China’s economic and technological relationship with Africa is the most consequential geopolitical story of the 21st century — and most people still underestimate it.

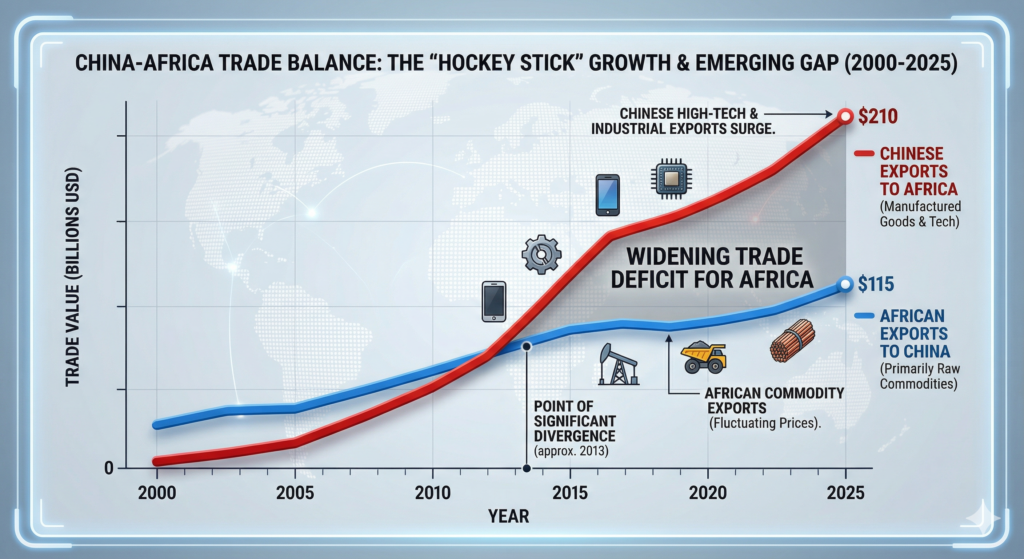

In 2024, trade between China and African countries reached $295.6 billion, a new record for the fourth consecutive year, and China has been Africa’s largest trading partner for 16 straight years. By the first eight months of 2025, bilateral trade had already hit $222 billion — up 15.4 percent year on year — suggesting the trajectory is accelerating rather than plateauing.

But trade figures only capture the surface layer. Underneath those numbers, Chinese companies dominate 70 percent of Africa’s 4G backbone infrastructure, Chinese-financed railways thread through mineral corridors in the DRC and Zambia, and AI-powered surveillance cameras from Huawei, ZTE, and Hikvision watch city streets from Nairobi to Lusaka to Abuja.

Meanwhile, tens of thousands of African students train annually in Chinese universities, absorbing technical standards that will shape the continent’s digital architecture for decades — long after any particular trade agreement has expired.

What makes this moment distinct from any previous phase of the relationship

Africa is no longer a passive recipient. Governments across the continent are becoming sharper, more coordinated negotiators. They are banning raw mineral exports to force local processing investment.

They are using Gulf capital — from the UAE and Saudi Arabia — as deliberate leverage against Chinese financing terms. Governments are expanding BRICS+ membership to diversify their financial relationships away from both Beijing and Washington. And they are watching closely as US tariff escalation pushes Beijing to treat Africa not merely as a supplier of raw materials, but as a strategic consumer market in its own right.

This guide maps every layer of that footprint. It addresses the debt trap controversy — and covers five dimensions:

- The downstream industrialisation question,

- Agricultural technology as soft power,

- The invisible battle over technical standardisation,

- Private Chinese entrepreneurship,

- And the emerging Gulf rivalry for African mineral rights and port management.

Each section links to a dedicated spoke article for deeper analysis.

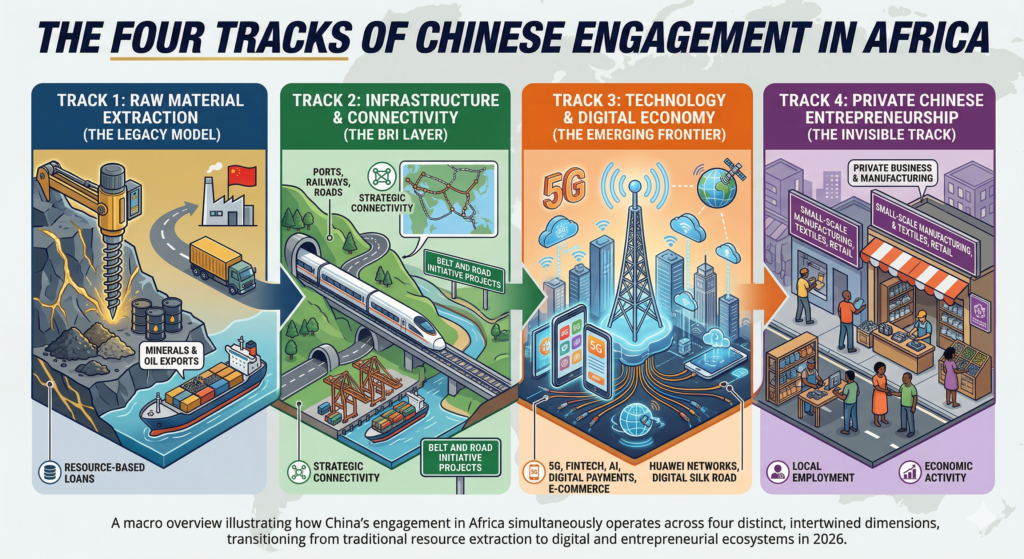

A conceptual diagram showing four overlapping tracks of Chinese engagement: a mining drill for raw materials, a railway for BRI infrastructure, a 5G tower for the digital economy, and a storefront for private entrepreneurship.

The Macro Framework: China’s Four Tracks in Africa

To understand how China operates in Africa, it helps to think in tracks rather than sectors. Because China’s engagement has evolved through four distinct operational modes — and all four are running simultaneously in 2026.

Collapsing them into a single narrative produces the kind of oversimplification that makes both Beijing’s defenders and its critics sound like they are talking about different countries.

Track 1: Raw material extraction — the legacy model

For the first decade of the 21st century, the relationship followed a clear pattern. Africa exported raw materials — oil from Angola, copper from Zambia, cobalt from the DRC — and China exported manufactured goods in return.

Chinese state-owned enterprises and their financing arms extended loans and built infrastructure in exchange for access to those resources, with Angola, the DRC, and Zambia becoming the archetypes of the model. It still operates today, but framing China’s Africa strategy primarily through this lens is like describing a river by its source rather than its current course.

Track 2: Infrastructure and connectivity — the BRI layer

The Belt and Road Initiative, formalised from 2013 onward, gave Beijing a structured financing instrument for ports, railways, roads, and energy projects that reshaped African connectivity — and simultaneously created the debt dynamics that have since generated enormous controversy.

Since 2022, however, this track has evolved significantly away from prestige megaprojects. Beijing now calls the updated model “Xiao Er Mei” — small and beautiful — shifting emphasis toward smaller, more targeted investments in technology and energy that are harder to unpick and more deeply embedded in local economic systems.

Track 3: Technology and the digital economy — the emerging frontier

This is the fastest-growing track and the one with the deepest long-term implications for African sovereignty. It covers Huawei’s 5G networks, Chinese fintech platforms, AI-powered smart city systems, agri-tech platforms, and the e-CNY digital yuan. And it matters not just because of what it builds, but because of what it determines: whose technical standards, whose data infrastructure, and whose governance models will shape the continent’s digital development for the next fifty years.

Track 4: Private Chinese entrepreneurship — the invisible track

This track receives the least attention in strategic analysis, yet generates the most day-to-day economic activity and the most cultural friction.

Hundreds of thousands of private Chinese entrepreneurs have moved to African cities to set up small-scale manufacturing in plastics, textiles, furniture assembly, and electronics repair — operating entirely outside FOCAC frameworks and BRI financing. They hire local workers, compete with local businesses, and generating both opportunities and tensions that look nothing like the SOE model.

As the continent’s leading smartphone provider with a 48% market share in 2025, Transsion Holdings—the maker of TECNO, Infinix, and itel—serves as the ultimate ‘Trojan Horse’ for Chinese digital influence, pre-installing a closed-loop ecosystem of mobile payment apps and the continent’s most popular music streaming service, Boomplay, directly into the pockets of Africa’s youth.

Understanding China’s Africa presence without accounting for this track produces a picture that is clean and legible but fundamentally incomplete.

How the trade model is shifting

The 2025 Blue Book of China-Africa Economic and Trade Cooperation describes the directional shift plainly: China-Africa trade is moving away from a purely resource-based model toward something more diversified, high value-added, and technology-intensive.

New sectors are expanding rapidly — telecommunications, digital economy, green energy, and financial services — and Chinese EV manufacturers are eyeing African assembly plants as both a production base and a market.

Solar panel exports to Africa jumped 60 percent in the twelve months to June 2025, with the continent importing over 15,000 megawatts of Chinese solar capacity in that period — a number that reflects both genuine energy demand and Beijing’s need to redirect manufacturing exports away from US tariff pressure.

The trade deficit problem

Despite that diversification, Africa’s structural position in the trade relationship remains deeply asymmetric. Africa’s top five exporters to China in 2024 were the DRC, Angola, South Africa, Guinea, and Zambia — all selling primarily minerals and oil, according to Johns Hopkins’ China Africa Research Initiative — while Africa’s imports from China hit $179 billion in 2024 against exports of just $99 billion.

That widening imbalance is the central grievance African negotiators carry into every forum. And it explains why FOCAC 2024 focused so heavily on market access and zero-tariff commitments. The gap between what Africa sells and what it buys from China is not just an economic statistic — it is the fundamental source of tension that shapes every other dimension of this relationship.

Why Africa matters more to China in 2025 and 2026

Several converging pressures explain why Beijing’s Africa engagement is intensifying rather than plateauing. Critical mineral supply chains for electric vehicles and battery technology depend on African resources — cobalt from the DRC, copper from Zambia, and lithium from Zimbabwe.

As the clean energy transition accelerates, so does the strategic premium on securing those supply chains. Africa’s 1.4 billion people represent a growing export market at precisely the moment US tariffs are closing off access to American consumers, while African voting blocs at the United Nations and in multilateral institutions carry genuine diplomatic weight in the competition between Beijing and Washington for global influence.

Most immediately, US tariff escalation is the single largest driver of China’s Africa pivot in 2025 and 2026. Chinese exports to Africa surged 24.7 percent in the first eight months of 2025, with solar panels, electronics, vehicles, and machinery flowing south in volumes not seen since the height of the commodity supercycle.

This is economic redirection, not altruism, and it will intensify as the trade war with the United States deepens.

The Western counter-narrative

The G7’s Partnership for Global Infrastructure and Investment has pledged $600 billion globally, and the EU’s Global Gateway has committed €300 billion with half earmarked for Africa. The US and EU-backed Lobito Corridor railway — connecting mineral-rich Zambia and the DRC to Angola’s Atlantic coast — is explicitly framed as a sustainable alternative to Chinese BRI financing.

These initiatives represent genuine Western strategic recalibration, but they face a structural problem that no amount of political will has yet resolved. Western private capital demands risk-adjusted returns that African infrastructure projects rarely offer without substantial subsidy, whereas Chinese state capital can tolerate longer timeframes because it is serving strategic objectives rather than purely commercial ones.

A line chart showing the ‘hockey stick’ growth of China-Africa trade from 2000 to 2025, highlighting the widening gap between African exports (primarily raw commodities) and Chinese imports (manufactured goods and tech).

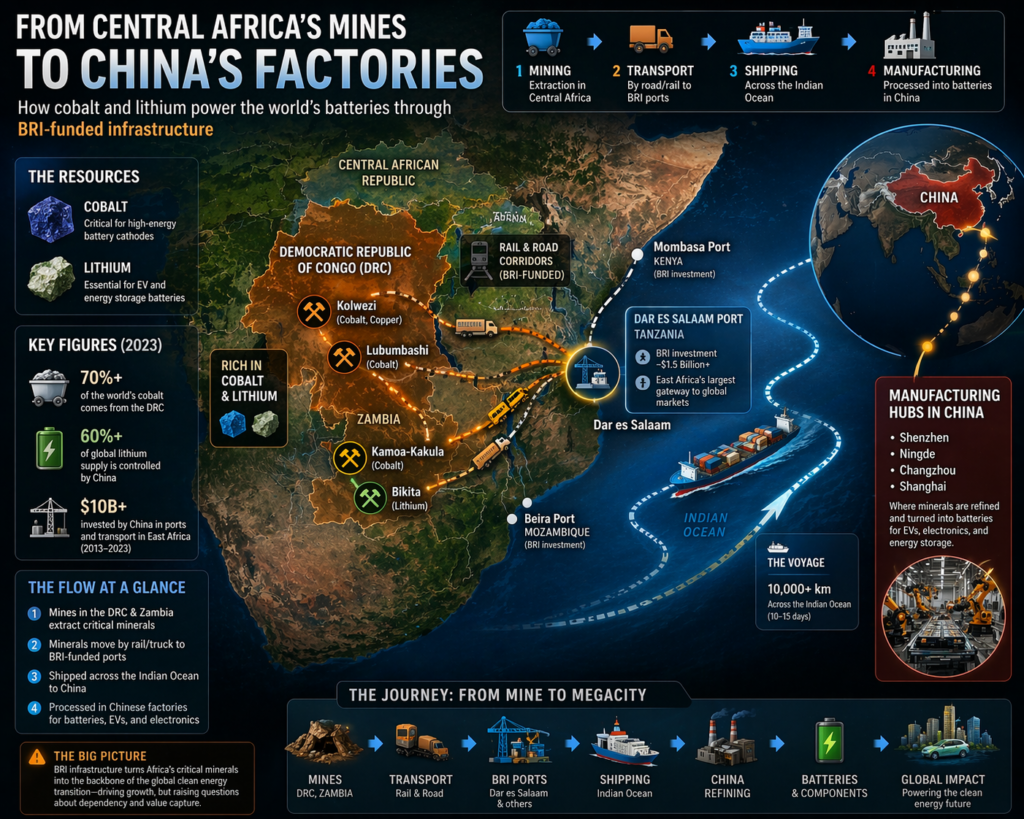

Belt and Road Initiative: Minerals, Corridors, and the “Small and Beautiful” Pivot

The Belt and Road Initiative now covers nearly all of Africa’s 54 states, and since its launch in 2013 it has funded ports, railways, energy infrastructure, and telecommunications networks across the continent. In 2023 alone, African countries received $21.7 billion in BRI cooperation agreements — a figure that tells you something important about the BRI’s current scale but very little about its evolving character.

Why minerals are the BRI’s core logic in Africa

The Belt and Road Initiative Africa minerals story is inseparable from the global clean energy transition. Electric vehicle batteries require cobalt, copper, lithium, and manganese at industrial scale, and Africa holds an outsized share of global reserves of each.

China recognised this strategic reality before most Western governments and used the BRI as a financing instrument to act on that recognition — building the railways, ports, and logistics infrastructure that move those minerals from inland extraction sites to ocean-facing export terminals.

The countries most deeply integrated into this system — the DRC, Zambia, Zimbabwe, Guinea, and South Africa — are all resource-rich economies where Chinese state-linked companies have taken significant equity stakes or operating roles in the sectors that matter most to Beijing.

An infographic mapping the flow of cobalt and lithium from Central African mines through BRI-funded ports like Dar es Salaam, ending at manufacturing hubs in China.

The pivot to “small and beautiful”

The BRI of 2026 looks significantly different from the BRI of 2015, and understanding that evolution matters for interpreting where Chinese capital is actually flowing.

A wave of large infrastructure projects ran into debt sustainability problems in the late 2010s, generating both financial losses for Chinese lenders and the reputational damage of the “debt trap” narrative in Western media. Beijing’s response, from 2022 onward, was to pivot deliberately toward smaller, more targeted investments in energy, technology, and agricultural processing — the “Xiao Er Mei” model that prioritises returns that are harder to criticise and deeper to unwind.

The FOCAC 2024 action plan committed China to deliver 1,000 “small yet beautiful” livelihood projects between 2025 and 2027, a deliberate rebranding away from dam-and-highway diplomacy toward an image of granular, community-level development.

The TAZARA railway rehabilitation — elevated to a signature commitment at FOCAC 2024 — illustrates the duality. It is simultaneously a livelihood project improving connectivity in Tanzania and Zambia, and a mineral logistics corridor connecting inland mining districts to Indian Ocean ports. China has not abandoned infrastructure ambitions. It has made them more precisely targeted at the supply chains that matter most to its own industrial economy.

A more sophisticated form of resource access

Rather than simply financing a railway in exchange for a commodity off-take agreement — the transaction logic of the early BRI — China now invests in processing capacity, battery precursor supply chains, and Special Economic Zones that embed Chinese economic presence more deeply and make it more difficult to reverse.

The goal is the same as it has always been: securing supply for China’s industrial economy. But the method is subtler, more integrated, and harder to unpick — which is precisely the point.

The Downstream Shift: Africa’s Fight for Local Processing

One of the most significant and underreported developments in China-Africa minerals is the question of what happens after extraction — and African governments are increasingly demanding a different answer.

Rather than simply mining raw materials and shipping them to Chinese refineries and processing facilities, a growing number of African governments are insisting that the refineries, smelters, and battery component factories be built on African soil, where the economic value of processing stays in-country.

The export ban wave

Zimbabwe moved first, banning the export of unprocessed lithium ore in 2022 to force foreign investors — including Chinese firms — to build processing capacity in-country rather than extract and export.

Namibia followed with restrictions on unprocessed critical minerals, and Zambia is actively negotiating to ensure more of its copper is processed domestically before export.

Nigeria has pushed for local refining capacity in its oil sector along similar lines. Taken together, these moves represent a structural shift in how African governments approach resource sovereignty — a shift from negotiating access terms to negotiating value retention.

The tension at the heart of the relationship

This creates a direct and unresolved tension at the centre of the China-Africa minerals relationship, because China’s manufacturing dominance in electric vehicle batteries, solar panels, and consumer electronics depends partly on its control over the refining and processing stages of the critical minerals supply chain.

Moving those stages to Africa would raise Chinese production costs and reduce Beijing’s control over the supply chains that underpin its green technology industrial strategy. As a result, Beijing has shown limited enthusiasm for local processing commitments, even as FOCAC communiqués gesture broadly toward “industrialisation” as a shared goal.

Some Chinese firms have built processing capacity in African countries when forced to by regulation. Many have not, and the gap between the “industrialisation” rhetoric in FOCAC documents and the reality of Chinese investment patterns on the ground remains wide.

This is not a uniquely Chinese failing — Western mining companies operating in Africa have an equally poor record of building processing capacity in-country — but China’s current dominance in global refining makes its behaviour on this question particularly consequential for Africa’s long-term development trajectory.

The downstream shift question is ultimately the most honest test of whether China’s engagement in Africa is genuinely oriented toward African industrialisation or primarily toward securing raw material flows at the lowest possible cost.

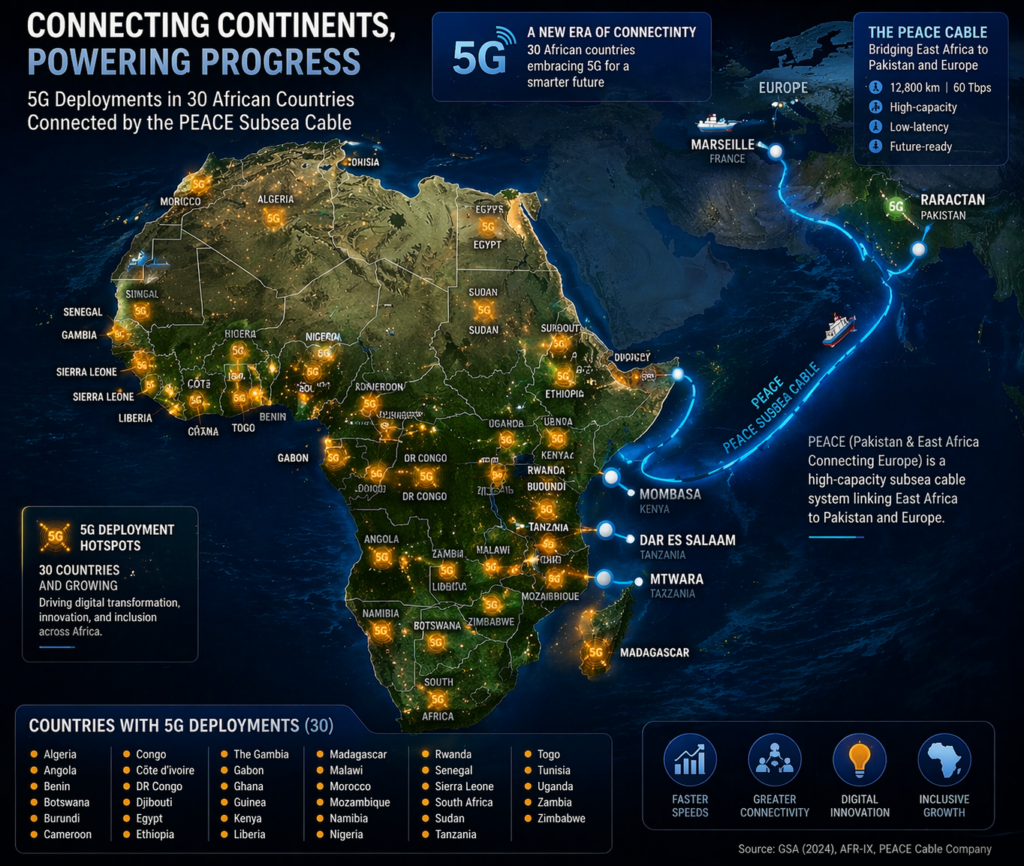

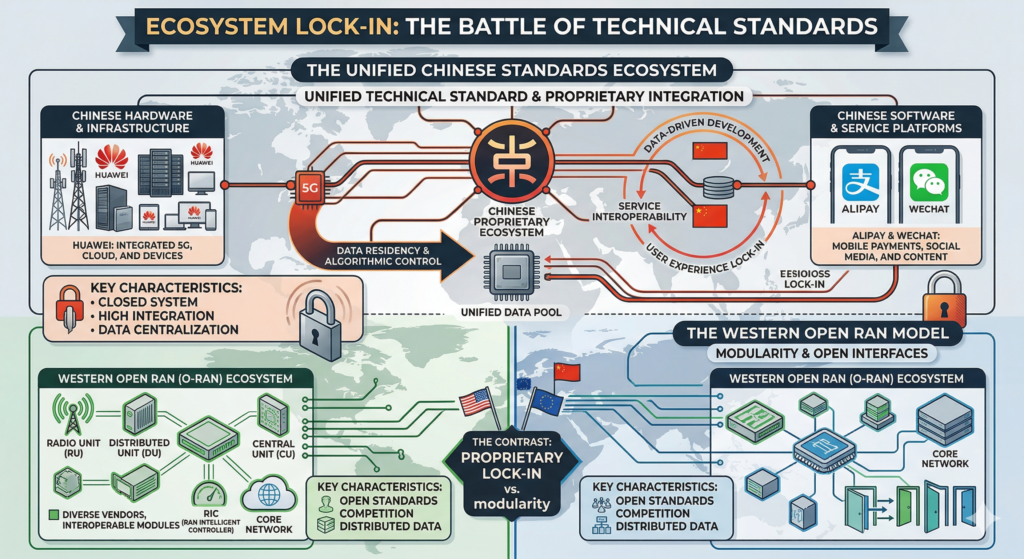

Huawei’s 5G Expansion and the Technical Standardisation War

The Huawei Africa 5G expansion is arguably the most strategically significant dimension of China-Africa technology trade, for a simple reason: telecommunications infrastructure is not easily replaced once installed.

Huawei entered Africa’s telecoms market in Kenya in 1998 and by 2005 had become one of the continent’s leading providers. It now dominates 70 percent of Africa’s 4G backbone and leads 5G rollouts across 30 African markets, with local training programmes that have certified over 120,000 African technicians — creating not just hardware dependency but a professional class whose skills are calibrated to Huawei’s systems.

South Africa: where 5G and mining converge

The most revealing recent development is the MTN-Huawei-China Telecom partnership in South Africa, formalised at AfricaCom in late 2024. In March 2025, MTN Group and Huawei signed a strategic MoU at MWC Barcelona, with the flagship project being Africa’s largest 5G-enabled private network — deployed for a manganese mining company in South Africa’s Northern Cape.

The network integrates worker monitoring, vehicle tracking, unmanned trucks, and energy management into a single 5G-connected industrial system, and it previews precisely how Chinese 5G infrastructure and industrial IoT are converging in Africa’s extractive sector.

Since MTN launched its South African 5G network in 2020, coverage has expanded from 25 percent to 44 percent of the population, with 900 new 5G sites added in 2024 alone. According to the GSMA Mobile Economy Sub-Saharan Africa 2024 report, 5G is expected to contribute $10 billion to the region’s economy by 2030 — a projection that, if realised, will be built almost entirely on Huawei’s hardware.

Country-by-country: an embedded presence

The South Africa case is the most advanced, but the pattern of embedded Huawei presence repeats across the continent. In Ghana, Huawei’s country director met President John Mahama in October 2025 to pledge deeper cooperation in cloud computing, AI, and skills training, building on a two-decade presence that includes over 300 local employees and more than $100 million in ICT infrastructure investment.

In Ethiopia, Huawei partners with Ethio Telecom on 4G and 5G capacity upgrades. In Algeria, it operates a handset manufacturing facility serving local and regional markets. In Kenya, it has built backbone infrastructure since 1998, and in Nigeria, it supplies core network infrastructure to the country’s largest telecoms operators.

Across all these markets, Huawei’s position is not that of an equipment vendor competing on price — it is that of an embedded infrastructure partner with deep institutional relationships, local staff, local training centres, and years of accumulated switching costs working in its favour.

No African government has banned Huawei equipment, and South Africa and Brazil both declined US pressure to do so in 2022, citing economic pragmatism.

The absence of a credible, equally affordable Western alternative is the central fact of this market. Ericsson and Nokia are technically competitive, but they lack Huawei’s financing packages, its local training commitments, and the decade-deep relationship capital that makes switching not just expensive but genuinely disruptive.

The technical standardisation risk

A table comparing the “Ecosystem Lock-in” of different standards

| Feature | Chinese Standard (e.g., Huawei/ZTE) | Western Standard (e.g., Ericsson/Nokia) |

| Financing | Turnkey (Vendor + State Bank loan) | Market-based / Private Equity |

| Interoperability | Higher within “Digital Silk Road” apps | Global Open RAN standards |

| Data Residency | Often routed/managed via partner hubs | Strict GDPR/Local compliance focus |

The debate about Huawei in Africa has focused primarily on surveillance and data access, and those concerns are legitimate. But there is a second, less visible risk that deserves equal attention: technical standardisation.

When a country builds its 5G network on Huawei architecture, it does not merely acquire a telecommunications system — it adopts a technical standard, a specific set of protocols, interfaces, and specifications that determine what other equipment can connect to that network, and what cannot.

Power grids, smart city systems, industrial IoT networks, and payment infrastructure built on Chinese technical standards use specifications designed to interface with Chinese hardware and software, which means that Western alternatives may be technically incompatible or prohibitively expensive to retrofit into an established ecosystem.

Huawei’s Open RAN architecture, for example, uses proprietary elements that diverge from Western Open RAN specifications in ways that matter at deployment scale. Data encryption standards adopted in Chinese smart city deployments do not always interface cleanly with EU GDPR-compliant data management systems.

This is not a conspiracy or a deliberate trap — it is the normal logic of platform competition, the same strategy the United States pursued with GPS, SWIFT, and internet protocol standards.

But for African governments making infrastructure decisions now, the implication is consequential: the technical choices made in the next five years will constrain the choices available in the next twenty.

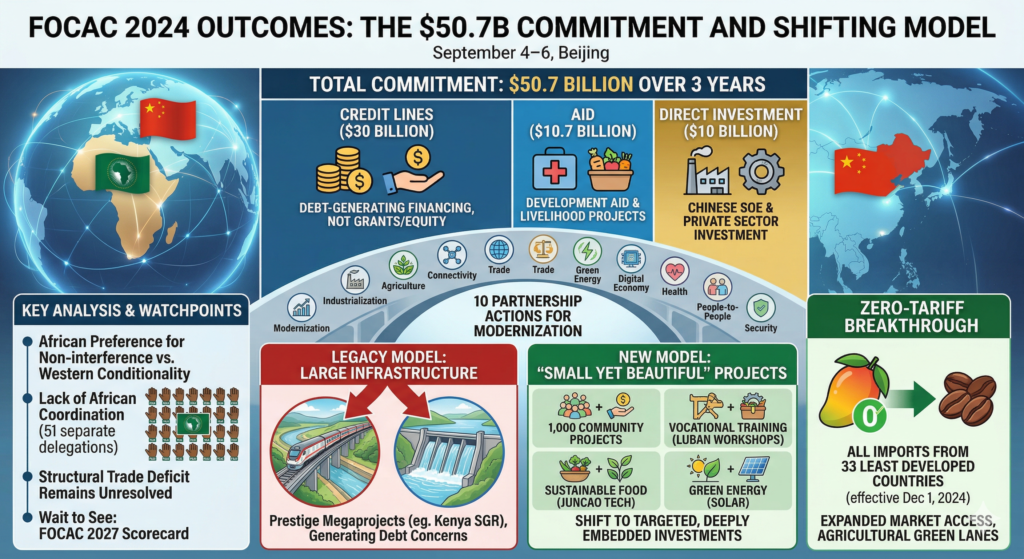

FOCAC 2024: What China Actually Committed To

The 9th Forum on China-Africa Cooperation was held in Beijing from September 4–6, 2024, and by any measure it was a significant diplomatic event — 51 African heads of state attended, more than typically appear at the UN General Assembly, a fact that is itself a geopolitical signal about where African governments believe consequential partnerships are being made. China pledged $50.7 billion over three years, a 25 percent increase over the $40 billion committed at the 2021 Dakar summit, and a figure that surprised many analysts who had expected China’s domestic economic slowdown to dampen its African ambitions.

Breaking down the $50.7 billion

The composition of that commitment matters as much as the headline number. Of the $50.7 billion, $10 billion is designated as direct investment, $10.7 billion as aid, and $30 billion as credit lines — meaning the largest single component is debt-generating financing rather than grants or equity.

Whether those credit lines accelerate African development or deepen financial dependency will depend on which countries receive them, on what terms, and in which sectors, none of which was specified in the summit communiqué with the precision that African finance ministers would need to make informed assessments.

The ten partnership actions

Xi Jinping announced ten partnership actions spanning modernisation support, industrialisation, agricultural development, infrastructure connectivity, expanded trade access, green development, digital economy cooperation, people-to-people exchange, health cooperation, and peace and security.

The breadth of these commitments reflects China’s ambition to position FOCAC as a comprehensive development partnership rather than a transactional minerals-for-infrastructure exchange — though the gap between the ambition of the framework and the specificity of the implementation plans remains significant.

The zero-tariff breakthrough

The commitment with the most immediate and practical impact was the zero-tariff announcement. From December 1, 2024, China extended zero-tariff treatment to all least developed countries with diplomatic ties — covering 33 African nations and eliminating barriers on 100 percent of their product categories.

Combined with the “green lane” fast-track customs arrangements for African agricultural produce, this creates a genuinely meaningful market access pathway for African exporters into a consumer market of 1.4 billion people — the kind of structural opening that Western development programmes have rarely been able to offer.

The soft power dimension

Beyond the financial commitments, FOCAC 2024 was notable for what it signalled about China’s strategic self-positioning. The summit’s theme was “Joining Hands to Advance Modernization,” and China used the platform explicitly to promote its own development path as a model rather than simply as a financing option.

The FOCAC Beijing Action Plan included commitments to share “governance experiences” — a phrase that, in Chinese policy language, encompasses state capitalism, infrastructure-led development, and what Xi Jinping calls “whole-process democracy.” This is not incidental framing.

It is soft power encoded in an economic document, and it represents a significant escalation beyond the passive “non-interference” posture that characterised earlier phases of China’s Africa engagement.

What FOCAC 2024 did not resolve

A clear-eyed assessment of the summit must also note what it left unaddressed. The structural trade deficit remains unchanged. Local labour content requirements in Chinese projects are still contested in virtually every major partnership country.

The terms of mineral concession agreements were not subject to the kind of systematic renegotiation that several African governments had sought. And critically, African countries arrived in Beijing as 53 separate delegations rather than a coordinated bloc — a fragmentation that significantly constrained their collective bargaining power and that China, which prefers bilateral relationships over multilateral African coordination, has no incentive to help resolve.

Agricultural Technology and the Rural Soft Power Play

China is currently the largest importer of African agricultural goods, and that trade relationship is being transformed by technology in ways that receive almost no coverage in Western strategic analysis — yet constitute one of Beijing’s most effective and least-discussed soft power instruments on the continent.

Where Western development programmes have historically approached African agriculture through the lens of governance reform and institutional capacity, China’s agri-tech model arrives with drones, market access platforms, and practical tools that operate at the farm level rather than the ministry level.

The political implications of that contrast are not subtle.

From Juncao to agri-tech at scale

The most visible element of China’s agricultural engagement is Juncao technology — an innovation using fungus cultivation on grass straw to produce mushrooms and animal feed in areas with poor soil quality, which China has transferred to over 100 countries including Ethiopia, Rwanda, and Zimbabwe.

It is practical, inexpensive, and genuinely useful, the kind of technology transfer that builds goodwill at the community level rather than through government-to-government communiqués. But Juncao is the surface layer of something considerably more significant.

Chinese companies are now deploying agricultural drones for crop spraying across multiple African markets, reducing pesticide costs and improving yields for smallholder farmers who previously could not afford professional crop protection services.

Alibaba and its agricultural subsidiaries are piloting e-commerce platforms designed to allow rural African farmers to sell directly into Chinese consumer markets — a model that, if it scales, would represent a genuine structural change in how African agricultural producers access global demand, bypassing the commodity traders and export intermediaries that have historically captured much of the value in African agricultural supply chains.

Green lanes and market access

China has also introduced “green lane” fast-track customs arrangements for African agricultural produce entering China, reducing clearance times and spoilage losses for perishable goods. Combined with the zero-tariff FOCAC commitment, these arrangements create a plausible — if not yet fully realised — pathway for African agricultural exports into a market of 1.4 billion increasingly middle-class consumers.

That pathway stands in contrast to Western agricultural development programmes, which have invested heavily in improving African production capacity without offering comparable access to high-value consumer markets.

A necessary caveat

Alibaba’s rural e-commerce ambitions in Africa have repeatedly outpaced delivery on the ground. The platforms exist in pilot form, and the vision is compelling, but they do not yet operate at transformative scale in any African market. The potential is real; the current reality is more modest. Any analysis that presents the agri-tech soft power play as already accomplished overstates a story that is still in its early chapters.

A diagram illustrating ‘Ecosystem Lock-in,’ showing how Chinese hardware (Huawei) and software (Alipay/WeChat) create a unified technical standard that contrasts with Western Open RAN models.

Chinese Fintech in Africa: WeChat Pay, Alipay, and the Post-Dollar Trend

The story of Chinese fintech in Africa is frequently mischaracterised as a story of platform conquest — WeChat Pay and Alipay expanding into African consumer markets and displacing local alternatives. That is not what is happening.

The more accurate and more interesting story is about model export, structural influence, and a quiet but consequential shift in the financial architecture that underlies China-Africa trade.

The scale of the Chinese platforms — and their limits in Africa

WeChat Pay and Alipay together processed over $80 trillion in transactions in 2024, and Alipay’s global monthly active users hit 1.4 billion in 2025. Their architecture — QR codes, super-apps that bundle payments with social features, commerce, and financial services — was built on a powerful insight that mobile-first, cash-heavy populations could leapfrog card infrastructure entirely, an insight perfectly calibrated for the African market.

Yet neither platform has achieved mass consumer penetration in Africa directly. Their primary presence in African markets today serves Chinese business travellers, diaspora communities, and cross-border merchants — a significant footprint, but not the retail dominance that the platform scale might suggest.

How Africa’s fintech learned from China

The deeper influence is architectural rather than branded. M-Pesa’s agent-banking model, OPay’s super-app strategy, and Flutterwave’s API-first payment infrastructure all reflect lessons absorbed from the Chinese fintech playbook, each adapted to African regulatory environments and infrastructure constraints.

The Chinese fintech revolution did not conquer Africa directly — it shaped the designers and entrepreneurs who built Africa’s own financial platforms, creating an intellectual lineage that connects Alibaba’s rural e-commerce innovations in Zhejiang to the mobile money networks serving smallholder farmers in western Kenya.

Currency swaps and the de-dollarisation agenda

The more geopolitically significant development, however, is not in consumer payments but in cross-border trade finance. In December 2024, China and Nigeria renewed a 15 billion yuan ($2 billion) currency swap agreement that allows businesses to trade directly in yuan and naira without routing through the US dollar system.

Similar arrangements exist with Egypt, South Africa, and Kenya, and together they represent a quiet but consequential step in de-dollarising trade corridors between China and Africa — reducing exposure to dollar exchange rate volatility and, for countries that have faced or fear US financial pressure, creating a parallel settlement architecture that does not run through American-controlled financial infrastructure.

The digital yuan and what BRICS+ means for financial architecture

China’s digital yuan — the e-CNY — is the story to watch as this trend develops. The PBOC has been piloting e-CNY cross-border transactions since 2021, and by April 2025 the currency was accepted in ten overseas jurisdictions. If e-CNY becomes a standard settlement currency for China-Africa trade, it would represent a structural shift in the continent’s financial architecture with implications well beyond bilateral commerce.

That shift becomes more credible when set against the BRICS+ expansion: Egypt and Ethiopia both joined BRICS in January 2024, bringing two of Africa’s most significant economies into a framework that is actively developing yuan-denominated and local-currency trade settlement alternatives to the dollar system. By 2026, the question is no longer whether this post-dollar architecture will exist — it already does, in embryonic form — but how quickly and under what circumstances African governments will choose to use it.

BRI Debt Traps: Myth, Reality, and the Mineral Collateral Question

“Debt-trap diplomacy” is the most contested frame in China-Africa analysis, and few topics generate more heat and less analytical clarity. The term was coined in 2017 by Indian analyst Brahma Chellaney and rapidly became the dominant Western frame for interpreting the Belt and Road Initiative.

A frame that is simultaneously useful as a political shorthand and misleading as a description of how Chinese money actually moves in Africa. Getting this debate right matters, because both the oversimplified accusation and the reflexive denial obscure what is genuinely concerning about Chinese lending patterns on the continent.

Where the myth case is strongest

Multiple independent studies have concluded that the BRI debt trap does not exist as a deliberate, systematic Chinese strategy. The Centre for Global Development, Chatham House, and Johns Hopkins’ China Africa Research Initiative have all reached essentially the same conclusion: China has not consistently seized assets when borrowers defaulted, has repeatedly restructured debts and extended repayment timelines, and has in some cases forgiven debts entirely.

The Sri Lanka Hambantota port remains the case most frequently cited as evidence of a deliberate trap, yet it involved a specific lease arrangement driven by Sri Lankan fiscal distress rather than a programmatic pattern of Chinese asset seizure.

Moreover, the framing of Chinese lending as uniquely predatory ignores a long historical precedent: Western private banks used resource-backed lending in Latin America and Africa for decades before China did, and the structural logic of securing loans against commodity off-take agreements is not a Chinese invention.

Where real debt concerns exist

Dismissing the debt trap narrative entirely, however, misses something real and important. A 2025 Lowy Institute study found that in 54 of 120 developing countries, debt service payments to China now exceed the combined repayments owed to Paris Club countries — a finding that reflects the sheer scale of Chinese lending rather than deliberate entrapment, but that nonetheless represents a genuine constraint on African fiscal policy.

Roughly 20 percent of Africa’s external debt is owed to Chinese institutions, and in Zambia, Angola, and Ethiopia, that share is substantially higher, limiting the fiscal space those governments have to respond to economic shocks or to fund domestic development priorities.

The mineral collateral question — the honest framing

The most accurate and analytically useful framing is not “debt trap” but resource-backed lending — a model in which many Chinese loans are tied, implicitly or explicitly, to commodity off-take agreements that give Chinese companies preferential access to African mineral production in exchange for the financing.

Oil from Angola secures infrastructure loans; cobalt and copper access in the DRC is linked to processing investment; lithium concessions in Zimbabwe underpin Chinese industrial financing. This is not asset seizure, and it is not unique to China.

But it does mean that Chinese capital is not neutral — it is channelled toward securing supply chains for China’s industrial economy, and the terms of those arrangements, which are frequently opaque and rarely subject to parliamentary scrutiny in the borrowing country, deserve far more attention than the debt trap debate has generated.

China’s State Mining Companies in the DRC

The Democratic Republic of the Congo is the single most important country in the world for the global clean energy transition, and China’s position within it is dominant.

The DRC holds approximately 70 percent of global cobalt reserves and ranks among the top three copper producers worldwide, making it the indispensable geography for the EV battery supply chains that underpin China’s green industrial strategy. For a country that manufactures roughly 75 percent of global EV batteries, the DRC is not a peripheral investment opportunity — it is existential.

The key players and their positions

China Molybdenum (CMOC) operates the Tenke Fungurume copper-cobalt mine — one of the world’s largest — and the Kisanfu cobalt project. In 2023, CMOC surpassed Glencore to become the world’s largest cobalt producer, a milestone that placed a Chinese state-linked company at the centre of a supply chain that every major automaker in the world depends upon.

Zijin Mining holds a major position in the Kamoa-Kakula copper complex, the world’s highest-grade large copper deposit. Sinomine Resource Group is active in lithium and mineral processing, and MMG, a Minmetals subsidiary, operates the Kinsevere copper mine.

How the operational model works

Chinese mining companies in the DRC follow a recognisable operational pattern that reflects both commercial logic and strategic design. Entry typically comes through acquisition of existing projects rather than greenfield exploration, which reduces risk and accelerates production timelines. Formal partnerships with the DRC state mining company Gécamines provide local institutional legitimacy.

Chinese construction contractors handle infrastructure work, channelling capital spending through Chinese-controlled firms even when the extraction happens on Congolese soil. And financing is often structured to route processing and shipping through Chinese-controlled intermediaries, ensuring that value capture extends well beyond the mine gate.

Some arrangements go further, tying mineral access directly to Chinese-built road and energy infrastructure in the “minerals-for-infrastructure” swap model — a variant of the Angola model applied to hard rock mining — which creates infrastructure that the DRC genuinely needs but that simultaneously deepens the structural dependency of the relationship.

Local content tensions and what they reveal

Local content has been the persistent friction point in Chinese mining operations across the DRC, and it is a friction point that matters beyond its immediate economic impact.

DRC civil society organisations have documented cases of Chinese companies employing Chinese labour in skilled roles rather than training and hiring Congolese workers, environmental compliance failures including sulphuric acid spills and water contamination incidents, and community benefit arrangements that fall well short of what was promised in project agreements.

Western mining majors have equally poor records in the DRC historically, which makes the whataboutism argument technically valid and the underlying standard equally inadequate. What these tensions reveal, beyond their immediate human cost, is the distance between the “mutual development” narrative that Beijing uses to frame its engagement and the operational reality on the ground.

Smart Power vs. Western Conditionality — and the Gulf Rivalry

Understanding why African governments consistently prefer the FOCAC model to Western partnership frameworks requires taking seriously a critique of Western development finance that African leaders have been making for decades and that Western analysts have been slow to internalise.

Chinese engagement does not come with the conditions that have historically characterised Western aid and lending — macroeconomic reform requirements, privatisation mandates, anti-corruption benchmarks, democratic governance standards, environmental safeguards — conditions that reflect genuine lessons about development effectiveness but that have also been applied selectively, inconsistently, and in ways that have sometimes advanced Western commercial interests more visibly than African development priorities.

Why the FOCAC model keeps winning

Chinese financing, by contrast, operates under the official “non-interference” principle — faster, less paternalistic, and more compatible with African governments’ policy autonomy. The evidence from FOCAC 2024 is instructive in this regard: the summit attracted more African heads of state than the UN General Assembly, a signal not of Chinese coercion but of genuine African preference for a partnership model that delivers specific financial commitments without requiring governments to defend their domestic policies to external supervisors.

Whether that preference is wise in the long run is a separate question. It is the political reality shaping decisions today, and any analysis that dismisses it as naivety or corruption misunderstands why it persists across governments of very different political characters.

Where non-interference becomes active promotion

China’s “smart power” becomes most controversial — and most consequential — where it moves from passive non-interference to active promotion of an alternative governance model. The FOCAC Beijing Action Plan’s commitment to share “governance experiences” is not rhetorical boilerplate: it signals a deliberate effort to present state capitalism, surveillance-enabled social management, and development-first governance as legitimate alternatives to liberal democratic frameworks, particularly attractive to governments that experience Western democracy promotion as a threat to their political stability rather than a path to development.

This is a genuine ideological competition, not merely a commercial one, and its implications extend well beyond any individual infrastructure project.

An honest assessment of both models

Neither model, examined honestly, has a strong track record. Western conditionality has not transformed governance in Africa, has often entrenched dependency and resentment, and has sometimes served as a mechanism for advancing Western commercial interests in the name of development.

Chinese non-conditionality has financed real infrastructure, delivered real educational and technical benefits, and built genuine goodwill — while simultaneously enabling authoritarian consolidation in some partner states and concentrating resource extraction in Chinese hands.

African civil society organisations are correct to argue that the binary choice between these two external models is a false one, and that African-owned development frameworks deserve far more analytical attention than they currently receive in the geopolitical literature on China-Africa relations.

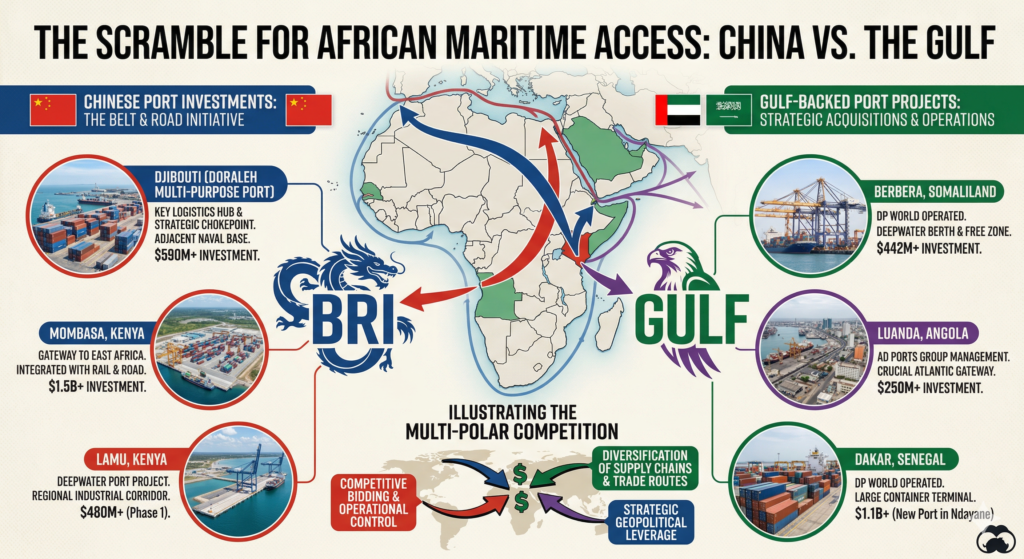

A comparative graphic showing Chinese port investments (e.g., Djibouti) alongside Gulf-backed port projects (e.g., DP World in Berbera and Luanda), illustrating the multi-polar competition for maritime access.

The Gulf rivalry and Africa’s multi-alignment strategy

The traditional “China vs. the West” binary is increasingly obsolete. What both Beijing and Brussels have failed to fully absorb is the disruptive entrance of Gulf capital, which is fundamentally reshaping the negotiating landscape in 2026. No longer restricted to oil and real estate, the UAE and Saudi Arabia have emerged as aggressive, fast-moving competitors for the very assets China once assumed were its own.

The Battle for Ports and Pits

The rivalry is most visible in maritime logistics and “green” minerals. Dubai’s DP World and Abu Dhabi’s AD Ports Group are now in direct, head-to-head competition with Chinese state giants like COSCO and China Merchants. While China has anchored its presence in Djibouti and Mombasa, Gulf players have secured or are developing strategic footholds in Dakar, Berbera, Luanda, and Pointe-Noire.

In the mining sector, the shift is even more stark. The UAE’s International Resources Holding (IRH) and Saudi Arabia’s Ma’aden are no longer just passive investors; they are outbidding Chinese state-owned enterprises (SOEs) for critical mineral rights. A prime example is Zambia’s copper sector, where IRH has utilized its massive liquidity to challenge China’s historical dominance, offering terms that prioritize faster capital injection and localized processing.

Multi-Alignment as a Power Move

African governments are not merely “caught in the middle”—they are exploiting this multi-polar competition with newfound strategic sophistication. By positioning Gulf capital as a viable “third way,” leaders in Lusaka, Nairobi, and Cairo are leveraging the following advantages:

- Speed and Agility: Unlike the G7’s PGII, which is often bogged down by domestic political cycles and private equity risk-aversion, Gulf sovereign wealth funds move with a velocity that rivals—and sometimes exceeds—Chinese state banks.

- Negotiating Leverage: African negotiators now use UAE investment term sheets as a blunt instrument to squeeze better concessions from Chinese counterparts, particularly regarding local labor quotas and debt sustainability.

- Diversified Dependency: By spreading strategic assets across Chinese, Western, and Gulf interests, African states are effectively “multi-aligning,” ensuring that no single foreign power holds a monopoly over their national infrastructure or digital future.

This dynamic is a clear signal that the era of uncontested Chinese access is over. In 2026, the continent is no longer a passive recipient of foreign strategy; it is a competitive marketplace where the highest bidder must now offer more than just a check—they must offer a partnership that respects African agency.

African Universities and the Chinese Tech Scholarship Pipeline

China’s educational engagement with Africa is one of the most underanalysed dimensions of the relationship, and in the long run it may prove to be the most durable — precisely because its effects operate through human capital formation rather than physical infrastructure, and human capital is considerably harder to renegotiate than a mining concession.

The strategic logic of 50,000 scholarships

FOCAC 2024 committed to 50,000 Chinese government scholarships for African students over the next three years, reinstating a level that was cut to 10,000 at the pandemic-era 2021 summit and signalling a recommitment to educational soft power as a strategic instrument.

The scholarships cover undergraduate, postgraduate, and doctoral study, with a strong emphasis on STEM fields — engineering, telecommunications, computer science, agricultural science, and biomedical research — that is not accidental.

African scholars trained at Chinese universities learn Chinese-standard technical systems, graduate familiar with Huawei equipment and CITIC financing structures and ZTE network architecture, and return home as engineers, officials, and executives who are naturally more comfortable advocating for Chinese solutions in their professional environments.

This is soft power operating through human capital formation, and it is a long-horizon investment whose effects will be felt most strongly in the 2030s and 2040s, when today’s scholarship cohorts occupy senior positions in African industry, government, and academia.

It receives far less analytical attention than Huawei’s hardware deployments or BRI loan terms, despite being potentially more consequential for the long-term character of the China-Africa relationship.

Luban Workshops and vocational training

The “Luban Workshop” programme extends the educational model beyond university scholarship to vocational training, establishing Chinese-curriculum technical schools across Africa that focus on practical skills aligned with Chinese industrial investment.

By 2024, Luban Workshops were operating in over 20 African countries, training mechanics, electricians, and IT technicians in standards that integrate naturally with Chinese-built infrastructure — so that the Chinese-built railway also generates demand for Chinese-trained maintenance staff, and the Chinese-built data centre creates a professional ecosystem calibrated to Chinese technical systems.

Confucius Institutes, digital learning, and the African response

The Confucius Institute network runs over 60 campuses across Africa, extending Chinese language and cultural programming into African universities and funding departments that would otherwise lack resources. Several governments, including Kenya, have reviewed their Confucius Institute arrangements over academic freedom concerns, and those concerns are legitimate.

Most governments have maintained the partnerships, however, because the funding is real and alternatives are scarce — a pragmatic calculation that illustrates a broader pattern in the China-Africa relationship.

China’s digital education push through platforms like XuetangX scales this model further, distributing Chinese technical curriculum to African learners without requiring physical mobility to China.

African scholars who have studied in Chinese institutions often offer a more nuanced picture than Western critics present — many describe Chinese technical education as more practically oriented and less condescending about African capability than some Western-funded programmes. The soft power pipeline works partly because it delivers genuine educational value, and any analysis that reduces it to pure manipulation misses the complexity of why it is received as well as it is.

Surveillance Technology Exports: Smart Cities, AI Cameras, and Democratic Risk

The most politically charged dimension of China-Africa digital infrastructure is the export of AI-powered surveillance technology packaged as “Safe City” and “Smart City” programmes — a framing that is accurate enough to be credible and misleading enough to be dangerous.

Across major African cities from Nairobi to Lusaka to Abuja to Accra, governments are deploying networked camera systems, facial recognition infrastructure, and command-and-control centres built and often operated by Chinese firms, using Chinese bank financing that covers the full cost of deployment. A 2023 Censys analysis identified over 46,000 commercially deployed devices from Huawei, ZTE, Hikvision, and Dahua in Kenya, Zambia, South Africa, and Mauritius alone — a number that has grown substantially since.

Nigeria: Africa’s largest buyer

Nigeria has emerged as the continent’s largest buyer of Chinese surveillance technology, with the National Public Security Communication System costing $470 million — 85 percent financed by China Eximbank, with ZTE Corporation and Hikvision as the primary contractors.

The project built nationwide surveillance and video conferencing infrastructure for the Nigerian Police Force, and Lagos State separately deployed approximately 13,000 CCTV cameras under its Safe City initiative before expanding again with 10,000 high-definition facial recognition-enabled cameras.

Oyo State added its own Huawei and Hikvision-powered network independently. Taken together, these deployments make Nigeria a case study in how Chinese surveillance infrastructure scales from a single federal contract into a layered national ecosystem through sequential state-level procurement decisions.

Ghana, Morocco, Zambia, and the financing model

Ghana, Morocco, and Zambia have each reportedly spent over $250 million on Chinese surveillance technology packages, financed through Chinese bank loans covering 85 to 100 percent of costs — a financing model that makes the technology effectively free at the point of procurement and creates deep integration between Chinese state-linked companies and the surveillance architectures of African governments, with Chinese technical teams often operating command centres during setup and maintaining the systems long afterward.

Digital Sovereignty in Africa: Data, Governance, and the Algorithmic Risk

The most politically charged dimension of China-Africa digital infrastructure isn’t just the hardware; it’s the question of who owns the data that hardware generates. In Zimbabwe, the government’s partnership with CloudWalk Technology attracted international scrutiny when reports surfaced that the deal included provisions for training AI algorithms on African faces.

This highlights a growing crisis of digital sovereignty. African facial recognition datasets are a goldmine for Chinese AI firms looking to refine global products. Without robust local data-protection laws, African biometric data effectively becomes a raw material—extracted, processed in China, and sold back as a finished security product.

In Ethiopia, ZTE and Huawei provide the backbone of government surveillance capability. Ghana’s Accra Intelligent Traffic Management System was controversially awarded to Huawei after a procurement dispute, with Human Rights Watch raising concerns about its potential use against political opposition.

Why governments buy — and what they are actually buying

Three factors explain African government demand for Chinese surveillance technology, and they are all legitimate:

- The cost is significantly lower than Western alternatives,

- The financing requires no human rights impact assessments or civil liberties preconditions,

- And the stated need is real.

Urban crime, traffic management, and counter-terrorism are genuine challenges in rapidly urbanising African cities, and the technology demonstrably helps address them. A surveillance camera that reduces road fatalities and a surveillance camera that tracks political opponents are the same piece of hardware — the difference lies entirely in how the system is governed, who has access to the footage, under what legal authority, and with what oversight mechanisms.

That governance layer is precisely what is missing. In Uganda, Huawei’s camera network was reportedly used to monitor opposition candidate Bobi Wine. In Zimbabwe, surveillance technology has been linked to the targeting of journalist Hopewell Chin’ono and opposition leader Jacob Ngarivhume.

The governance gap — the absence of continent-wide data protection standards, judicial oversight requirements, or transparency obligations about data-sharing with Chinese government entities — is what makes the hardware genuinely dangerous, regardless of its origin.

The problem is not Chinese cameras. The problem is African governments deploying powerful surveillance capabilities without the legal frameworks and democratic accountability structures that would prevent those capabilities from being turned against the people they are supposed to protect.

The 2026 Inflection Point: Three Simultaneous Pressures

China-Africa technology trade sits at a genuine inflection point in 2026, shaped by three simultaneous pressures that did not exist in the same combination five years ago and that are collectively accelerating the pace and depth of Chinese engagement in ways that require careful attention from anyone trying to understand where the relationship is heading.

Pressure 1: US tariff escalation and the search for alternative markets

American tariffs on Chinese goods expanded significantly in 2024 and 2025, and their effect on Chinese export strategy has been rapid and substantial. Chinese exports to Africa surged 24.7 percent in the first eight months of 2025, with solar panels, electronics, vehicles, and machinery flowing south in volumes that reflect the systematic redirection of export capacity away from the US market.

Africa — with 1.4 billion people, an urbanising middle class, and still-developing consumer markets — is the clearest candidate for absorbing that redirected capacity. This is not altruistic development financing. It is economic redirection in response to external pressure, and it will intensify as the US-China trade conflict deepens.

Pressure 2: The clean energy transition and the minerals scramble

The global scramble for EV battery minerals is bringing Africa’s geological endowments into the sharpest strategic focus they have ever attracted, and it is doing so at a moment when China already controls dominant positions in the processing and manufacturing stages of the supply chain.

The DRC, Zambia, Zimbabwe, and South Africa hold reserves that every major economy needs, and the downstream shift pressure discussed earlier in this guide reflects African governments’ growing awareness that their leverage in this moment is real and time-limited — real because the world needs their minerals, and time-limited because the window for demanding better terms narrows as Chinese supply chain integration deepens.

FOCAC 2024 offered little on this front. The 2027 summit will be the genuine test of whether China will support African mineral processing or continue to resist it.

Pressure 3: Western and Gulf competition, and what it means for African agency

The G7’s PGII and the EU’s Global Gateway are attempting to offer credible alternatives to Chinese financing and technology, and the Lobito Corridor railway is the flagship demonstration project. But both initiatives continue to face the structural problem that private Western capital demands risk-adjusted returns that African infrastructure projects rarely offer without subsidy, while Chinese state capital can tolerate strategic patience.

What is changing the equation more significantly is the Gulf’s role — newer, faster-moving, and in some respects more competitive with Chinese terms than Western alternatives have managed to be.

The combination of Chinese, Western, and Gulf capital competing for African strategic relationships is creating a genuine multi-alignment opportunity for African governments, and FOCAC 2024’s explicit integration of African Continental Free Trade Area alignment into Chinese infrastructure commitments suggests Beijing is aware that the era of relatively unchallenged access to African strategic assets is giving way to something more contested and more complex.

How African governments leverage that complexity — individually through bilateral deal-making, and collectively through continental coordination — will determine whether the inflection point of 2026 produces better terms for Africa or simply more sophisticated forms of the same dependency.

What to Watch — and What It All Means

China’s footprint in Africa is neither the developmental salvation Beijing claims nor the neo-colonial conspiracy its most strident critics describe.

It is something considerably more complicated than either characterisation allows: a relationship built on genuine complementarity between Chinese capital and manufacturing capacity on one side, and African resource endowments and infrastructure deficits on the other, but one that is shot through with asymmetries of power, information, and negotiating capacity that consistently advantage Beijing and that African institutions are only beginning to develop the collective capacity to address.

Signs of a maturing relationship

What makes this moment meaningfully different from any previous phase of the relationship is that African governments are increasingly aware of those asymmetries and are attempting, with growing sophistication, to close them. The FOCAC 2024 zero-tariff commitments represent genuine movement on market access. The wave of mineral export bans signals real determination to capture downstream value.

The AU’s emerging data governance framework points toward continental standards that could constrain the most problematic applications of surveillance technology. The use of Gulf capital as a negotiating lever against Chinese terms reflects strategic awareness rather than improvisation. Taken together, these developments suggest that Africa’s side of the China-Africa relationship is maturing — not rapidly enough to correct the fundamental asymmetries in the near term, but directionally in a way that is significant.

The structural tensions that will define the next decade

Several unresolved tensions will define the trajectory of the relationship through the 2030s. The downstream industrialisation question — whether China will genuinely support African mineral processing or continue to resist it in defence of its own supply chain interests — is the single most important test of whether FOCAC’s “industrialisation” commitments are substantive or rhetorical.

The technical standardisation battle, playing out quietly in 5G spectrum allocation decisions and smart city procurement choices across the continent, will determine whose hardware, software, and governance models are embedded in African infrastructure in 2040 in largely irreversible ways.

And the post-dollar financial architecture, being assembled piece by piece through currency swaps, BRICS+ expansion, and e-CNY pilots, will reshape the financial plumbing of African trade in ways whose full implications are not yet visible.

Five indicators to watch through 2027

FOCAC 2024–2027 implementation scorecard.

The $50.7 billion commitment only matters if it materialises, and historical implementation rates have run below 50 percent for investment commitments. Tracking actual disbursements against pledges — by sector and by country — is the most direct measure of whether FOCAC 2024 represents a genuine shift in Chinese engagement or a well-managed diplomatic performance.

DRC mineral concession renegotiations

The Congolese government’s ongoing review of Chinese mining agreements, pushing for better terms on local processing and revenue sharing, will shape the Belt and Road Initiative Africa minerals dynamic for the next decade. Whether Kinshasa succeeds in capturing substantially more value from Chinese-operated mines is the most consequential single bilateral negotiation on the continent.

5G spectrum allocation in Nigeria and Ethiopia

Both countries face 5G licensing decisions that will function as a bellwether for the continent’s telecommunications architecture — and for whether any African government is prepared to pay the price of choosing Western alternatives over Huawei in a market where Huawei’s proposition remains significantly more competitive.

e-CNY Africa pilots

Any formal announcement of e-CNY use in China-Africa trade settlement — even a bilateral pilot with a single African central bank — would represent a structural shift in China-Africa digital infrastructure whose implications would extend well beyond the countries directly involved.

Surveillance governance legislation

The African Union’s model data protection framework will be the test of whether African governments adopt meaningful oversight requirements for surveillance technology or allow the governance gap to persist indefinitely.

The technology is already embedded across major African cities. Whether it serves development or repression depends almost entirely on the legal and institutional frameworks that are built around it — and that choice belongs to African governments, not to Beijing, Brussels, or Washington.

The End of Paternalism and the Birth of a Hard Bargain

China’s presence in Africa is neither a charitable gift nor a colonial conspiracy; it is a clinical, state-backed pursuit of industrial survival. In 2026, we have moved past the era of “non-interference” into an era of deep integration. From the lithium mines of Zimbabwe to the 5G cores of Lagos, African infrastructure is becoming a physical extension of the Chinese industrial machine.

However, the “passive Africa” narrative is dead. The 2025–2026 inflection point has revealed a continent that is finally learning to play the great powers against one another. By leveraging Gulf capital to squeeze Chinese lenders and using raw mineral bans to force Beijing’s hand on industrialization, African nations are moving from being the chessboard to being the players.

The Looming Decades

The real danger for Africa in the coming decade isn’t a “debt trap”—it’s a “standardization trap.” If African governments continue to trade long-term digital sovereignty for short-term infrastructure financing, they risk waking up in 2040 in a continent that is technically incompatible with the rest of the world and politically transparent to Beijing.

The Belt and Road Initiative, the Huawei backbone, and the e-CNY pilots are powerful tools for development, but they are dual-use. They can either be the rails upon which Africa rides toward its own industrial revolution, or the chains that bind its digital and economic future to a single patron.

The question is no longer what China wants from Africa. We know the answer: minerals, markets, and diplomatic loyalty. The only question that remains is whether African leaders have the stomach to demand a price that includes their own industrial independence. The window to set that price is closing..