By 2025, African debt became something different entirely: a geopolitical laboratory where China quietly rewrote rules that Western institutions spent decades perfecting.

The usual Western “referee” system? Facing new competition.

IMF warnings? Louder, but less decisive.

And China? Busy redrawing the playbook.

This isn’t just about loans. It’s about who gets to define what fair or sustainable means in global finance.

Key Takeaways

- China now co-chairs major African debt restructurings alongside Western creditors—a first in multilateral finance

- Kenya has implemented yuan-based repayment models, while Ethiopia and Zambia explore similar approaches

- The IMF no longer sets the terms alone—bilateral flexibility has become the new norm

- Africa’s external debt ($1.1 trillion) now exceeds the combined GDP of its three largest economies

- China’s “delay and extend” strategy—timeline extensions and rate cuts without principal forgiveness—has become the new standard

- The emerging hybrid system offers speed and flexibility but raises concerns about transparency and coordination

Africa’s Debt Landscape: The Mounting Pressure

Africa’s external debt hit approximately $1.1 trillion in 2024—larger than the GDP of South Africa, Nigeria, and Egypt combined. The pressure? Mounting across the continent, with twenty-two low-income African countries either already in debt distress or at high risk by early 2024.

Who Owns the Debt?

China: 12-17% of Africa’s total external public debt, making it the largest bilateral creditor outside the Paris Club

Eurobond lenders: private creditors, unpredictable and expensive

Multilateral lenders: IMF, World Bank, AfDB — still the “stabilizers,” but now competing for influence

Many high-debt African countries spend over 30% of their revenue servicing debt, with the continental average around 27-30%. That’s more than what some allocate to education and healthcare combined.

Countries like Ghana, Zambia, and Kenya feel it most acutely. Each debt service payment becomes a political calculation — pay the bondholders, or pay the citizens?

China’s Expanding Role: From Builder to Banker

China’s role isn’t what it used to be. It’s no longer just building roads and stadiums — it’s now deciding repayment timelines, interest structures, and even what currency the bill comes in.

As Africa’s largest bilateral creditor, China holds 12-17% of the continent’s total external public debt. But Beijing’s approach diverges sharply from Washington’s or Paris’s.

While the IMF writes policy papers, China negotiates in hotel conference rooms — one country at a time. It doesn’t lecture about governance or impose political reforms; instead, it tweaks maturities, extends tenors, and experiments with yuan swaps.

Critics call it “debt diplomacy.” African finance ministers often note faster responses and greater flexibility—though critics point out this speed frequently comes with limited transparency and minimal parliamentary oversight, concerns echoed by Western creditors and civil society organizations.

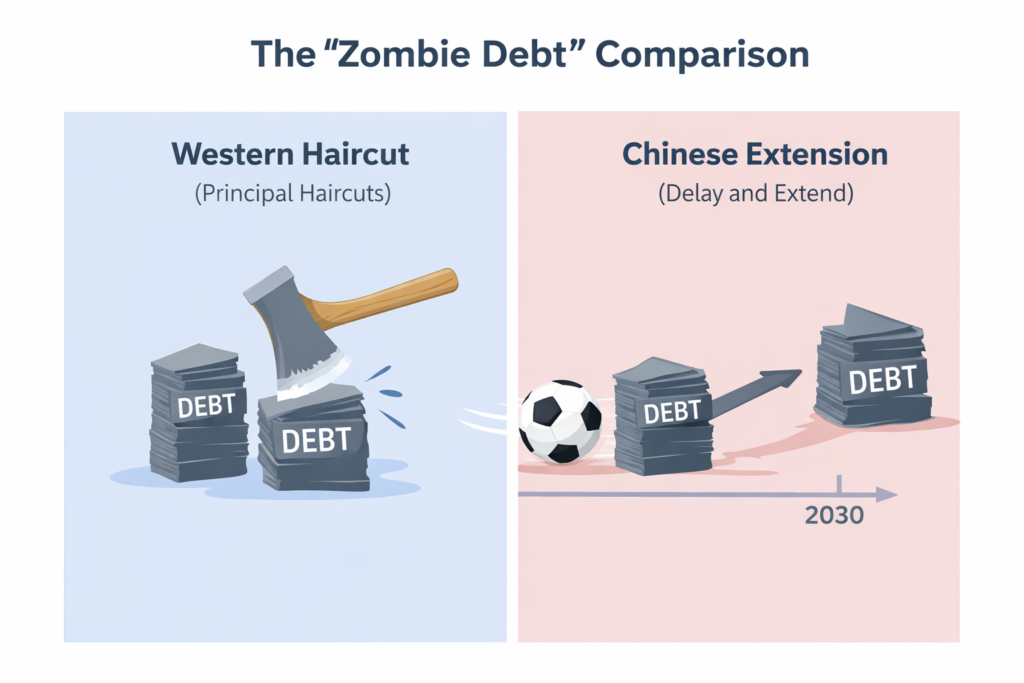

Understanding China’s “Delay and Extend” Philosophy

China’s strategy differs fundamentally from traditional debt relief. Rather than writing off part of what countries owe (what finance experts call a “haircut”), Chinese creditors prefer to:

- Extend repayment timelines dramatically: Zambia’s debts were pushed out to 2043—over 12 years beyond the original schedule

- Slash interest rates: Down to 1-2.5% in Zambia’s case, compared to original rates of 4-6%

- Keep the original loan amount intact: No principal reduction

This “reprofiling” approach achieves significant reductions in present value—Zambia saw a 40% reduction in debt burden measured in today’s money—without China technically forgiving a dollar of the original loan.

Why does China insist on this method? Many Chinese loans fund major infrastructure—ports, railways, power plants. By maintaining the nominal loan value, China preserves its long-term legal and financial stake in these assets for decades to come. It’s patient capital with strategic patience to match.

Debt Stock vs. Debt Flow: While China fixes the flow (how much is paid each month), the stock (the total mountain of debt) never gets smaller.

Related guide: How the Belt and Road Initiative Evolved After 2023

Before the Disruption: Old Rules, New Frustrations

There was a time when all debt roads led to Paris. The Paris Club set the standards for restructuring. Uniform terms. Predictable (if rigid) outcomes. Then came COVID-19, the G20’s Common Framework, and good intentions that stumbled over bureaucracy.

Coordination collapsed almost immediately.

Private creditors dragged their feet—Ghana’s restructuring negotiations with Eurobond holders stretched for over two years, exemplifying how private creditors can effectively veto comprehensive relief packages.

China bristled at being told what to do, particularly when the framework assumed it would simply accept Paris Club terms developed without Beijing’s input.

And borrowers waited months, sometimes years, just to hear if relief was even possible.

The frustration was mutual. Western institutions wanted China “in the tent,” but on their terms. Beijing wanted flexibility and recognition as an equal player. The borrowers? They needed cash — fast.

The G20 Common Framework was designed to coordinate all major creditors—traditional Paris Club members like France and Germany, plus newer players like China, India, and Saudi Arabia. In theory, everyone agrees to provide comparable relief so one group doesn’t benefit at another’s expense.

In practice, the framework has proven fragile. Zambia’s four-year restructuring timeline revealed how a single major creditor with different priorities can slow the entire process to a crawl.

The Pivot (2023–2025): China’s Quiet Reinvention

Then came the pivot. From big loans to smart restructuring. From lending for prestige projects to managing repayment diplomacy. From direct government loans to channeling funds through African financial institutions.

The Lending Pattern Shift: A Strategic Repositioning

Perhaps the most revealing change isn’t in restructuring old debts—it’s in how China is deploying new money.

Chinese lending to African governments had collapsed from a peak of $28.4 billion in 2016 to just $1.9 billion in 2020. But 2023 saw a rebound to $4.61 billion—the highest volume since 2019.

The crucial detail? Over half that money—$2.59 billion—went to African financial institutions rather than directly to governments.

This represents sophisticated risk management. From 2000 to 2022, only 5% of Chinese loans went to Africa’s financial sector. In 2023, it was over 50%. That’s not a trend—it’s a strategic pivot.

By channeling funds through African multilateral banks and nationally-owned financial institutions, China maintains economic presence and influence while avoiding direct exposure to sovereign balance sheets that might end up in the next round of debt restructuring.

Yuan Settlements and Currency Flexibility

China’s post-2023 strategy introduced yuan settlements to reduce dollar dependency for resource-rich borrowers. Currency swaps let countries like Ethiopia and Kenya negotiate liabilities in more flexible terms, though the IMF has warned about currency volatility risks and the potential for increased exposure to yuan fluctuations.

From Multilateral Gridlock to Bilateral Speed

No long IMF waiting lines, no multilateral red tape. China’s bilateral approach prioritizes speed, though transparency advocates note this often means contracts bypass parliamentary review and public scrutiny—including confidentiality clauses, escrow accounts, and cross-default triggers that aren’t fully visible to other creditors.

Revenue-Linked Structures: A New Model

Tying repayments to project cash flows rather than arbitrary schedules represents genuine financial innovation. These structures acknowledge that infrastructure projects generate value over time, not immediately.

Zambia’s case proved the model works—when transparency concerns are managed.

When China co-chaired Zambia’s creditor committee with France, it was more than symbolism. It was a declaration: We can lead this now too.

Zambia’s Hard-Learned Lesson: Four Years to Resolution

When Zambia became the first African nation to default during the COVID-19 pandemic in November 2020, few anticipated it would take four years to reach a debt deal. The negotiations revealed something important: getting China, Western governments, and private investors to agree on debt relief is far more complicated than anyone expected.

Fast-forward to 2024 — the deal closed. Zambia’s restructuring covered $6.3 billion in external debt. China agreed to extend maturities to 2043 while reducing rates to 1-2.5%—terms that achieved a 40% reduction in present value, meaning Zambia’s debt burden lightened significantly in today’s money.

The IMF cheered from the sidelines. Bond prices rose slightly, signaling restored confidence.

The October 2023 Standoff: Comparability as a Weapon

But here’s where it got complicated. In October 2023, China—as co-chair of Zambia’s Official Creditor Committee—effectively blocked the country’s agreement with private bondholders. The reason? China argued the bondholders weren’t offering relief “comparable” to what official creditors provided.

Analysis showed China was demanding that private creditors accept terms more generous than what the IMF said was necessary to restore Zambia’s debt sustainability. In the revised deal that eventually emerged, official creditors (including China) would recover 55 cents per dollar lent, while private bondholders would get 62 cents per dollar—yet China had successfully forced deeper concessions from the private sector.

This wasn’t just technical haggling. It was a strategic use of veto power to shift the financial burden onto commercial lenders while China preserved its own position through extended timelines rather than actual losses.

Yet the exact terms remain murky. Transparency? Limited. Contract details were negotiated behind closed doors with minimal public disclosure—a pattern that concerns Western creditors and governance advocates. Yet the country got breathing space, and local markets responded positively.

Zambia taught Beijing something crucial: collaboration sells credibility. You can lead behind closed doors, as long as outcomes look reasonable to everyone else—and you can use the “comparability” principle to protect your interests while appearing cooperative.

Zambia is now monitoring yuan-based settlement models for future negotiations, though implementation remains in early exploratory stages.

Ethiopia’s Balancing Act: Speed Through Standardization

Ethiopia’s case was subtler—and notably faster than Zambia’s tortuous process. It restructured approximately $8.4 billion in bilateral debt in March 2025, with over $1 billion from China. The deal provides $2.5 billion in debt service relief through 2028, paving the way for the IMF to return with a $3.4 billion Extended Credit Facility by mid-2025—a sign of restored confidence.

The relative speed suggests China has now standardized its approach: participate in the G20 Common Framework, but on Beijing’s terms—no principal cuts, aggressive timeline extensions, and strict enforcement of “comparability” with private creditors.

But Ethiopia’s story is less about the numbers and more about performance optics. Infrastructure loans tied to telecom and transport — vital sectors — couldn’t default without major fallout. So China allowed breathing room, carefully.

The message? “We’ll help, but we need you to stay functional.”

Negotiations with private bondholders faced impasses through 2025, but Ethiopia’s hybrid model — Chinese patience plus IMF oversight — might just be the new template for other African nations navigating dual dependencies.

Ethiopia is currently negotiating a $5.38 billion swap arrangement, though finalization remains pending as of late 2025.

Ghana’s Market Success Story: The Power of Credibility

Ghana offers a more optimistic angle. Despite not being part of the Common Framework’s initial focus countries, Ghana achieved one of the fastest credit rating upgrades after debt restructuring in recent memory. By mid-2025, Ghana had successfully returned to international capital markets—a crucial milestone that most distressed countries struggle to reach.

Ghana’s success demonstrates something important: when African governments commit to fiscal reforms and work transparently with creditors, market confidence can return surprisingly quickly. This creates a positive cycle—better creditworthiness makes external creditors, including Chinese entities, more willing to finalize agreements because the likelihood of eventual repayment increases.

However, the road wasn’t smooth. Ghana’s restructuring negotiations with Eurobond holders stretched for over two years, exemplifying the “coordination chaos” that plagues the new multipolar system. Private creditors demanded better terms than bilateral and multilateral lenders offered, creating the exact comparability disputes that paralyzed Zambia’s process.

Standard Gauge Railway train in Kenya, linked to the dilemma of Yuan-based debt repayments

Kenya’s Yuan Conversion: Bold Implementation

Kenya’s problem isn’t insolvency — it’s cash flow. Payments for the Standard Gauge Railway, energy grids, and highways have piled up faster than tax revenues. China is now its largest bilateral creditor, holding approximately $8 billion in loans, with $600 million in annual SGR debt service alone—nearly 10% of government revenues.

The solution? Kenya converted $3.5 billion in Chinese loans to yuan repayment in 2025, saving approximately $215 million annually by eliminating dollar conversion costs. It’s bold and practical—Kenya imports heavily from China, so settling in yuan cuts out the dollar bottleneck.

Still, there’s an elephant in the room — a major Eurobond maturing in late 2025. If markets stay hostile, President Ruto’s government may be forced into Zambia-style comprehensive talks by year’s end, complete with the lengthy negotiations and private creditor standoffs that characterized both Zambia and Ghana’s restructurings.

The “New Rules”: How China Is Rewriting the Playbook

We’re now seeing a new sovereign order take form. Beijing may not be shouting about it, but the rules are evolving in real time.

Comparison: Old System vs. New Hybrid Model

| Aspect | The Western “Reset” | The Chinese “Hybrid” |

| Long-term Impact | Clean slate, but immediate pain (Austerity). | No immediate pain, but 20+ years of debt overhang. |

| Investor Reaction | Restored confidence via lower debt totals. | Caution due to “hidden” seniority and lack of data. |

Five Pillars of the New System

1. Comparable Treatment—With Teeth

When France and China co-chaired Zambia’s creditor committee, it marked the first time a non-Western power shared equal billing in African restructuring. China now demands the same seat at the table as traditional Paris Club members—and uses that seat to enforce strict “comparability,” ensuring private creditors share the burden.

2. Delay and Extend, Don’t Forgive

China’s reprofiling approach has become the standard: dramatic timeline extensions (Zambia to 2043, over 12 years beyond original schedules), slashed interest rates (1-2.5%), but no principal reduction. This preserves China’s nominal stakes while providing immediate relief.

3. Selective Openness

Transparency remains limited, but China has begun publishing aggregate lending data and participating in creditor coordination forums—unthinkable five years ago. However, individual contract terms often remain confidential with opacity creating suspicion among Western creditors, frustrating multilateral partners who require public disclosure for their own accountability.

4. Financial Innovation

Loans tied to project revenues, resource-backed structures, and yuan-denominated repayments — these aren’t simple forgiveness packages. They’re experimental financial engineering that acknowledges infrastructure economics differ from sovereign bonds. China’s 2023 shift toward funding African financial institutions rather than direct government loans represents sophisticated risk management that insulates Beijing from sovereign default while maintaining influence.

Close-up of financial documents and a decisive handshake between China and African officials over a specific bilateral debt renegotiation contract

5. Global Legitimacy Through Standardization

China now co-leads creditor forums and speaks the language of “debt sustainability”—borrowing IMF vocabulary while rejecting IMF oversight. Ethiopia’s relatively fast restructuring (compared to Zambia’s four-year ordeal) suggests China has standardized its approach enough to accelerate deals when borrowers meet Beijing’s conditions.

At FOCAC 2024, China pledged $50 billion in financing but offered limited direct debt relief, instead focusing on restructuring existing obligations and channeling new financing through intermediaries.

It’s not the Paris Club 2.0 — it’s messier but potentially more realistic.

For Africa, this hybrid model feels closer to home: slow, flexible, sometimes opaque, always political — but workable.

Under the Hood: The Real Tensions

Still, tension hums beneath the surface.

1. Transparency Wars and Contractual Opacity

China’s contracts remain secretive, often skipping parliamentary oversight. Western creditors and governance advocates strongly oppose this approach.

Chinese loan agreements often include confidentiality clauses, escrow accounts, and cross-default triggers that aren’t fully visible to other creditors. This makes it hard to verify whether everyone’s truly sharing the burden equally. Kenya’s SGR contracts weren’t fully disclosed to parliament until after signing. Zambia’s restructuring terms remain partially confidential even after closure.

Borrowers quietly admit they sometimes prefer this opacity — fewer political headaches, faster deals — but the lack of public accountability creates long-term governance risks and undermines democratic oversight.

Escrow Accounts: Many Chinese loans require the borrower to keep a “cash buffer” in a specific account. If the borrower misses a payment, China takes it automatically. Other creditors (like Eurobond holders) feel that if China has a secret “shortcut” to getting paid, their own investment is riskier. This is why they charge higher interest rates to African nations—a “Transparency Tax.”

2. Coordination Chaos and Private Creditor Wildcards

Private creditors remain the wildcards. Eurobond holders can veto entire restructuring packages. Ghana’s negotiations dragged for over two years as private creditors demanded better terms than bilateral and multilateral lenders offered. Zambia’s October 2023 standoff showed how China can block deals it deems insufficiently “comparable.”

Without private creditors agreeing to comparable relief, “comprehensive solutions” remain aspirational. The Paris Club’s principle of “comparable treatment” assumes all creditors will act in coordinated good faith. Reality proves messier, especially when major players use that principle strategically.

3. Institutional Complexity on the Chinese Side

Unlike unified Western lending agencies, Chinese lending involves multiple entities—the Export-Import Bank of China, China Development Bank, Industrial and Commercial Bank of China—each with different mandates and risk appetites. This institutional fragmentation makes coordination difficult even when Beijing wants to move quickly.

4. Political Versus Economic Motives

Western creditors historically focused on economic sustainability. Chinese lending often serves broader geopolitical and developmental goals—maintaining influence, securing resource access, supporting Chinese contractors—which changes the calculus of what constitutes acceptable relief. This creates fundamental misalignment in creditor priorities.

5. Domestic Pain Points

Austerity measures, subsidy cuts, and public sector layoffs fuel protests from Accra to Lusaka. In Kenya, 2024 protests against tax increases and austerity turned violent. In Zambia, fuel subsidy removal sparked widespread demonstrations.

Citizens may not care whether debt came from Paris or Beijing — they just see rising fuel prices, closed clinics, and frozen public sector salaries. The political cost of restructuring falls on democratically elected governments who must balance external creditor demands with domestic political survival.

6. Currency Risks

While yuan settlements offer flexibility, the IMF warns about new vulnerabilities. Countries taking on yuan-denominated debt exposure themselves to Chinese monetary policy and yuan volatility rather than dollar volatility—trading one risk for another rather than eliminating it.

Global Ripples: The New Multipolar Debt System

Zoom out. The real story isn’t Africa alone. It’s the slow-motion reorganization of global finance.

The IMF and World Bank are learning to share the sandbox. Private lenders are pricing risk differently when China’s in the mix — sometimes cheaper (due to competition), sometimes not (due to complexity and coordination challenges).

By 2026, we’re seeing the emergence of a multipolar debt system: a few Western institutions, a pragmatic China, and dozens of African borrowers testing both sides for terms that actually work.

Think of it as diplomacy, but with spreadsheets.

This shift has implications beyond Africa. Middle-income countries across Asia and Latin America are watching these experiments closely. If the hybrid model proves sustainable, expect wider adoption. If coordination collapses or transparency concerns escalate, the G20’s Common Framework may face fundamental redesign.

The four-year Zambia timeline and two-year Ghana negotiations show how fragile this system remains—a single major creditor with different priorities can slow the entire process to a crawl.

What African Leaders Are Demanding: Beyond the Debt Cycle

African leaders are increasingly pushing back on the debt-finance model itself. At recent forums, they’ve called for a fundamental shift—less borrowing for infrastructure, more Chinese investment in local industries, and crucially, better trade terms so African countries can export more to China.

The logic is sound: generating dollar revenues through trade reduces the structural need for dollar-denominated loans that often precipitate debt crises. It’s a defensive strategy aimed at genuine financial autonomy rather than cycling between borrowing booms and restructuring crises.

Both sides now acknowledge that future engagement must include:

- Greater transparency in loan terms and conditions—no more hidden clauses

- Stronger debt sustainability analysis before commitments—avoiding unviable projects

- Better coordination among Chinese institutions—ending the fragmentation problem

- More focus on revenue-generating projects—infrastructure that pays for itself

- Trade over loans—boosting African exports to reduce borrowing dependency

The era of massive, opaque infrastructure lending appears to be over. What’s replacing it is more cautious, more sophisticated, and potentially more sustainable—though also potentially less transformative in scale.

Policy Moves That Could Actually Work

For African governments, this isn’t just theory — it’s survival strategy. Here’s what could shift the balance:

Publish a Centralized Loan Registry

No more hiding figures in appendices. Debt sustainability starts with knowing exactly what’s owed, to whom, when, and under what conditions—including those confidentiality clauses. Several countries lack basic debt management information systems—fixing this is foundational.

Train Debt Analysts in Every Finance Ministry

Negotiating leverage comes from understanding NPV (net present value) calculations, comparability standards, and currency risk better than the lenders do. Technical capacity matters as much as political will—especially when facing sophisticated Chinese institutions that understand these metrics deeply.

Blend Repayments Strategically

Use yuan for Chinese imports, dollars for Eurobonds, local currency for regional trade. Diversify the exposure rather than concentrating risk in a single currency corridor. Kenya’s $215 million in annual savings shows the practical benefits.

Create an AU-Led Debt Coordination Forum

It would give Africa a united voice when talking to both China and the West—preventing divide-and-conquer tactics. Currently, each country negotiates alone, weakening collective bargaining power. China’s bilateral preference exploits this fragmentation.

Demand Transparency in All Deals

Whether negotiating with Paris, Beijing, or private bondholders, African governments should insist on parliamentary oversight and public disclosure of major contract terms. Short-term political convenience shouldn’t override long-term governance standards. Ghana’s transparent approach to reforms helped restore market confidence faster.

Shift the Conversation from Loans to Trade

Follow the path African leaders are advocating: push for better market access to China, investment in local manufacturing, and trade terms that generate revenues rather than debts. This addresses the structural problem rather than just managing its symptoms.

Looking Ahead: The Hybrid Order Takes Shape

The next phase will be characterized by reform, resilience, and realignment. China’s not replacing the West. It’s remixing the system — projects that generate profit instead of promises, deals cut over tea instead of press briefings, loans channeled through African institutions rather than directly to governments.

Africa’s role? To negotiate smarter. With data, not desperation.

Zambia proved comprehensive restructuring is possible when China cooperates—though it takes four years of painful negotiation. Ethiopia showed that standardized approaches can work faster when borrowers meet Beijing’s conditions. Ghana demonstrated that transparent fiscal reforms restore market confidence and creditworthiness. Kenya proved that yuan settlements can move from theory to practice, creating tangible fiscal savings of hundreds of millions annually.

The Realities African Nations Must Navigate

China isn’t walking away. Despite debt crises and criticism, Chinese engagement continues—just in different forms and with different risk management. The 2023 lending rebound to $4.61 billion confirms this, though the shift toward financial institutions rather than governments signals strategic repositioning.

The G20 Common Framework works, barely. It can bring diverse creditors to the table, but the process is slow, contentious, and vulnerable to strategic blocking by major players protecting their interests. Zambia took four years; Ghana took two years just to align private creditors.

“Delay and extend” is now the standard. African countries seeking Chinese debt relief should expect long timeline extensions (to 2043 and beyond) and dramatic rate cuts (to 1-2.5%), but not principal forgiveness. This provides immediate breathing room but creates long-term debt overhang that may require further restructuring down the road.

Private creditors bear increasing burden. China’s willingness to use the “comparability” principle to force deeper private sector concessions changes the risk calculus for commercial lenders and bondholders investing in African sovereign debt. Expect higher risk premiums and tougher terms from private markets.

Indirect financing is the future. China’s shift toward funding financial institutions—from 5% of lending (2000-2022) to over 50% (2023)—signals a more subtle, harder-to-track form of engagement that insulates Beijing from direct sovereign default risk while maintaining influence.

African Nations Should Negotiate African Debt

The future of African debt won’t be written in Paris or Beijing. It’ll be negotiated in Nairobi’s Treasury building, Lusaka’s Finance Ministry, and Addis Ababa’s central bank—by officials who learned that the new rules aren’t really rules at all. They’re leverage, data, and the willingness to make both superpowers compete for credibility.

For African nations, the path forward requires difficult choices: accept these new terms of engagement, develop alternative financing sources, or fundamentally restructure economies to depend less on external capital. The countries that succeed will likely be those that combine pragmatic negotiation with Chinese creditors, fiscal discipline that restores market confidence (like Ghana), and long-term strategies to boost exports and attract non-debt investment.

Zambia restructured. Ethiopia stabilized. Ghana returned to markets. Kenya converted. The question isn’t whether Africa can navigate this hybrid order—it’s how quickly other emerging markets will copy the playbook, and whether the transparency and coordination challenges can be resolved before the next debt crisis hits.

Infrastructure vs. Austerity: The IMF often demands spending cuts (Austerity) to fix the budget. China allows the spending to continue as long as the project (the railway or port) stays under their influence.

for a leader in Nairobi or Lusaka, a “Zombie Loan” that keeps the lights on today is often more politically survivable than a “Clean Reset” that requires firing thousands of public workers tomorrow.

The “Zombie Debt” Trap: A Counter-Argument

While the “Delay and Extend” model provides immediate fiscal breathing room, many Western economists and the IMF argue it creates a long-term drag on African growth.

1. The “Evergreening” Problem

By refusing to cut the principal (the “haircut”), China effectively keeps “zombie debt” on the books. This means a country might stay technically solvent but remains heavily leveraged for decades.

- The Risk: High debt-to-GDP ratios scare off high-quality foreign direct investment (FDI), as investors fear future tax hikes or currency instability needed to service that persistent principal.

2. Opportunity Cost of “Patient Capital”

Traditional debt relief (principal cancellation) allows a country to “reset.” When debt is forgiven, that money can immediately flow into a nation’s sovereign wealth fund or new tech infrastructure.

- The Hybrid Reality: Under the “Delay and Extend” model, a country is committed to paying back the full $1 billion (plus 1-2% interest) until 2043. Even if the interest is low, the repayment obligation remains a permanent line item in the national budget, potentially crowding out internal innovation for a generation.

3. The Transparency “Risk Premium”

Western markets price risk based on data. When Chinese contracts include confidentiality clauses or “escrow-backed” project revenues, private bondholders get nervous.

- The Result: To compensate for the “unknown” variables in Chinese-held debt, private lenders may charge African nations higher interest rates on Eurobonds. In essence, the “secrecy” of the hybrid model might be indirectly raising the cost of capital from the rest of the world.

The Era of the Triple Gamble

As we look toward the 2030s, the African debt landscape has ceased to be a binary choice between Washington’s “clean slate” and Beijing’s “patient capital.” Instead, it has evolved into a sophisticated, albeit high-stakes, hybrid order. For African finance ministers, the “New Rules” represent a triple gamble:

- The Growth Gamble: Betting that “Delay and Extend” will provide enough immediate liquidity to spark industrialization before the massive nominal principal payments come due in the 2040s.

- The Transparency Gamble: Assuming that the speed and flexibility of opaque, bilateral deals with China outweigh the “transparency tax” and higher interest rates demanded by wary Western private bondholders.

- The Sovereignty Gamble: Navigating a multipolar world where leverage isn’t found in total alignment with one side, but in the ability to make both systems compete for the privilege of financing Africa’s future.

The “Zambia Model” and the “Kenya Conversion” are not just technical anomalies; they are the opening chapters of a new playbook. In this era, debt is no longer just a liability to be erased—it is a geopolitical tool to be managed. Success will not be measured by who has the cleanest balance sheet, but by which nations can convert these extended timelines into tangible economic productivity.

For the first time in decades, the rules of global finance are being rewritten in real-time—and this time, the ink is being dried in Nairobi, Lusaka, and Addis Ababa as much as in Paris or Beijing.

Frequently Asked Questions

What is yuan debt repayment and how does it work?

Yuan debt repayment allows countries to service Chinese loans using Chinese currency (yuan/renminbi) instead of US dollars. This matters because many African countries import heavily from China—machinery, consumer goods, infrastructure materials. By settling loans in yuan, they can use trade revenues directly rather than first converting local currency to dollars, then to yuan for Chinese imports. Kenya’s 2025 conversion of $3.5 billion in loans saves approximately $215 million annually in currency exchange costs and reduces exposure to dollar volatility.

Why does China prefer “delay and extend” over debt forgiveness?

China’s reprofiling approach—extending timelines and cutting rates without reducing principal—serves multiple purposes. Many Chinese loans fund major infrastructure like ports, railways, and power plants. By maintaining the nominal loan value, China preserves its long-term legal and financial stake in these assets for decades. In Zambia’s case, pushing debts to 2043 (12+ years beyond original schedules) while slashing rates to 1-2.5% achieved a 40% reduction in present value without technically forgiving a dollar. This patient capital approach aligns with China’s long-term strategic interests in maintaining influence and asset claims.

What is the G20 Common Framework and why does it struggle?

The G20 Common Framework was designed to coordinate all major creditors—traditional Paris Club members like France and Germany, plus newer players like China, India, and Saudi Arabia—so everyone provides comparable relief. In practice, it struggles because: (1) China can strategically block deals it deems insufficiently “comparable,” as happened in Zambia’s October 2023 standoff; (2) Chinese lending involves multiple institutions with different mandates, making coordination complex; (3) confidentiality clauses in Chinese contracts make it hard to verify equal burden-sharing; (4) political versus economic motives clash—Western creditors focus on sustainability, while Chinese lending serves broader geopolitical goals. The result: Zambia took four years to reach a deal.

What are the risks of multipolar debt systems?

Coordination becomes exponentially harder when creditors have fundamentally different approaches. Key risks include:

- Longer negotiation timelines: Zambia took 4 years, Ghana took 2+ years with private creditors

- Strategic blocking: Major creditors can use “comparability” requirements to protect their interests and shift burdens

- Transparency gaps: Confidentiality clauses, escrow accounts, and cross-default triggers remain hidden

- Institutional fragmentation: Multiple Chinese lending entities with different risk appetites complicate alignment

- Currency exposure: Yuan settlements trade dollar volatility for yuan volatility and exposure to Chinese monetary policy

- “Free rider” problems: Some creditors negotiate better terms, creating inequitable outcomes

How does this affect ordinary Africans?

Debt restructuring typically requires austerity: subsidy cuts, tax increases, public sector hiring freezes. In Kenya, 2024 austerity sparked violent protests. In Zambia, fuel subsidy removal caused prices to spike. The human cost—reduced healthcare, education, and infrastructure investment—falls hardest on lower-income populations. However, without restructuring, debt service crowds out all social spending. Countries like Zambia were spending more on debt service than healthcare and education combined. Restructuring creates breathing room for governments to reinvest in citizens, though the transition period is painful and politically volatile.

Why is China shifting loans to African financial institutions instead of governments?

This represents sophisticated risk management. From 2000 to 2022, only 5% of Chinese loans went to Africa’s financial sector. In 2023, it jumped to over 50% ($2.59 billion of $4.61 billion). By channeling funds through African multilateral banks and nationally-owned financial institutions, China maintains economic presence and influence while avoiding direct exposure to sovereign balance sheets that might end up in debt restructuring. It’s harder to track, reduces Beijing’s direct default risk, yet preserves strategic engagement—a win for China’s risk-adjusted returns.

What is “comparability” and why does it matter?

“Comparability” means all creditor groups should provide similar levels of relief so no one benefits at another’s expense. China has weaponized this principle strategically. In Zambia’s October 2023 standoff, China blocked the deal with private bondholders, arguing they weren’t offering relief comparable to official creditors. In the final deal, official creditors (including China) recovered 55 cents per dollar while private bondholders got 62 cents—yet China forced deeper private sector concessions by threatening to veto the entire restructuring. This shifts financial burdens onto commercial lenders while China maintains position through timeline extensions rather than actual losses.

Is China’s approach better than the IMF’s?

“Better” depends on priorities. China offers: speed (6-12 months for standardized deals), flexibility (customized terms per country), no political conditions, and preservation of relationships through timeline extensions rather than defaults. However: limited transparency, contracts bypass democratic oversight, and long-term debt overhang may require future restructuring. The IMF provides: legitimacy, technical expertise, public accountability, and uniform standards—but moves slowly (12-24+ months) and imposes unpopular austerity conditions. The emerging hybrid model—Chinese flexibility plus IMF oversight—may combine strengths if transparency concerns can be addressed. Ghana’s success and Ethiopia’s relatively fast deal suggest the hybrid approach works when borrowers commit to reforms.