South Africa, Kenya, Egypt, and Nigeria are pursuing four entirely different visions of what it means to lead the continent’s artificial intelligence future. Here is what the data actually shows — and who is likely to win on each dimension.

The AI Momentum Index: Africa 2025–2030

| Metric | Value | Context & Significance | Strategic Outlook |

| Market Valuation | $4.5B → $16.5B | 2025 baseline growing to 2030 projection. | Represents a 267% increase in economic contribution over five years. |

| Adoption Rate | 42.1% | Kenya’s generative AI usage (highest on the continent). | Indicates grassroots integration outpacing formal enterprise deployment. |

| Ecosystem Density | 120+ | Active AI-first startups in Lagos, Nigeria. | Positions Lagos as the primary engine for localized AI innovation. |

| Global Standing | 36th | South Africa’s rank in Stanford’s Global AI Vibrancy Index. | The only African nation currently in the top 40 globally for AI maturity. |

| Labor Impact | 230M | Projected digital jobs in Sub-Saharan Africa by 2030. | Highlights the critical need for AI-augmented skills in the workforce. |

As artificial intelligence moves from experiment to industrial infrastructure, four African countries are making distinct bets on how to win.

South Africa has spent a decade building the continent’s deepest technical foundation.

Nigeria has assembled Africa’s largest startup ecosystem. It is betting that sheer market scale will translate into economic dominance.

Egypt has pursued a sovereign AI strategy — investing in a national large language model and positioning itself as the bridge between African and Middle Eastern markets.

Kenya, meanwhile, has achieved something none of the others have: a grassroots AI adoption rate that rivals the world’s most digitally advanced economies.

Which country’s version of leadership matters most?

The question of who leads Africa in AI by 2030 cannot be answered with a single metric. Leadership looks different depending on how you measure it — infrastructure, policy, startup density, economic impact, or daily AI usage. On each dimension, a different country is ahead.

“Africa’s AI movement has shifted from consumerism to foundational building. Startups are building language models that understand local context, while others are integrating the technology in hardware tools to improve efficiency, sovereignty, and innovation.”TechCabal, December 2025

Cinematic shot of a modern African tech hub, incorporating the Sandton data center.

The State of Play in 2026

Africa’s AI market was valued at approximately $4.51 billion in 2025. A compound annual growth rate of 27.42% is projected to carry it to $16.53 billion by 2030.

The continent currently captures just 2.5% of the global AI market — a figure that underscores how much of the race remains to be run. Yet within that constrained overall position, a small group of countries has separated itself sharply from the rest.

Nigeria, Kenya, South Africa, and Egypt together captured 83% of all AI startup investment in early 2025. They host the continent’s four largest data center clusters and more than 230 AI-specific startups. Between them, they have also drawn in the major cloud hyperscalers.

Microsoft Azure operates regions in South Africa. Google and AWS have local infrastructure in Nigeria. Egypt attracted Gulf capital through the G42-Benya Technologies partnership. The gap between these four and the rest of the continent is not narrowing — it is accelerating.

As of late 2025, only 16 African countries had launched national AI strategies. Notably, Nigeria — the continent’s most populous nation and its largest startup ecosystem — was still drafting its formal AI policy as of July 2025. That gap reveals how misaligned formal governance can be from on-the-ground innovation activity.

Pillar One: Infrastructure

The Hardware Gap

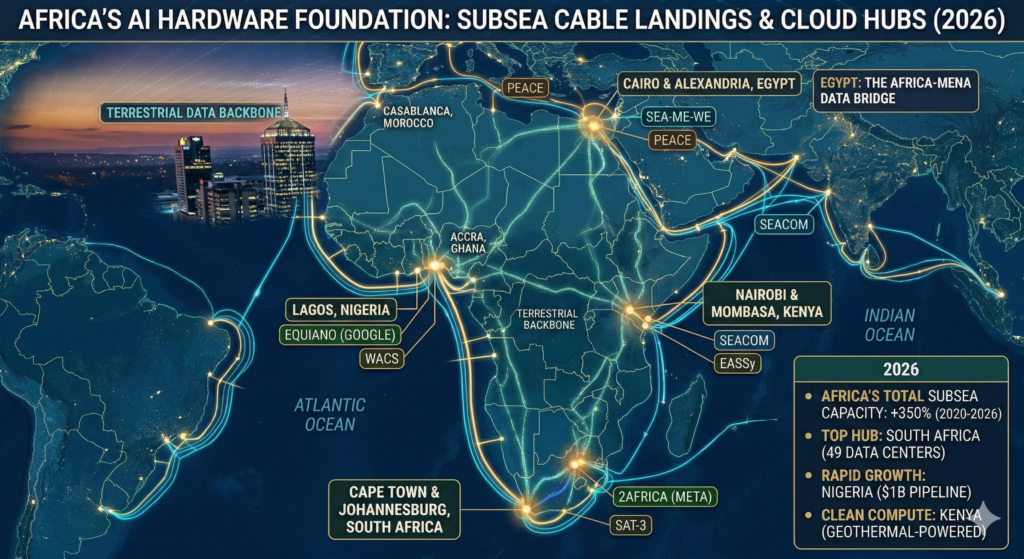

Infrastructure remains the defining bottleneck for African AI, and South Africa’s advantage here is not marginal — it is structural. South Africa hosts 49 data centers and controls roughly 70% of the continent’s total data center capacity. Furthermore, it operates Microsoft Azure hyperscale regions in both Johannesburg and Cape Town.

In 2025, Cassava Technologies deployed 3,000 NVIDIA GPUs across South Africa, creating Africa’s first network GPU-as-a-Service offering. South Africa is the only African country in Stanford University’s 2025 Global AI Vibrancy Tool. It ranks 36th globally — within the top 20% of all countries worldwide.

By contrast, Nigeria is mounting the continent’s most aggressive infrastructure expansion, despite a critical structural disadvantage. Its national grid has never exceeded 6 gigawatts for 230 million people. Compare that with South Africa’s 48 gigawatts for 63 million. Close to one billion dollars in AI-ready data center investment is currently arriving.

MTN’s Sifiso Dabengwa center in Ikeja is already operational. Airtel’s $120 million Nxtra hyperscale facility in Eko Atlantic was designed specifically for GPU workloads. Kasi Cloud’s planned 100-megawatt AI campus in Lekki is under development.

Nigeria’s data center market is projected to grow from roughly $300 million in 2025 to $800 million by 2031. But as one industry executive said at Hyperscalers Convergence Africa 2025: “Success requires two things: power and bravery.”

Egypt and the MENA corridor

Egypt holds a strong third position. It is one of Africa’s four major data center hubs. Its subsea cable geography is a key asset — several major cable systems land on its Mediterranean coast, giving it strong global connectivity.

A partnership between G42 and Benya Technologies began building localized AI compute capacity in 2022, and that investment has compounded since. Notably, Egypt’s AI diffusion rate of 13.4% by late 2025 was the highest among the Big Four.

This suggests its infrastructure is translating into real usage more effectively than Nigeria’s, despite Nigeria’s greater raw ambition.

Map of Africa showing the landing points of major subsea cables.

Kenya’s clean energy edge

Meanwhile, Kenya has carved a distinct niche through clean energy. Geothermal power provides the majority of Kenya’s electricity, giving it a structural cost advantage for running data centers sustainably. IXAfrica announced a 53-megawatt hyperscale facility expansion.

A partnership between the US Trade and Development Agency and Kenyan Semiconductor Technologies Limited is pursuing a semiconductor manufacturing facility in Nairobi. If delivered, this would make Kenya the first Sub-Saharan country with local chip manufacturing capacity.

Africa AI Infrastructure scorecard 2026

| Country | Readiness Score | Infrastructure Assets | Key Strategic Advantage | Primary Constraint |

| South Africa | 95/100 | 49 Data Centers | 70% of continental capacity; mature AWS/Azure hubs. | Low societal AI diffusion rates. |

| Egypt | 72/100 | 14 Data Centers | High 13.4% AI diffusion; elite subsea cable landing. | Centralized gov-led model. |

| Nigeria | 58/100 | 16 Data Centers | $1B incoming investment; aggressive cloud expansion. | Critical power grid stability. |

| Kenya | 54/100 | 18 Data Centers | Geothermal energy; sustainable compute niche. | Funding & compute scale. |

Pillar Two: Policy & Regulation

From aspiration to enforcement

By 2026, African AI governance has moved beyond strategy documents. Countries with active frameworks are beginning to enforce them. Consequently, the gap between nations with mature policy infrastructure and those without is becoming commercially significant — it now affects where investors choose to deploy capital.

Egypt leads the continent on formal government AI readiness. It has been ranked first in Africa on this metric in recent assessments. Specifically, its second-edition national AI strategy (2025–2030) focuses on healthcare, agriculture, and Arabic natural language processing.

The state directly funds AI research and provides tax incentives through its Technology Innovation Parks. Furthermore, it co-invests with the private sector at a scale no other African government matches. The unveiling of Karnak — Egypt’s national large language model — at the Ai Everything MEA summit in Cairo in February 2026 marked a turning point. Egypt declared its intention to own its AI infrastructure, not merely consume it.

Kenya’s National AI Strategy

Similarly, Kenya’s National AI Strategy, launched in March 2025, is among the continent’s most operationally detailed. It sets seven measurable outcomes and proposes a National AI Council. It also creates sector-specific Technical Working Groups and explicitly prioritizes indigenous model development.

Kenya ranks eighth in Africa on the Oxford Insights Government AI Readiness Index. Its strong data protection framework gives investors regulatory confidence.

Southern and West Africa

By contrast, South Africa follows a rights-based approach, aligning AI deployment with its existing Protection of Personal Information Act (POPIA). Its national AI policy was entering final approval stages in 2026, emphasizing ethical deployment and job preservation rather than pure growth.

This caution has real costs — it has slowed some AI deployment. However, it also builds the institutional trust that supports long-term foreign investment.

Nigeria presents a paradox. Its startup ecosystem is the continent’s most dynamic, yet it remained in the drafting phase for its national AI policy as of mid-2025.

The Nigeria AI Research Scheme (NAIRS) and the 3 Million Technical Talent (3MTT) initiative represent meaningful grassroots capacity building. Nevertheless, the absence of a formal regulatory framework creates uncertainty for large-scale enterprise and foreign investment.

National AI policy maturity scorecard

| Country | Maturity Score | Governance Status | Strategic Focus | Primary Strength |

| Egypt 🇪🇬 | 88/100 | Leader: Active 2nd Gen Strategy. | Sovereign AI & Arabic NLP. | Ranked #1 in Africa for Gov Readiness. |

| Kenya 🇰🇪 | 80/100 | Advanced: Active 2025–2030 Strategy. | Agritech & Grassroots adoption. | Ranked 8th in Africa (Oxford Insights). |

| South Africa 🇿🇦 | 74/100 | Finalizing: Ethics-first framework. | Rights-based & POPIA alignment. | Deepest institutional & legal maturity. |

| Nigeria 🇳🇬 | 55/100 | Drafting: Aggressive execution. | Digital economy & talent (3MTT). | Massive startup-led momentum. |

Pillar Three: Startup Ecosystems

Talent, capital, and the localization imperative

Africa’s AI funding picture is simultaneously encouraging and sobering. By mid-2025, 159 AI startups across the continent had raised a combined $803.2 million. In the same period, global private AI investment reached $100–130 billion annually. Africa’s entire five-year total represents less than what major US AI companies raise in single funding rounds.

Within Africa, the distribution is starkly uneven. Kenya and Tunisia demonstrate the best capital efficiency. Egypt leads in company count with 44 AI startups. However, its average raise of $1.9 million per company suggests an early-stage ecosystem still building towards scale.

By comparison, South Africa’s 31 companies raised $150.4 million — the highest total — reflecting the advantages of established financial infrastructure. Nigeria’s 34 startups raised $47.3 million, a lower figure that understates its ecosystem’s dynamism. Many of its companies bootstrap or raise from informal networks.

Indeed, the defining trend of 2025–2026 is the shift from “consumerism to foundational building.” The most sophisticated African AI companies are no longer wrapping foreign APIs. Instead, they are training their own models on local data, in local languages, for local contexts. Importantly, this shift is commercially important.

Generic AI products built for Western markets consistently underperform in African environments — those involving code-switching between languages, informal payment systems, and connectivity constraints.

Who owns the AI?

Yet building the AI is only half the equation. A subtler and more consequential question is: who owns the equity? The majority of Africa’s most prominent AI startups are Delaware-incorporated entities backed by US or UK venture capital. That structure routes IP, revenue, and ultimate exit value out of the continent. However, this is beginning to change.

South African pension funds, long conservative about domestic tech exposure, are starting to allocate to AI infrastructure.

Egypt’s sovereign wealth mechanisms have co-invested alongside private capital in the Technology Innovation Parks ecosystem.

The Gulf’s MGX and PIF have saturated domestic opportunities. As a result, they are increasingly looking at African AI as a strategic asset class rather than a charitable gesture.

The countries that develop local institutional capital pipelines by 2030 will capture compounding economic returns that pure-tech leadership alone cannot deliver. Leadership is not just building the AI. It is owning the IP.

The Disruptors: Startups to Watch

Nigeria — Language & Health

Awarri / N-ATLAS: Multilingual LLM infrastructure

Awarri is the core technical engine behind N-ATLAS — Nigeria’s open-source multilingual large language model. It is trained on hundreds of millions of tokens of localized data in Yoruba, Hausa, Igbo, and Nigerian-accented English.

Positioned as a national digital public good, N-ATLAS provides the language layer for chatbots, citizen services, and media transcription. It reduces dependence on foreign APIs while giving local developers a shared foundation to build on.

Moniepoint: AI-powered fintech

A fintech giant that has captured over 70% of Nigeria’s offline payment market through AI-driven credit scoring and real-time fraud detection. Moniepoint demonstrates how AI embedded in financial infrastructure can achieve mass-market penetration in an economy that runs primarily on cash and informal transactions.

Eight Medical: Emergency health AI

Uses AI to track hospital bed availability and ambulance proximity in real time, cutting emergency response times to under 10 minutes in Lagos. A model for how AI can solve infrastructure gaps rather than simply layer on top of existing systems.

AI that analyzes infant cries to detect birth asphyxia and neurological conditions — addressing one of Nigeria’s most acute health challenges with a tool that requires no specialist equipment, only a smartphone microphone.

South Africa — Infrastructure & Enterprise

ODC (Open Distributed Compute): Edge AI compute

Secured $45 million — backed by MTN and Nvidia — to convert 5G cell sites into AI-ready compute hubs. This edge architecture enables low-latency AI for autonomous mining and smart cities. It has no equivalent elsewhere in Africa. It could become South Africa’s most significant contribution to AI infrastructure on the continent.

Designs silicon-photonics chiplets that move data between AI chips using light instead of copper, dramatically reducing energy use in large-scale AI systems. Acquired by GlobalFoundries (US) in November 2025 — a rare and significant deep-tech exit from the African continent, validating that world-class chip design is possible here.

Naked Insurance: AI-native insurtech

Automated underwriting and claims processing allow users to get covered or settle a claim in seconds without any human intervention. The most mature consumer-facing AI product in Africa, demonstrating what the enterprise end-state looks like.

Egypt — Arabic NLP & Sovereign AI

Karnak (National LLM) + Olimi AI: Sovereign AI

Egypt’s state-backed large language model, launched in early 2026 and unveiled at the Ai Everything MEA summit in Cairo. It serves as the foundational layer for Arabic-dialect startups like Olimi AI. Olimi builds multilingual voice agents trained to understand Egyptian, Saudi, and Emirati Arabic — a differentiated commercial advantage across a 400-million-person market.

Intella: Arabic voice AI

End-to-end Arabic voice-to-text and sentiment analysis serving as the backbone for customer service automation across the Middle East and North Africa. Egypt is the only country with both an African footprint and deep Arabic-language AI capability. That gives Intella a market opportunity no Nigerian or Kenyan competitor can easily replicate.

SURGiA: Hospital supply chain AI

AI-powered predictive analytics managing hospital inventory across 150,000-plus orders, preventing stockouts of critical medicines. Scales through Egypt’s Technology Innovation Parks ecosystem — a government co-investment model that has created a more stable commercial environment than most African countries offer.

Last-mile AI: Startups like Apollo Agriculture are proving that machine learning is most effective when applied to essential sectors like food security.

Kenya — Agritech & Logistics

Apollo Agriculture: Satellite + ML credit

Uses satellite imagery and machine learning to provide customized credit and farming advice to over 350,000 smallholder farmers, helping them double crop yields. A global benchmark in “last-mile AI” — proving that sophisticated machine learning can be deployed profitably with minimal existing infrastructure.

Leta: AI logistics optimization

Powered over 8 million deliveries across 7 African markets using AI route and load optimization. Reduced truck usage for major clients including KFC and Twiga Foods by 25% — a quantifiable efficiency gain in a sector that directly affects food security across the continent.

An electric vehicle company whose “Pay-As-You-Drive” model is backed by an AI system managing battery health and real-time charging demand across Nairobi’s bus network. A preview of how clean energy and AI will converge in East African transport infrastructure.

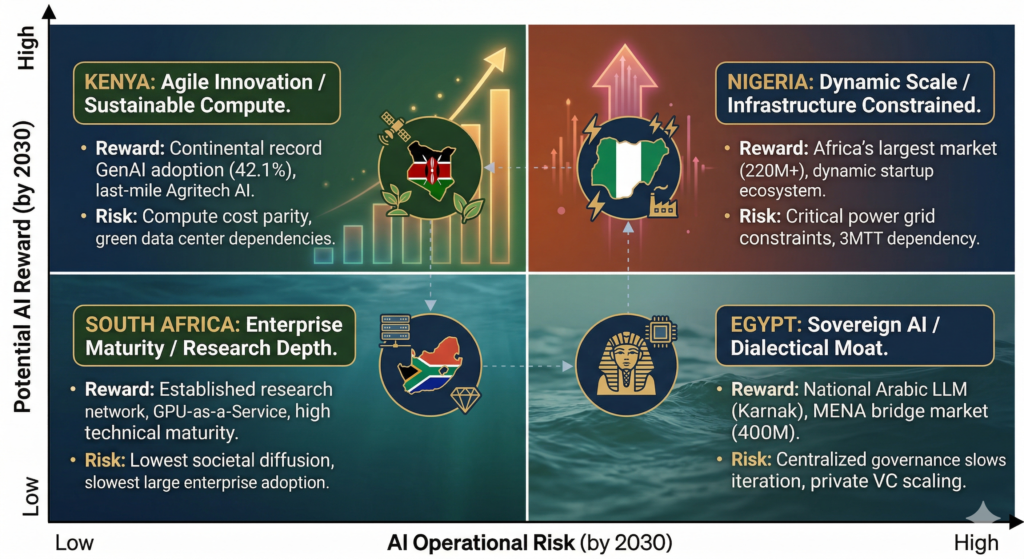

CleanTech: The 2030 Verdict

Leadership in African AI by 2030 will not be winner-takes-all. The continent is large enough — and the technological landscape differentiated enough — that multiple countries can claim meaningful leadership at once. Each will lead on its own terms.

Country by country

South Africa — Industrial & Research Leader

Benchmarked, mature, globally recognized

South Africa will almost certainly retain the enterprise and research crown through 2030. It is the only African country on global AI competitiveness rankings and has the continent’s deepest AI research network.

Its GPU-as-a-Service infrastructure — built on 5G cell sites by ODC — gives it an edge AI capability with no current continental rival. However, its weakness is diffusion: South Africa’s AI is concentrated in large corporations and research institutions, not in the daily routines of its 60 million people.

Nigeria — Economic Volume Leader

The market bet — contingent on power

Nigeria is the highest-upside bet of the four — and the highest risk. It has a population of 220 million and Africa’s densest AI startup ecosystem. Close to $1 billion in data center investment is incoming.

Specifically, its N-ATLAS language model could make Lagos the Bangalore of African AI. However, if Nigeria cannot solve its power infrastructure problem, its capacity will remain constrained to expensive diesel-backed facilities. That is still a very significant if.

North Africa and East Africa

Egypt — Regional Influence & Sovereign AI

The MENA bridge — durable and structural

Egypt’s advantage is geographic and linguistic in ways that cannot be replicated. Its Arabic-language AI infrastructure serves a 400-million-person market that straddles Africa and the Middle East. Furthermore, the Karnak LLM and the ecosystem of dialect-specific AI companies it enables give Egypt a structural commercial moat.

Egypt will lead in regional influence — acting as the primary conduit between African and Arab world AI ecosystems. That position carries significant economic weight as Gulf capital continues to pour into AI infrastructure.

Kenya — Grassroots Adoption & Sustainable Compute

Africa’s most AI-literate population

Kenya’s 42.1% generative AI adoption rate is so far above its peers that it demands its own category. This is not corporate-driven adoption. It is individual, bottom-up, small-business-driven integration that suggests AI is genuinely changing how Kenyans work and transact.

Indeed, combined with geothermal-powered data centers, a comprehensive national AI strategy, and a potential semiconductor manufacturing facility, Kenya is building the most sustainably differentiated AI ecosystem on the continent.

The economic argument is becoming structural: AI inference now accounts for roughly 90% of ongoing compute cost. Kenya’s geothermal surplus gives it a long-run marginal cost advantage that no diesel-dependent or carbon-taxed competitor can easily match. Its limitation today is depth of enterprise deployment. Its long-term advantage is that it may be the cheapest place to run AI at scale.

Structural Risks That Could Reshape the Race

Nigeria’s power ceiling

Nigeria’s grid has never crossed 6 gigawatts for 230 million people. Specifically, AI data centers require high-density GPU infrastructure with stable power. Without a structural grid breakthrough, AI workload capacity will remain constrained to diesel-backed private facilities — expensive, environmentally costly, and ultimately unscalable.

The $803M vs $130B gap

Africa’s total AI startup funding through mid-2025 was $803 million across five years. Global private AI R&D investment reached $100–130 billion in 2024 alone. The infrastructure gap is not just large — it is accelerating. Consequently, this concentration risk means a few company failures could collapse entire national AI ecosystems.

Talent, energy, and geopolitics

Talent arbitrage — not just brain drain

The classic “brain drain” framing is outdated. By 2026, the more accurate picture is talent arbitrage. Many of Nigeria’s and Kenya’s most senior AI engineers live in London, Berlin, or Toronto but lead Lagos- or Nairobi-based teams remotely. Notably, the short-term benefit is real — diaspora engineers bring global standards home.

However, the structural risk is subtler: the hollowing out of local middle management. As OpenAI, Google DeepMind, and Mistral increasingly poach senior African AI talent for remote roles at Western salaries, the next generation of team leads and mentors never forms on the ground.

Countries that develop local retention incentives — equity schemes, university research funding, government AI labs — will compound their ecosystems faster than those relying purely on diaspora goodwill.

Energy, compute, and geopolitics

The energy-compute paradox

A critical distinction separates AI training from AI inference. Training a large model is a one-time energy event. Inference — running the model millions of times daily — is where 90% of total AI compute cost accumulates by 2030. Consequently, this asymmetry reshapes the competitive map entirely. Kenya’s geothermal surplus means its marginal cost of AI inference could actually decrease over time as new capacity comes online.

South Africa, by contrast, faces rising carbon taxes on its coal-heavy grid. Nigeria’s GPU-class facilities depend on diesel generation that scales poorly and expensively. For startups choosing where to host inference infrastructure by 2028, Kenya’s clean power economics may therefore matter more than South Africa’s current data center density.

This is the energy-compute paradox: the country with the smallest enterprise AI footprint today may have the lowest long-run compute costs tomorrow.

China’s DeepSeek playbook

Chinese AI models are accelerating adoption across Africa through accessibility-first pricing strategies. Specifically, this could shape the continent as a consumer of Chinese AI infrastructure rather than a builder of its own. The sovereign AI movements in Egypt and Nigeria are partly motivated by precisely this concern. How this geopolitical dynamic resolves will shape which country’s infrastructure investments prove most durable.

Ghana: the disruption nobody is talking about

Ghana secured a $1 billion UAE deal for what is described as Africa’s largest AI hub, scheduled for launch in 2026. Google opened its first AI Community Center in Africa in Accra in July 2025, building on its 2019 AI research lab there. If the UAE-backed hub delivers at scale, Ghana could meaningfully disrupt the Big Four narrative before 2030 — particularly in West Africa, where Nigeria currently has no serious infrastructure rival.

As of late March 2026, the AI policy landscape in Africa has moved from “high-level strategy” to “operational enforcement.” To provide a balanced perspective across the Big Four, these recommendations focus on solving the structural “Development-Governance Paradox”—the challenge of regulating a technology before the infrastructure to support it is fully built.

The Risk/Reward Matrix visualizing where the Big Four stand in the race to 2030

Strategic Policy: The 2030 Roadmap

1. Data Sovereignty & “Digital Embassies”

The primary risk for 2030 is “Digital Colonialism”—where African data is trained abroad, and the resulting insights are sold back to the continent.

- The Recommendation: Adopt the Federated Learning model. Instead of moving raw data (from hospitals or banks) to central servers, policies should mandate that models move to the data.

- Implementation: * Egypt is already leading this with Karnak, its sovereign LLM.

- Nigeria should codify its N-ATLAS project as a “Digital Public Good” to ensure local startups don’t have to pay foreign API fees for local language processing.

2. The “Green Compute” Subsidy

Compute cost is the single greatest barrier to entry for African startups. High energy costs in South Africa and Nigeria make local AI training prohibitively expensive.

- The Recommendation: Implement “Compute Credits for Compliance.” Governments should provide subsidized access to National AI Hubs (like the one recently announced in Ghana or Kenya’s Geothermal AI Park) for startups that meet ethical and local-data standards.

- Implementation: * Kenya can leverage its geothermal surplus to offer the continent’s lowest “Carbon-per-Inference” rates.

- South Africa should pivot its GPU-as-a-Service (ODC) initiative into a public-private utility to lower the barrier for SMEs.

3. From “Brain Drain” to “Talent Circulation”

With global firms like Google and Microsoft opening R&D centers in Nairobi and Lagos, the risk is that local talent is absorbed into “Global AI” rather than “Local Solutions.”

- The Recommendation: Establish National AI Fellowships that allow top engineers to split their time between global firms and local public sector challenges (e.g., AI for the 2027 Kenyan General Election or Nigerian power grid optimization).

- Big Four Implementation: * Nigeria’s 3MTT (3 Million Technical Talent) program should evolve into a specialized “AI Residency” program that offers equity grants for engineers building local “last-mile” applications in agritech and health.

Comparison of Current Legislative Status (March 2026)

| Policy Area | South Africa | Nigeria | Egypt | Kenya |

| Governance Model | Multi-Regulator: Embedding AI into existing bodies (FSCA, POPIA). | Hybrid: National AI Research Scheme (NAIRS) + Digital Economy Bill. | Centralized: National Council for AI (NCAI) leading unified strategy. | Legislative: AI Bill 2026 (Senate) creating an AI Commissioner. |

| Data Rights | Strong POPIA alignment; focus on bias mitigation. | Focus on “Indigenous Data” protection via NDPA. | Sovereign data mandate; national “Foundation Model” ownership. | Right to “Plain Language” explanation of AI decisions. |

| Sandbox Status | Proposed in Draft Policy (March 2026). | Informal sector-led sandboxes (Fintech focus). | Active Technology Innovation Parks (SME focus). | Mandatory “Regulatory Sandboxes” in AI Bill 2026. |

To ensure Africa doesn’t just consume AI but owns its future, the “Big Four” must pivot toward these three structural interventions:

I. Federated IP

Mandate a “Federated Learning” architecture for high-stakes sectors (Health, Finance). Instead of moving raw African data to foreign cloud servers, models must be trained locally on-site.

- The goal is to protect “Indigenous Data” and ensure the intellectual property of localized insights remains within national borders.

II. The Compute Credit Exchange

Establish a National AI Compute Fund that provides subsidized GPU access to local startups in exchange for “Public Good” contributions (e.g., using their models to solve local grid or water issues). This will lower the barrier to entry caused by the high cost of NVIDIA/specialized hardware.

III. STEM Talent Circulation

Shift from preventing “Brain Drain” to encouraging “Talent Circulation.” Create “AI Residency” visas that allow the diaspora to consult for local government projects remotely or through short-term physical residencies without losing their international status. It Infuses local ecosystems with global senior expertise while maintaining local leadership.

Legislative Maturity Index (2026)

| Pillar | Egypt 🇪🇬 | Kenya 🇰🇪 | South Africa 🇿🇦 | Nigeria 🇳🇬 |

| Data Rights | Sovereign Mandate | Privacy-First | POPIA-Aligned | Execution-First |

| Compute Subsidies | High (State-led) | Emerging (Green) | Mature (Private) | Pipeline ($1B) |

| Regulatory Lead | ITIDA | AI Bill 2026 | Dept. of Science | NITDA/3MTT |

The four parallel races

Africa’s AI race to 2030 is not a single contest. It is four parallel races running simultaneously — for infrastructure maturity, policy depth, startup density, and genuine population-level adoption. Specifically, South Africa is winning the first. Egypt and Kenya are contending seriously for the second. Nigeria is winning the fourth.

Overall, what the data makes clear is that the era of African AI “aspiration” has definitively ended. Data centers are going up. National language models are being trained. Startups are building for African realities rather than adapting Western products.

Governments are moving from strategy to enforcement. The question for the next four years is therefore not whether Africa will have an AI ecosystem — it clearly will. Instead, the question is who builds the infrastructure the rest of the continent depends on, and whether that infrastructure stays on African soil.

Given the current trajectories, South Africa provides the enterprise foundation. Nigeria supplies the market momentum. Egypt controls the regional gateway. Kenya demonstrates what mass adoption actually looks like. Any serious bet on African AI needs all four in the analysis.

The Comparison at a Glance

| Dimension | South Africa 🇿🇦 | Nigeria 🇳🇬 | Egypt 🇪🇬 | Kenya 🇰🇪 |

|---|---|---|---|---|

| Data centers | 49 — continental leader | 16, rapid expansion underway | 14, strong subsea connectivity | 18, geothermal-powered |

| AI adoption rate | 15.3% (internet users) | 8.2% | 13.4% (diffusion rate) | 42.1% — continental record |

| AI startups | 31 companies, $150M raised | 120+ companies, $47M raised | 44 companies, $83M raised | Strong fintech & agritech density |

| Policy status | Final approval (2026) | Still drafting (mid-2025) | #1 Africa — active 2025–2030 | Active March 2025 strategy |

| Key strength | Infrastructure & enterprise depth | Market scale & startup volume | Arabic NLP & MENA reach | Grassroots adoption |

| Critical risk | Low adoption despite maturity | Power grid constraint | Centralized model limits speed | Infrastructure & funding scale |

| 2030 role | Industrial & research leader | Economic volume leader | Sovereign AI & regional bridge | Grassroots & green compute hub. |