvals.

“We’ll provide the equipment now. You can pay us back over several years. Interest rates will be reasonable. The network will be operational in months.”

For operators in fast-growing markets where competitors are also expanding, the ability to deploy immediately while deferring payment (3–7 years typical) explains much of Chinese success in Africa — more than technological superiority or cost advantages alone.

Comparative Financing Terms

| Lender | Interest Rate | Maturity | Grace Period | Speed | Key Conditions |

|---|---|---|---|---|---|

| China Exim Bank | 1–6% | 15–20 years | Up to 8 years | Fast (months) | Tied aid — Chinese contractors/equipment required |

| China Dev. Bank | ~5–7% (market) | 5–10 years | Varies | Fast (months) | Project commercial viability |

| Huawei/ZTE Vendor | Subsidized/deferred | 3–7 years | Short | Very fast (weeks) | Exclusive use of vendor equipment |

| World Bank IDA | 0.75–1.5% | 25–40 years | 5–10 years | Slow (years) | Governance reforms, environmental standards, competitive procurement |

| African Dev. Bank | ~2–4% | 15–20 years | 3–5 years | Moderate (6–18 months) | Regional development alignment |

| EU Development Finance | 0–3% (blended) | 20–30 years | 5–10 years | Slow (years) | Environmental standards, labor rights, transparency |

| U.S. DFC | ~6–8% (near-market) | 10–15 years | Limited | Moderate (6–12 months) | Private sector participation, U.S. strategic interests |

Regional Deep Dives

East Africa: Strategic Laboratory

Kenya (~$1.5–2.5B estimated), Ethiopia (~$3–4B), and Djibouti (dual-use data center adjacent to PLA naval base) form the densest concentration of Chinese digital infrastructure on the continent.

West Africa: Scale & Complexity

Nigeria is China’s largest single African engagement partner. Nigerian authorities deliberately diversify vendors, splitting 5G contracts among Huawei, Ericsson, and ZTE as a conscious hedge against dependency.

Southern Africa: Resistance & Dependency

South Africa is the outlier with notably lower Chinese tech investment, driven by advanced existing infrastructure, U.S. diplomatic pressure, and vocal domestic civil society.

North Africa: Megaproject Model

Egypt is the largest recipient of Chinese tech infrastructure investment in Africa, anchored by the New Administrative Capital — where Chinese firms now operate, not just build.

Central Africa: The Next Frontier

DRC, Cameroon, and Congo-Brazzaville remain the least digitally penetrated by Chinese infrastructure. Lower economic development and political instability create barriers — for now.

Zimbabwe: Surveillance Laboratory

The 2018 CloudWalk partnership explicitly uses Zimbabwe as an AI training environment, sending facial data on millions of citizens to China to improve algorithm accuracy on darker skin tones.

Ethiopia: Deepest Chinese Technological Penetration

Ethiopia’s network was built almost entirely by ZTE and Huawei. Total estimated tech investment: $3–4 billion, including the complete national 2G/3G/4G build-out by Ethio Telecom ($1.6+ billion known investment) and Addis Ababa’s Safe City project with over 1,900 cameras with facial recognition.

During Ethiopia’s civil conflict (2020–2022), Human Rights Watch documented that Ethiopian security officials have virtually unlimited access to call records and regularly record phone calls without legal process or oversight — through systems built and maintained by Chinese companies. Whether Chinese technicians provided active operational support during hostilities remains unconfirmed.

Ethiopia also represents a success case for African negotiating agency: Ethiopian negotiators successfully inserted clauses requiring technology transfer commitments and significant local employment — demonstrating that state capacity and political will can extract better terms.

Egypt: The Build-Operate-Maintain Model in Action

Egypt is the largest recipient of Chinese tech infrastructure investment in Africa, driven by the New Administrative Capital (NAC) — planned for 6.5 million people, 45 kilometers east of Cairo. 85% of the Central Business District funding comes from Chinese lenders, including a $2.2 billion loan from China Exim Bank.

China State Construction Engineering Corporation has moved beyond construction into long-term operational control through a joint venture with Egyptian partners — granting Chinese firms decades of operational access to smart city services, surveillance systems, and digital government platforms, with recurring revenue from service fees. Rather than building and departing, Chinese companies maintain operational access to sensitive systems indefinitely.

Djibouti: Strategic Ambiguity by Design

This tiny nation hosts China’s only established overseas military base and serves as a critical submarine cable landing point. The Djibouti Data Center, built by China Merchants Group in 2018, sits adjacent to both the Doraleh Multipurpose Port and the People’s Liberation Army naval base — creating deliberate dual-use capabilities where commercial data center operations can support military intelligence gathering and naval operations.

Surveillance, Security, and Human Rights

Uganda: Direct Political Surveillance Allegations

In 2019, reports emerged alleging that Huawei employees accessed encrypted communications on behalf of the Ugandan government to surveil opposition politician Bobi Wine following a $126 million CCTV procurement. The allegations include interception of WhatsApp messages, location tracking, and intelligence provision to security services. Both the Ugandan government and Huawei denied the allegations; no independent technical verification has been publicly released.

The fundamental structural question: when foreign companies install and maintain sensitive surveillance infrastructure, what prevents them from providing operational support to authoritarian governments? Technical capabilities exist, political incentives are clear, and lack of transparency in contracts makes oversight nearly impossible.

The African Union Headquarters Breach

In 2018, Le Monde revealed that the Chinese-built AU headquarters in Addis Ababa had allegedly been secretly sending data nightly to Shanghai servers for five years. The Chinese government and construction companies denied the allegations. The AU conducted an investigation but released limited public findings, then swiftly moved to install new, non-Chinese systems. The incident was never fully resolved from a technical perspective — no independent audit results were published.

Notably, the breach did not stop Chinese-African tech cooperation, demonstrating the complex balance between security concerns and development needs.

The Backdoor Question

Despite extensive investigation, no confirmed, widespread hardware backdoor in Huawei equipment has been publicly documented with technical proof. The UK’s Huawei Cyber Security Evaluation Centre identified serious security shortcomings in Huawei code but did not confirm deliberate backdoors.

The risk persists structurally: Chinese national security laws require companies to cooperate with intelligence services when requested. The theoretical capability for China to compel Huawei to insert backdoors, combined with the technical access Huawei personnel require to maintain networks, creates vulnerability even without definitive exploitation evidence. For African nations, definitive proof of backdoors would likely only emerge after significant exploitation — making the decision political and strategic rather than purely technical.

Technology Transfer: Reality vs. Rhetoric

The Training Reality

Huawei’s “Seeds for the Future” program has trained over 120,000 students globally with significant African participation through training centers, scholarships, and internships in China. What is actually being transferred is largely the ability to operate and maintain Chinese proprietary equipment. Students learn to use Chinese systems, not to design alternatives or understand vendor-neutral principles.

This creates “trained dependency”: countries develop local expertise, but that expertise is non-transferable to other vendors’ equipment. When a Kenyan engineer spends five years learning Huawei systems, switching to Ericsson means that expertise becomes obsolete.

Success Cases: African Agency Works

Ethiopia successfully demanded specific technology transfer clauses and job creation requirements. Benin similarly leveraged its bargaining position to extract better terms. Common characteristics of successful negotiations:

- Unified government negotiating teams

- Clear priorities established before negotiations begin

- Willingness to walk away from deals not meeting requirements

- Long-term strategic planning beyond immediate connectivity needs

Success Stories: When Chinese Infrastructure Works

Ethiopia’s Rural Connectivity Revolution

Chinese-built telecommunications networks, financed rapidly through vendor loans to Ethio Telecom, extended 4G coverage into remote, low-profit rural areas. Western vendors consistently deemed rural Ethiopian coverage financially unattractive. Chinese vendor financing changed the calculation by offering deferred payment and accepting higher risk. Farmers now access weather forecasts and market prices; students connect to educational resources; health workers coordinate emergency responses; mobile money enables financial inclusion for populations previously without bank access.

Rwanda’s Multi-Vendor Success

Rwanda achieved over 90% broadband coverage while maintaining relative vendor diversity — a rare success in avoiding lock-in. The government utilized Chinese infrastructure financing while consciously treating it as one option within a competitive landscape, simultaneously engaging European vendors and multilateral lenders. The result: a thriving domestic tech sector, lower connectivity costs, and sufficient vendor diversity to preserve bargaining power. The model: leverage Chinese financing for rapid deployment, but maintain sufficient vendor diversity to preserve options for future transitions.

The 2Africa Cable

Now fully operational as of 2025, the 2Africa cable significantly increases regional bandwidth and decreases latency to global economic hubs. Lower latency to Europe and Asia improves video calls and cloud computing performance for all African users regardless of domestic network vendor — demonstrating that not all Chinese infrastructure follows the same concerning pattern.

The image contrasting two major Western tech initiatives, set against a blurred photographic background of a modern Lagos, Nigeria, cityscape at dusk.

The Competitive Landscape: Alternatives Emerge

U.S. Efforts: Limited but Targeted

The U.S. Clean Network initiative (2020) to exclude Chinese vendors from 5G networks largely failed in Africa. The U.S. has since shifted to targeted alternatives through the Partnership for Global Infrastructure and Investment (PGII) and DFC financing — focusing on specific high-value projects like the Lobito Corridor railway and telecommunications project connecting Zambia, DRC, and Angola. Structural disadvantages persist: the approach relies on private sector mobilization, requires extensive environmental and governance reviews, and comes with higher standards that increase costs. African nations frequently find U.S. alternatives cannot match Chinese offers on speed, scale, and certainty of financing.

European Union: Ambitious Plans, Slow Implementation

The EU launched Global Gateway in 2021, pledging to mobilize €300 billion by 2027 as a direct alternative to the BRI. Deployed capital remains much smaller than BRI volumes. The EU’s multi-stakeholder, consensus-driven decision-making creates bureaucratic delays that countries seeking immediate connectivity cannot accommodate. Global Gateway’s strength lies in higher standards — stronger environmental protections, labor rights, anti-corruption measures — but these standards increase costs and lengthen timelines.

India, South Korea, and Japan

India pursues training, technical cooperation, and software services over hardware dominance. India’s positioning as a fellow developing country with democratic governance offers diplomatic advantages, but financing capacity remains limited. South Korea and Japan offer quality over quantity — Samsung’s emergence as a 5G vendor provides an alternative to the Huawei-Ericsson-Nokia triangle — but like Western competitors, these alternatives struggle with scale and speed.

The Future: 2025–2030

Belt and Road 2.0: From Construction to Operation

China’s infrastructure strategy is evolving. The Build-Operate-Maintain model pioneered in Egypt’s New Administrative Capital represents the future template — Chinese firms increasingly seek long-term operational control rather than one-time construction payment. The next major competitive arena won’t be physical networks but cloud computing, AI, and data analytics platforms. Huawei’s establishment of regional cloud facilities creates a second layer of dependency: even if a country eventually diversifies physical network vendors, migrating government data and enterprise systems from established cloud platforms is extraordinarily expensive and disruptive.

African Agency: The Variable That Matters Most

Nations are demonstrating increasing sophistication through vendor diversification, growing regional coordination, indigenous capacity building, regulatory frameworks for data sovereignty, and strategic patience to allow competitive alternatives to mature. The future trajectory depends less on Chinese strategy than on African responses.

The Debt Reckoning

Zambia’s 2023 debt restructuring revealed Chinese preferences: extend maturity periods, preserve principal amounts, adjust interest rates, and avoid significant haircuts on loan face value. This approach — a debt treadmill rather than a debt trap — maintains long-term leverage while avoiding politically costly asset seizures. Perpetual debt service, even at adjusted rates, creates ongoing dependency with the creditor maintaining influence over budget priorities and diplomatic positioning for decades.

Technology Evolution: Beyond 5G

Starlink’s expansion into Africa creates genuine competition for rural connectivity, potentially undermining a key justification for Chinese infrastructure loans. Chinese companies are developing competing satellite constellation projects but lag SpaceX technologically. Open RAN technology could theoretically break Huawei-Ericsson-Nokia oligopoly, allowing smaller vendors and African companies to enter markets — though it requires more technical sophistication from operators. China leads globally in quantum communication technology, and if quantum-encrypted communications become strategically important, Chinese technological leadership could extend dominance into next-generation infrastructure. 10 — Conclusion

Digital Dependency and African Futures

China has built Africa’s digital backbone. This isn’t rhetoric — it’s documented fact: an estimated up to 70% of 4G networks, hundreds of thousands of kilometers of fiber, data centers processing massive traffic flows, surveillance systems watching millions of citizens, and cloud platforms hosting government services all trace back to Chinese financing, construction, and operation.

This infrastructure works. It provides connectivity, enables digital services, and accelerates development. Rural Ethiopian farmers access market prices. Kenyan entrepreneurs launch digital businesses. Egyptian government services migrate online. These are genuine benefits that alternative financing couldn’t have delivered at comparable speed and scale.

But the infrastructure also creates vulnerability: debt burdens contributing to fiscal crisis, technical dependency making vendor switching prohibitively expensive, surveillance capabilities enabling authoritarian control, and data flows through foreign-controlled systems persisting for decades.

Beyond Simple Narratives

This is neither pure development assistance nor pure neocolonial exploitation. It is a sophisticated, strategic relationship where both parties pursue national interests, with deeply asymmetric power dynamics favoring China but not eliminating African agency entirely. The critical variable for Africa’s digital future isn’t Chinese strategy — that is relatively clear and consistent. It is African responses: the quality of negotiations, sophistication of regulations, commitment to vendor diversity, investment in indigenous capacity, and willingness to coordinate regionally.

Nations that approach strategically can extract maximum technology transfer, maintain vendor diversity, manage debt sustainability, and protect data sovereignty. Nations that accept without serious negotiation face single-vendor dependencies, ignored debt burdens, and compromised data sovereignty.

The networks are already operational. The data already flows through Chinese systems. The question now is what happens next.